Wentz Weekly Insights

Software Selloff Continues as Iran Conflict Escalates

Last week, US stocks were down again in what was more of a risk-off week driven by a larger pullback in big tech, led by Nvidia’s 7% decline despite another blowout quarter. Even though the S&P 500 closed down 0.43%, breadth was positive – the equally weighted S&P 500 index outperformed by almost 1%. Defensive stocks performed the best – the consumer staples, utilities, and health care sectors were all higher by at least 2%.

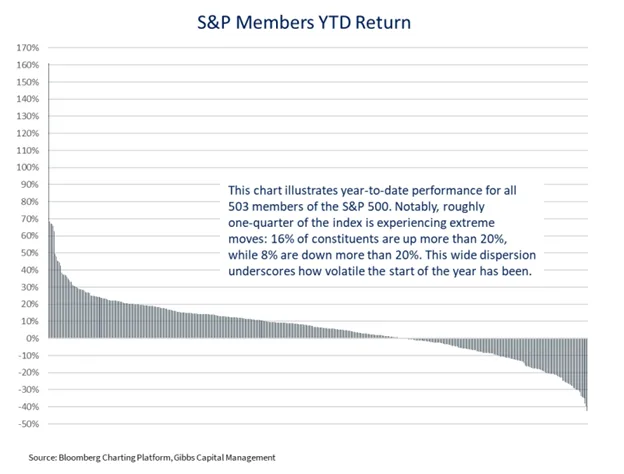

Despite the weakness in the cap-weighted index (the index is flat year-to-date), the average stock is performing well although volatility is high. The chart below shows the performance of every S&P 500 company year-to-date – roughly two-thirds of the components are positive.

But volatility of the best and worst performing stocks is what sticks out. As the chart mentions, 24% of stocks have experienced a move of at least 20% in either direction in just the first two months of the year, underscoring the higher volatility this year.

Meanwhile, credit spreads for investment grade corporate bonds widened last week the most since November, while they remain close to historically tight levels, it signals the growing risks investors are seeing. Credit spreads reflect the additional return an investor requires over a risk free benchmark (like US Treasuries), so widening spreads reflect rising default risks and fear while tighter spreads suggest optimism.

At the same time, the 10-year Treasury yield fell below 4% last week, the first time since a brief period late last year, reflecting investors buying up the safe haven asset.

There remain several evolving headlines that have been market moving – this past week most impactful was AI displacement worries, inflation, and the Iran conflict.

Technology was the worst performing sector last week, down over 2%, driven by more selling among software names. The next wave of selling was triggered by a research report from Cirtini Research, a thematic equity investing and global macro trading firm, that played out a hypothetical scenario of a macroeconomic crisis in June 2028 driven by artificial intelligence (if you’re interested, link is here). The authors call it a “thought exercise” with the purpose of exploring the risks that are underexplored, not necessarily forecasted to happen. The main idea is that AI success could unintentionally collapse the global economy from displacing human labor and destroying incomes and consumption.

Many responded to the research note, arguing AI will assist human labor and make the economy more efficient rather than displace workers.

The theme was hit further by more concerns in the private equity market. Private equity group Blue Owl, who has a larger exposure to software and newer tech companies, announced two weeks ago it was changing how investors can withdraw money from its flagship private credit funds, was restricting redemptions, and winding down its fund. The news alarmed investors and led to new concerns in the credit market.

We expect the volatility in the technology sector to continue as the economy adjusts and attempts to understand the impact, but we also see it creating buying opportunities in specific names.

Staying on the tech topic, Nvidia’s earnings report last week was another blowout – its financial results were well ahead of expectations and it provided a forecast that was well above estimates – however it was not enough to overcome the general worries in the sector.

Its CEO, Jensen Huang, also gave an attempt to calm worries around the AI displacement theme – saying the markets got it wrong and he expects firms to adopt agentic AI to build products and improve efficiencies, rather than AI agents eliminating existing software and tools. He also said “the agentic AI inflection point has arrived.”

An AI agent is a software system ran by AI that can perceive information, make decisions, and take actions to achieve a specific goal with autonomy. For example, you could tell it to book the cheapest flight to Florida next Friday and add it to your calendar and it could all be done in seconds. It could also include customer service requests.

The biggest headline in markets to start this week however revolve around the Middle East after the US and Israel carried out airstrikes on Iranian targets following weeks of building tensions. This was the fourth instance of armed conflict in Iran over the past two years, the most recent being the strikes on Iran’s nuclear facilities June 2025.

The immediate reaction in markets has been lower stock prices, lower Treasury yields, a higher dollar, higher gold – all reflecting a flight to safety – as well as a spike in oil prices. The kneejerk reaction may level out as investors understand this was expected. The US had built a massive presence in the Middle East in recent weeks, enough to make it the largest US military presence since the invasion of Iraq in 2003.

In “Operation Epic Fury” the US says the goal is to curb Iran’s ability to threaten the US and allies through nuclear weapons, missiles, and military power, while increasing political pressure on a regime change. Leading up to the strikes, there has been pressure on Iran to negotiate with threats of military action if no deal was made.

This brings another uncertainty to markets and with comments from the Trump that the US will continue its operations we expect heightened volatility to continue. The volatility index (VIX – a measure of implied volatility) spiked to 25 early this morning.

Outside of geopolitics, earnings continue this week with a big week from retailers with earnings reports from companies like Target, Best Buy, and from technology with the ninth largest S&P 500 company Broadcom. Then the week is capped off Friday with the February employment report, the first on-scheduled labor report since September. Current estimates are at 60,000 new jobs in February.

Recent Economic Data

- Producer Price Index: Inflation at the producer level ticked higher in January, increasing a more than expected 0.4% in the month. Prices for final demand goods fell 0.3%, led by a 2.7% decline in energy and 1.5% decline in food, while prices for final demand services increased 0.8%, drive by a 2.5% rise in trade. Inflation for final demand was up 2.9% over the past year and up 3.4% over the past year excluding food and energy.

- Factory Orders: Factory orders declined 0.7% in December, coming after a large 2.7% increase in November. Much of this came from transportation though, which is always volatile, as nondefense aircraft orders were down 25% in the month. Excluding transportation, orders were up 0.4%. Meanwhile, shipments of manufactured goods were stronger, rising 0.5% in the month and up 0.5% excluding defense.

- Construction Spending: Construction spending in December was at a seasonally adjusted annual rate of $2.169 trillion, 0.3% above November’s rate. Spending on residential construction increased 1.5% in the month while nonresidential spending fell 0.6% with nearly all nonresidential categories experiencing a decline. Construction spending is down 0.4% over the past year with residential down 1.2% and nonresidential up 0.3%.

- Consumer Confidence: The consumer confidence index was 2.2 higher in February to 91.2 with confidence edging higher, but remaining well below the cycle highs from 2024. The present situations index declined 1.8 points to 120.0 as net views on business conditions fell slightly. The expectations index increased 4.8 points to 72.0 with expectations for business, labor, and incomes all moving slightly higher.

- Jobless Claims: The number of jobless claims the week ended February 21 was 212,000, an increase of 4,000 from the prior week with the four-week average at 220,250. The number of continuing claims declined 31,000 in the week to 1.833 million. The four-week average for continuing claims was up 3,500 to 1.848 million.

Company News

- IBM: IBM was the latest victim of the AI disruption theme, with shares down double digits last week, down 13% Monday for its worst day since 2000, this coming after AI startup Anthropic (which runs the AI model most know as Claude) announced a new AI tool that can modernize Cobol which is a programming language that run on IBM machines.

- PayPal: Shares of PayPal were over 6% higher last Monday after Bloomberg reported the company is receiving takeover interest from potential buyers. The report added, citing people familiar with the matter, that at least one is interested in the entire company while others are interested in just parts of the company. Semafor later reported PayPal is not currently in talks to sell itself and has been working for months with bankers to prepare for a potential activist campaign or unwanted takeover bid.

- Warner Bros. Discovery: Paramount Skydance increased its bid for Warner Bros. Discovery just ahead of its deadline for its “best and final” offer, offering $31/share. The company said Paramount’s $31/share offer is superior, giving Netflix four days to counter with its offer. Netflix later withdrew its offer which pushed its shares higher.

- AMD: Shares of AMD were up last week after it said it is furthering its partnership with Meta to deploy up to 6 gigawatts of AMD chips to power Meta’s AI infrastructure, a deal valued at more than $100 billion. Meta will buy enough of AMD’s latest AI chips to power data centers up to 6 gigawatts of computing power over the next five years. The news helped lift other AI related stocks as well.

- Meta: The Information reported Meta made a multi-billion dollar deal to rent AI chips from Google and is also in talks to buy its chips for its data centers starting next year. Recall Google makes its own tensor processing units (TPUs) that power AI. The report also said Google and an investment firm that was not identified have reached a deal to fund a joint venture that would lease TPUs to other customers. It was separately reported by The Information that Meta has been developing its own AI chips, however it has been facing issues with design and recently discarded its most advanced chip and has instead shifted its focus to a less complicated version.

- OpenAI: OpenAI confirmed it has raised $110 billion in its latest funding round, including $50 billion from Amazon, $30 billion from Nvidia, and $30 billion from SoftBank, now valuing the company at $730 billion. With the news, the company said it has experienced a meaningful acceleration in subscriber momentum and now has more than 900 million weekly active users and over 50 million paying subscribers with 9 million business users.

- Uber: Uber said it is buying parking reservation app SpotHero Inc., an effort to continue expanding its customer base, though financial terms were not disclosed. SpotHero allows customers to find and reserve parking spots at more than 13,000 parking garages, lots, and valets across more than 400 cities in the US and Canada. It expects to integrate SpotHero’s features into the Uber app.

Other News:

- Tariffs: After the Supreme Court shot down Trump’s emergency tariffs (the tariffs announced last April), he used a different law to impose a 10% global tariff later that day at a press conference. It was also reported the US Customs and Border Protection sent a memo to importers informing them of a 10% tariff rate that would apply to every country for a period of 150 days starting at 12:01am Tuesday (February 24), which was confirmed by the White House. The Administration is also working on increasing that tariff to 15%.

- Credit Risks Concerns Rising: JPMorgan CEO Jamie Dimon received a lot of attention last week after comments on the economy and the risks banks and investors are taking. He warned some banks are doing “dumb things” to create higher interest income, adding that he is starting to see parallels to the era before the 2008 Financial Crisis. He said aggressive competition and lower credit standards are leading banks/lenders to take higher risks to boost profitability.

- Fed Talk:

- Fed Governor Christopher Waller said he does not know how to think about Fed policy when the economy is growing at the same time it isn’t creating additional jobs, calling last year’s job market the weakest non-recession year for jobs since 2002. He said if the trend continues its current path he sees a shift to a pause in rate cuts or if we see weaker job growth like last year, there is equally a case for rate cuts. Waller has historically been more dovish so this was a hawkish tilt.

- Chicago Fed President Austan Goolsbee said the progress on inflation has stopped and the Fed needs to pay attention, warning to his fellow policymakers inflation stalling at 3% is “not a safe place to be”. He added overall the economy is strong and driven by consumer spending though AI is another driver.

WFG News

Upcoming Events:

In March we will welcome a Social Security Specialist who will provide an overview of how Social Security works and discuss key strategies to help maximize your benefits.

Click the link below to RSVP today!

WFG Investment Classes:

Interested in learning more about investing and how the markets work? Wentz Financial Group holds various Investment Basics classes throughout the year. Contact us for details!

The Week Ahead

Investors will be focused on geopolitics this week and if the conflict in Iran escalates as well as the impact on the oil markets. On the earning’s calendar, focus moves to retailers with many big box stores reporting like Target, Best Buy, AutoZone, Abercrombie & Fitch, Kroger, Costco, and others like MongoDB, CrowdStrike, Box, Broadcom, Veeva, Okta, Ciena, and Marvell Technologies. Also on the corporate side is a pick up in brokerage conferences – these sometimes bring on notable company announcements. The first week of the new month brings on labor market reports. We will see ADP payroll report, jobless claims, and Friday’s monthly employment report where current consensus estimates 60,000 new jobs were added in the month. Other data comes from the PMI manufacturing index, the ISM manufacturing index, ISM services index, productivity and costs, and retail sales.