Wentz Weekly Insights

Trump Nominates New Fed Chairman, Eases Market Concerns

Markets were mixed last week but most stocks ended the week lower with the S&P 500 equally weighted index down 0.35%. The cap weighted index rose 0.34%, thanks to a solid week from Meta (Facebook) and Apple after their earnings reports, and crossed the 7,000 milestone for the first time ever. Small caps reversed the recent strength, along with the most shorted and momentum names, with the Russell 2000 index retreating 2.08%.

Market jitters were eased somewhat two weeks ago after the Davos World Economic Forum when Trump ruled out using force to acquire Greenland and said a framework was in place to avoid tariffs on European countries over the future of Greenland. Trump said the framework includes access to mineral rights and collaboration on the Golden Dome. We are still waiting to hear details about the framework or a possible deal.

Last week’s focus turned from politics to fourth quarter earnings season and the Federal Reserve. We saw a large chunk of the S&P 500 report quarterly financial results last week including four of the Magnificent 7; Microsoft, Meta, Tesla, and Apple (Amazon and Alphabet this week and Nvidia the end of the month).

Meta was the clear winner, up 8.8% after it reported revenue growth that accelerated and forecasted first quarter growth well above the consensus expectation. Capital expenditure/spending has been a key concern and the company forecasted spending to increase to $21.4 billion in the quarter, more than expected. Despite this, the stock was higher as investors appreciated the accelerating revenue growth more.

Apple shares were up almost 5% after its earnings report as its revenues of $143.8 billion were $5 billion more than expected with profits also above expectations, driven by better sales and higher gross margins. Apple’s biggest revenue generator, the iPhone, is what drove the better than expected results with management calling iPhone 17 demand “staggering.” Its $85.3 billion worth of iPhone sales was nearly $7 billion more than expected. Apple doesn’t typically provide detailed forecasts, but what it did provide suggested sales growth will be higher than expected in the current quarter.

Microsoft’s results were solid too, however the stock sold off nearly 10% for one of the largest market cap declines in market history. Its cloud computing platform, Azure (similar to Google Cloud or Amazon Web Services), saw revenue growth of 38% which is quite strong, however that underwhelmed investors who were expecting higher growth. Azure includes Microsoft’s AI business and investors are hoping its massive investments will pay off with higher growth. It also forecasted higher capital expenditures than expected for the current year and lower free cash flows, leading to more worries about the AI investment payoff.

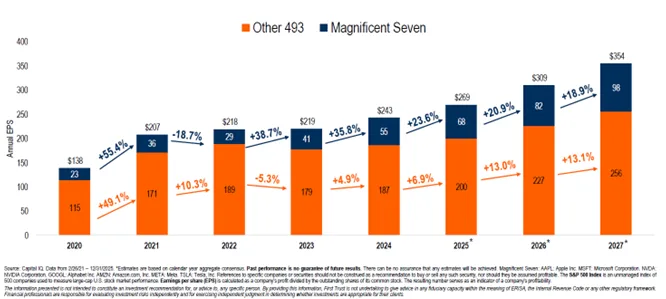

These Magnificent 7 companies are so important because they make up almost a 40% weight of the S&P 500 index. They also make up 36% of the profits of the index and the growth rate of their profits is 21%, almost double the growth rate of the other 493 companies in the index, as seen in the chart below. Each bar represents the earnings (per share) of the S&P 500 with the blue portion representing the profits made by the Magnificent 7 companies and the orange portion representing profits of the other 493 companies.

As you see, in 2020 these seven companies made up just 20% of the index’s profits, which is expected to grow to 36% this year due to their incredible growth over the past five years.

The S&P 500 as a whole is seeing much better profit growth than was expected when the quarter began. With about 33% of the S&P 500 having reported so far, current estimates see fourth quarter earnings growing at 11.9%. This is above the 8.3% expected when the quarter began. Those that are reporting higher profits than expected are reporting profits 9% higher than expectations. The key driver to the market has been stronger earnings, and it is evident it has continued in the fourth quarter.

The other big headline last week revolved around the Federal Reserve with its policy meeting Wednesday and Trump’s announcement of his nomination for the next Federal Reserve Chairman.

The Fed ended its first policy meeting of the year with no change in interest rates. It had a more upbeat view of the economy; in the statement it upgraded its view of economic activity to expanding at a “solid” pace, up from “moderate” pace. Much of the comments supported the view that the labor market is showing more signs of stabilizing while inflation has remained somewhat elevated.

Because upside risks to inflation and downside risks to employment have diminished, the Fed believes it is in a good position to pause rate cuts. It appears by recent comments the Fed sees the risks to both sides of its mandate (inflation and employment) as balanced. As such, we believe the Fed will hold rate steady for several meetings. However, Powell still was sure to emphasize these risks still exist.

Then, Friday Trump announced his pick for the next Fed chair, the former Fed governor and ex-investment banker Kevin Warsh. The immediate reaction in the markets was a re-pricing based on different monetary policy expectations – stocks fell, bond yields moved higher, the dollar strengthened, and precious metals declined – all situations that occur from a more hawkish Fed (favoring higher rates over lower rates).

The most apparent market reaction was in the precious metals market where silver plunged 30%, its worst drop since 1980, while gold fell nearly 10%. Warsh is known to lean hawkish (favoring higher rates over lower rates) and since gold and silver are traditional inflation hedges, the precious metals sold off. It is also important to keep things in perspective – silver went from under $30/oz the beginning of 2025 to $115 before Friday’s decline, now sitting in the $80s, while gold went from $2,700/troy oz to $5,500 over the same timeframe.

Focus will remain on earnings this week with another roughly 25% of the S&P 500 set to report results. In addition, we will be seeing several data reports on the labor market, although Friday’s monthly employment report may be delayed due to the partial government shutdown.

Recent Economic Data

- Case Shiller Home Price Index: In November, the average home price was up 0.4% after seasonal adjustments, but down 0.1% before seasonal adjustments, according to the monthly Case Shiller home price index. The annual increase in November was just 1.4%, a considerable slowdown over the past several years including a slowdown from the 3.8% annual rate the nation experienced November the year prior. Regional patterns for home prices continue to show large differences – the Midwest and Northeast are leading with the highest home price increases, like Chicago’s 5.7%, New York’s 5.0%, and Cleveland’s 3.4% annual gains, while the areas along the sunbelt are seeing annual declines, like Tampa’s -3.9%, Phoenix’s -0.4%, and Dallas’s -0.4%.

- Trade Balance: Estimates for fourth quarter GDP are likely to get a little downward revision after the latest data on trade. In November, the trade deficit increased to $56.8 billion, almost doubling from the 17-year low of $29.4 billion in October. The higher deficit was due to a surge in imports, rising 5.0% in the month, or by $16.8 billion, while exports fell 3.6%, or $10.9 billion (a majority of this commodities, like gold and precious metals). Year-to-date through November the deficit increased $32.9 billion, or 4.1%, compared to the same period the year before. The surge in imports could reflect solid US demand, while total trade activity, up 5.6% over the last year, reflects solid global demand.

- Jobless Claims: The number of jobless claims the week ended January 24 was 209,000, relatively unchanged from the prior week with the four-week average little changed at 206,250. The number of continuing claims at 1.827 million fell 38,000 in the week for the lowest since September 2024. The four-week average fell slightly to 1.867 million.

- Consumer Confidence: Consumer confidence, according the Conference Board’s monthly survey, deteriorated in January with some measures hitting new multi-year lows. The overall confidence index was 84.5, well lower than the 90 reading expected and the lowest reading since 2014. The present situations index was 113.7, down from 123 last month and the weakest since February 2021. The expectations index was down nearly 10 points to 65.1, the lowest since the major tariff announcements last April.

Company News

- CoreWeave: Nvidia said it will invest another $2 billion in CoreWeave to buildout its AI infrastructure, equal to about 5 gigawatts of infrastructure by 2030 to advance its AI adoption at a global scale. The deal is intended to buildout CoreWeave’s datacenters using Nvidia’s advanced AI chips to meet customer demand.

- UnitedHealth: A group of health insurers were down last week after the Centers for Medicare & Medicaid Services proposed an average reimbursement payment increase for Medicare Advantage plans of just 0.09% in 2027, equaling $700 million industry-wide. This is well below the 5% increase that was widely expected. This is just an advanced notice however. It gives insurers a chance to review and comment on the changes with the final rates typically a little higher than the proposed terms and will come by the beginning of April. A lower payment increase would squeeze insurance companies margins more, hence the stocks declines.

- Intel: Shares of Intel got a boost after the CFO disclosed a stock purchase as well as a Digitimes report that Nvidia may use Intel’s foundry to manufacture some of its chips for 2028 for its next generation AI chip platform, but that depends on improvements in Intel’s yields (the number of defect free chips produced compared to potential).

- UPS: In its earnings conference call, UPS management said it is planning to cut an additional 30,000 jobs this year as part of its multiyear turnaround plan along with its plans to wind down its partnership with Amazon. Last year it eliminated 48,000 jobs. It also said it has identified another 24 buildings to shut down, on top of the 93 it closed last year. It added it expects a total of $3 billion in savings related to unwinding it Amazon business.

- Tariffs: Trump said the US will increase tariffs on imports of South Korean automobiles, lumber, and pharmaceuticals to 25%, up from 15%, due to it not living up to its deal with the US that was finalized last year. Also, Trump warned Canada if it “makes a deal with China, it will immediately be hit with a 100% tariffs against all Canadian goods and products,” saying doing so would make Canada a “drop off port” for China to send its products into the US, including dumping steel.

WFG News

Upcoming Events:

In March, we will welcome a Social Security Specialist who will provide an overview of how Social Security works and discuss key strategies to help maximize your benefits.

Click the link below to RSVP today!

WFG Investment Classes:

Interested in learning more about investing and how the markets work? Wentz Financial Group holds various Investment Basics classes throughout the year. Contact us for details!

The Week Ahead

Its jobs week with most of the economic data reports this week focused on the labor market. The most notable data is Friday with January’s employment figures, though latest news tells us it may be delayed due to the partial government shutdown that started Sunday. The current consensus estimate sees 65,000 new jobs added in the month. Other reports include the job openings and labor turnover survey, ADP payroll figures, jobless claims, the PMI Manufacturing index, ISM manufacturing index, ISM services index, and consumer sentiment. The corporate calendar will be focused on earnings with it being the busiest week of the quarter – almost 25% of the S&P 500 index is set to report their quarterly figures. Notable companies reporting include Disney, Palantir, PayPal, PepsiCo, Pfizer, Eaton, AMD, Super Micro Computer, Chipotle, Uber, Abbvie, Alphabet, Qualcomm, Amazon, Reddit, Affirm, and Under Armour.