Wentz Weekly: The Stock Rally Continues Following Fed’s Meeting Over Higher Rate Cut Expectations

Wentz Weekly Insights The Stock Rally Continues Following Fed’s Meeting Over Higher Rate Cut Expectations

US stocks expanded their winning streak to seven weeks, the longest since 2017. It was another strong week for stocks, particularly small caps (more on why below). The S&P 500 rose 2.49%, while the Russell 2000, an index of small sized companies, rose 5.55%. The small cap index is now up 9.7% since the end of November and up 21.5% since the last market low seven weeks ago on October 27, versus the S&P 500’s 3.3% and 15.0% return over the same period, respectively. That is a big swing from how the markets performed the first 10 months of the year (when the 7 largest of 500 stocks in the S&P 500 drove all of the index performance).

Small caps have outperformed as Treasury yields have fallen dramatically across the curve. Last week saw another large decline in yields, driven by the recent Fed meeting and markets more aggressive rate cut expectations. The 2-year Treasury yield, which is most sensitive to Fed policy, fell 30 basis points (0.30%) to 4.43% and is now down from the cycle high of 5.26% just two months ago. Meanwhile, the 10-year Treasury yield, which is sensitive to the economy and longer-term Fed policy, fell 32 basis points to 3.91%, a significant decline from 5.02% reached October 23. This has generated one of the strongest bond rallies we have seen in recent memory with shorter term bonds up a couple percentage points and longer-term bonds up nearly 20% since the October lows.

Smaller size stocks have rallied on higher expectations for more rate cuts that will happen sooner than what was previously expected. Smaller companies tend to carry more debt and higher interest rates mean higher funding costs, which cut into company profits. On the other hand, when rates go down the cost to finance growth are lower.

The reason for the change in expectations was December’s most anticipated event – the Federal Open Market Committee’s (the Federal Reserve’s policy making committee) last meeting of the year. All aspects of the meeting were taken more dovish than expected – the policy statement, the Summary of Economic Projections (SEP), and Chairman Powell’s press conference.

There was no change in monetary policy, or interest rates, as was expected. The policy statement was unchanged except for the fact it added the word “any” when determining the extent of future policy tightening. When asked about this, Powell said they added the word to recognize we are at or near the peak in rates for this cycle, not taking the possibility of future rate hikes off the table.

The more significant reason for the markets strong reaction to the meeting came in the SEP. Each Fed policymaker gives their projections on interest rates (along with things like economic growth, unemployment, and inflation) about once per quarter. Based on these projections, the median policymaker sees three rate cuts in 2024, more than the one rate cut projected in its latest SEP published in September. The remarks from Powell at the post-meeting press conference on Wednesday indicated that the members were more comfortable with inflations path downward, and that was reflected in the rate projections. One developing thing we noted was the range of projections has widened in recent meetings. For example, two policymakers saw no rate cuts and one saw six rate cuts in 2024. In addition, one saw no rate cuts in 2024 and one saw as many as 12 rate cuts.

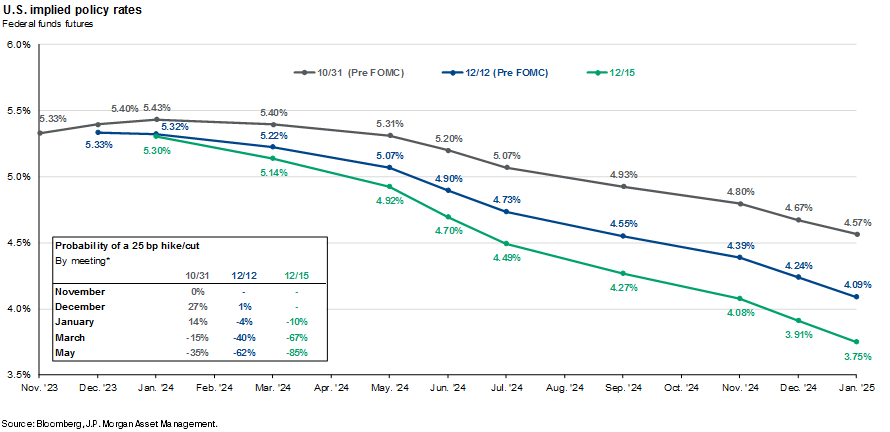

Now why did markets react so aggressively? The chart below provides an explanation. Prior to the meeting (the dark blue line), the market was forecasting four rate cuts in 2024, based on interest rate futures pricing. However, instead of moving to the Fed’s projections, markets got even more dovish and priced in even more rate cuts, now forecasting six rate cuts in 2024 (the green line). This is a huge change from October when the futures were pricing just one or two rate cuts in 2024 (the grey line).

The large swing in rate cut expectations is what has driven the large rally in stocks and bonds (rates go down, bond prices go up) since October. To add, the expectation of the first cut was pulled forward to March, up from June two months ago.

It appeared the purpose of this meeting, based on the statement and Powell’s press conference, was to set the stage for a “pivot,” that is change from a rate hike cycle to a rate cut cycle, which is the first time the Fed really acknowledged this to that extent. It was by far the closest the Fed has come to declaring victory on inflation. However, Powell did comment that the fight against inflation is not over and in his presser did not rule out additional rate hikes. We do still believe markets are getting well ahead of themselves by pricing so many rate cuts so early in 2024.

A lower interest rate environment means lower funding costs, an overall loosening in financial conditions, and higher present values for stocks (a lower interest rate creates a higher present value for future profits). After the rally over the past several weeks, stocks are now in extreme overbought territory. Goldman Sachs said in a note that the S&P 500 is nearing the most overbought level in well over a decade while nearly half of the stocks are trading at the most overbought level in over 30 years. While we are in a quiet period until the beginning of 2024, we don’t expect much additional move in stocks in either direction. However, the start to 2024 could look a lot different as we enter a weaker seasonal period, a new earnings season, more evidence of a slowing economy, and potentially the more hawkish Fed members pushing back on the markets’ aggressive rate cut expectations.

Week in Review:

Stocks opened the week mostly higher on Monday in waiting mode in anticipation of the inflation data and Fed meeting over the following days. The Treasury auctioned 3- and 10-year Treasury notes, where demand underwhelmed, but that did not have a big impact on yields, which were relatively unchanged on the day. Stocks made new 12-month highs after a 0.39% increase in the S&P 500.

Inflation data Tuesday morning was mostly as expected, but services inflation is up 5.6% annualized over the past three months, an acceleration from recent months. Despite this, Treasury markets were unfazed while stocks continued their move higher. Beside the CPI report, it was another relatively quiet day with stocks making new year-to-date highs after a 0.46% rise in the S&P 500. Energy was the worst performer again as oil fell another 3.6% as demand concerns from China (and global oversupply worries) continue.

Investors were in wait and see mode Wednesday morning up until the Fed policy decision at 2:00 and Chairman Powell’s press conference that followed. The Fed, as expected, made no change to policy but its projections showed it added more rate cuts to 2024 than what was projected in its last update from September, while Powell gave more dovish commentary at his presser. Treasury yields immediately plunged while stocks spiked – the 2 year yield fell over 40 basis points while the 10-year yield fell 17 bps to 4.02%, with stocks higher driven by smaller sized companies as the Russell 2000 rose 3.52%, the S&P 500 gained 1.37%, and Dow gained 1.40% to a new record high close.

Data on Thursday saw retail sales surprise to the upside for the fifth consecutive month in November, although the 12 month increase showed sales saw real (inflation adjusted) growth of just 1.0%, while jobless claims fell back to August lows. Stocks continued momentum from Wednesday’s Fed meeting with the soft landing narrative picking up over stronger consumer data. It was another day of broad strength, in fact the equally weighted S&P 500 index outperformed the cap weighted index the most since June, according to FactSet. The S&P 500 rose 0.26% while small caps rose 2.72% as Treasury yields continued to fall.

Markets were looking to open in positive territory Friday, that is until New York Fed President Williams pushed back on the idea policymakers are considering rate cuts, saying that were not talking about rate cuts at this time. It was a quadruple witching day, which led to increased volume at the close but it ended a mixed day overall. Small caps underperformed, falling 0.77%, while the S&P 500 was unchanged.

Driven by what the markets took as a dovish tone from the Fed, stocks surged while bond yields plummeted across the curve last week. In fact, markets have been pricing in a more dovish outlook for weeks that has led to the seventh straight week of gains for stocks. Treasury yields saw another dramatic decline, the 2-year fell 30 basis points to 4.43%, while the 10-year fell 32 bps to 3.91%. The dollar, which typically falls with a more dovish Fed, fell 1.40%, gold finished up 1.0%, and oil was higher by 0.3%, breaking a seven week losing streak, over broad market optimism and after a forecast from the IEA called for higher demand in 2024 that boosted sentiment. The major US stock indices finished as follows: Russell 2000 5.55%, Dow +2.92%, NASDAQ +2.85%, and S&P 500 +2.49%.

Recent Economic Data

Consumer inflation ended up coming in mostly as expected for November, however, core inflation is still double the Fed’s 2% target and still trending at that level. The consumer price index rose 0.1% in the month, slightly more than the no change expected. Energy is one of the major categories that contributed to lower inflation after a 2.3% decline in the month, coming after a 2.5% decline in October, while food prices were up 0.2%. In addition, over the past 12 months, the index is up 3.1%, with energy prices down 5.4% and food up 2.9%. Core prices, which takes the headline index and strips out food and energy prices due to their volatility, rose 0.3% in the month. Within the core categories, goods commodities saw the largest decline, down 0.3% driven by a 1.3% decline in apparel (retailers with sharp discounts?), while services prices were up 0.5%, driven by transportation up 1.1%, insurance costs, medical care up 0.6%, and shelter up 0.4%. One big thing to note is if you take services inflation over the past three months and annualize it, it is up a very hot 5.6%. After seeing the annual inflation rate in core prices decelerate in 10 of the past 11 months, the 12-month rate appears to have plateaued over the past couple months, settling at 4.0% in November, matching October’s 12-month increase.

The producer price index was unchanged in November, coming after a 0.5% decline in October, and was unchanged for both final demand goods and final demand services. Compared to a year ago producer prices have risen 0.9%, slowing again from the 1.3% 12-month rate in October. Energy was a big factor, where prices fell 1.2% in the month (after a 6.7% decline in October) as well as trade which fell 0.2% and transportation/warehousing which fell 0.5%. The 12-month change in producer prices excluding food, energy and trade was up 2.5%, a deceleration from 2.8% in October.

Prices of goods/services imported to the US fell 0.4% in November, now declining half of the time over the past 12 months. The decline was mostly due to fuel prices, which fell 5.6% in the month. The overall change in prices over the past 12 months is a decline of 1.4%. The change in export prices was down 0.9%, down 7 of the past 12 months and down 5.2% compared to November 2022. The decline was driven by lowest prices across the board, from industrial supplies to capital goods, consumer goods, and vehicles.

Retail sales surprisingly came in stronger than expected once again in November, surprising to the upside by a large amount for the fifth consecutive month. Sales at retail and food services rose 0.3% in the month, above the expectations of a 0.1% decline. It was not due to volatile categories either, sales excluding vehicles and gasoline were up a strong 0.6% in the month, better than the 0.1% increase expected. Spending was mixed though, 8 of the 13 major categories saw sales improve in the month, led by restaurants and bars up 1.6% (due to better weather perhaps?), sporting goods/hobby stores up 1.3%, online sales up 1.0%, and health care and furnishing stores both up 0.9%. Declines were seen in gasoline sales, as well as the miscellaneous stores, electronics, building materials, and department stores categories. Over the past 12 months sales are up 4.1%, which has been trending above the inflation rate (of 3.1%) but not by much, suggesting slow growth of real sales (inflation adjusted).

The number of unemployment claims the week ended December 9 was 202,000, down 19k from the prior week and back down to the lowest level since August. Claims have averaged 213,250 over the past four weeks. Continuing claims were 1.876 million, up 20k from the prior week (which saw a large decline from the week prior to that), with the four-week average at 1.874 million.

Industrial production increased 0.2% in November, in line with expectations with utilizations rates at 78.8%, continuing to trend at the lowest levels in over 2 years. Industrial production was driven by manufacturing and mining, which both rose 0.3% in the month, while utilities fell 0.4% which is most likely weather related as that category is very correlated to weather.

After a brief uptick in business activity in November, activity in the New York region appears to have slowed and declined again in December, according to the Empire State Manufacturing index. The headline general business conditions index was -14.5, down from a positive 9.1 in November. New orders and shipments declined, with a “significant” decline in unfilled orders and delivery times that were the shortest since before the pandemic. Employment declined while the pace of input price increases moderated and selling prices were steady. Optimism remained subdued.

Company News

Ford said it will cut production of its all-electric F-150 by 50% due to slower demand than what was expected. It will now target production of 1,600 per week, down from 3,200 per week. This follows new from October that it was cutting its spending plans on its EV business.

Toy maker Hasbro said it plans to cut 1,100 positions over the next two years as part of a cost cutting effort. This comes after it eliminated 15% of its workforce in January as part of a larger scale restructuring. It said the move was after it saw weaker than expected toy sales through the first nine months of the year.

Walgreen shares moved higher after a report said the company is restarting its discussions on a potential sale of its Boots drug chain (UK drug chain). These discussions were had multiple times last year but were discontinued over several issues including pension liabilities at the UK Boots chain, but conversations were kickstarted again after Walgreens recently made a deal with the insurer Legal & General to take over responsibility for the UK Boots pension plan. The report says it is talking about how it could separate from Boots, with one potential option an IPO on the London stock exchange, which could value the business at $8.8 billion.

Tesla recalled over 2 million vehicles over its autopilot driver assistance program. This follows an investigation by the NHTSA (National Highway Traffic Safety Administration) over multiple crashes that involved the vehicle’s autopilot.

Pfizer shares lost nearly 10% last Wednesday after it announced updated financial guidance for 2024, which includes projections for its recently announced acquisition of Seagen, that shows its total revenue and earnings forecasts much lower than the consensus estimate.

After receiving multiple buyout offers and taking weeks to examine the best outcome, U.S. Steel agreed to be acquired by Japanese steelmaker Nippon Steel. It will be a $14.1 billion deal that will value U.S. Steel at $55/share, a 40% premium to where shares traded on the previous day’s close and a 142% premium to where shares traded prior to the first report of a possible sale on August 11. U.S. Steel will retain its name, brand and headquarters in Pittsburgh after the deal closes.

Adobe said it has agreed to terminate its planned acquisition of the software company Figma because they could not see a clear path to regulatory approval from the European Commission and the UK Competition and Markets Authority. This comes several weeks after the UK regulator warned the deal would harm innovation and competition, leading to antitrust worries and concerns the deal would be blocked. As part of the initial agreement, Adobe will pay Figma a $1 billion termination fee.

A late Friday report from the WSJ said DocuSign is working with advisors to explore a sale. The possible suitors could include private equity and technology firms, but it adds the conversations are in the early stages. Shares rose over 12% after the news broke.

Other News

Other central bank headlines:

In an appearance on CNBC Friday, and the first policymaker to speak publicly since the FOMC meeting, New York Fed president Williams seemed to temper the dovish takeaway from the Fed meeting Wednesday, pushing back against the idea that policymakers are talking about rate cuts, saying “we aren’t really talking about rate cuts” adding that it was premature to talk about rate cuts in March. He repeated what Powell said Wednesday and the question is whether monetary policy is restrictive enough yet.

The International Monetary Fund said in its semi-annual economic outlook that policymakers across the globe need to keep interest rates at current levels, which are more elevated than usual, until they are sure and confident inflation is under control, despite slowing growth. The director said that sometimes central banks will “prematurely declare victory” on inflation, then it gets more entrenched and it makes it more difficult to bring inflation back down later on. This is the scenario that shaped out in the 1970s and 1980s, when policymakers were convinced inflation was coming down to a more normal level only for it to reaccelerate, and was also the last time inflation was this high.

Following the Bank of England’s policy meeting last week, it made no changes to monetary policy, holding its key interest rates steady for the third consecutive meeting, as expected. It was a 6-3 vote, with 3 policymakers voting to raise rates. It said it expects inflation to temporarily rise in January but then fall gradually after with the path of inflation lower than what it projected in its November report, due mostly to energy prices.

The European Central Bank also conducted its monetary policy meeting, voting to keep policy unchanged as well. It said that rates are at a level that will make a “substantial contribution” to bring inflation back to target, if held at these levels high enough, adding that tighter financial conditions have helped to reduce demand, which is helping bring inflation down. ECB President Lagarde said even though inflation is coming down, policymakers should not get complacent and the policymaking committee “did not discuss rate cuts at all.”

There have been mixed views and frequently changing views on the oil market by many analysts and energy agencies. The International Energy Agency (IEA) said in its December oil market report that it is cutting oil demand growth forecast slightly to growth of 2.3 million barrels per day (bbl/day) for 2023, bringing global oil demand to 101.7 million bbl/day. However, it increased its 2024 oil demand forecast by 130k bbl/day to 1.1 million bbl/day. At the same time, OPEC was more bullish, forecasting 2024 demand growth to be 2.25 million bbl/day. The improved 2024 forecast helped push oil higher last week, ending a 7 week losing streak for the commodity.

The Week Ahead

The main market events for December are behind us now, but there will still be several things in focus this week including housing market data, the PCE inflation reading, and several high profile earnings results. We will see November data on the housing market with the housing market index on Monday, housing starts and permits on Tuesday, existing home sales on Wednesday, and new home sales on Friday. In addition, the most anticipated data release will be the personal income and spending report on Friday. Economist see incomes rising 0.4%, consumer spending rising 0.3%, and most importantly a 0.2% increase in core PCE inflation, the Fed’s preferred inflation read. Other data includes consumer confidence, jobless claims, the final revision on Q3 GDP, the Philly Fed Manufacturing index, durable goods orders, and the consumer sentiment index. On the earnings side, the notable companies reporting include FedEx, Accenture, FactSet on Tuesday, General Mills, Micron on Wednesday, and Nike, Carnival, and Paychex on Thursday. Elsewhere, the corporate calendar will be pretty quiet with no brokerage conferences or investor day events. In central bank news, the Bank of Japan holds its policy meeting, while Fed speak will be light around the holiday period.

By Wentz Financial|2023-12-19T16:41:04-05:00December 18th, 2023|Uncategorized, Wentz Weekly|Comments Off on Wentz Weekly: The Stock Rally Continues Following Fed’s Meeting Over Higher Rate Cut Expectations