Wentz Weekly Insights

Fed Says Further Progress on Inflation Delayed Due to Tariffs

Thanks to a post-Fed meeting rally, stocks were able to squeeze out a positive week for the first time in over a month. The S&P 500 finished higher by 0.51% after Fed Chairman Powell indicated tariffs could end up being transitory while the Fed maintained its projections of two rate cuts for 2025. Once again consumer related stocks underperformed and on the index level, the more value weighted Dow index outperforming the more growth related Nasdaq index by 1%.

The bond market saw a small increase as yields fell across the curve. Most of the drop came Wednesday after the Fed meeting as policymakers at the Fed kept their projections of two rate cuts for both this year and next. Both the 2-year and 10-year Treasury yield fell six basis points to 3.97% and 4.26%, respectively. Both are down moderately from the beginning of the year due to the higher uncertainty around tariffs and their potential impact.

News flow and market volatility decreased last week with the main headline revolving around the Fed meeting that concluded Wednesday with no change in interest rates. It did make a policy adjustment by slowing the pace at which its Treasury holdings will mature off its balance sheet, from $25 billion per month to $5 billion per month effective in April (while keeping its agency security runoffs unchanged). It said it did this as a strategic response to prevent further disruptions due to the debt ceiling debate and ensure financial stability and liquidity.

The only other change to its policy statement was the Fed adding “uncertainty around” the economic outlook has increased, which replaced the wording about risks to the outlook being balanced.

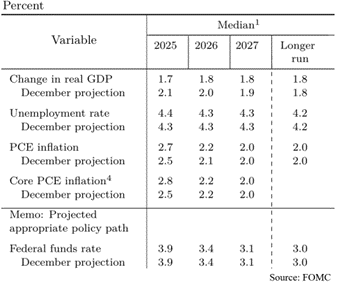

With the release of the statement was the updated Summary of Economic Projections (SEPs – where each of the 19 Fed officials give their projections on several economic indicators). See the chart below for the new projections compared to December. The updated projections showed a lower expectation on economic growth for 2025 of 1.7%, down from 2.1% (and down for 2026 and 2027), while inflation expectations moved up to 2.7% from 2.5% this year, and unemployment rate moved up to 4.4% from 4.3%.

Projections on interest rates were unchanged (Federal funds rate), with the average official projecting two rate cuts this year and two next year, with rates ending 2026 at 3.5%. However, there was a hawkish tilt compared to the December projections – the number expecting less than two cuts doubled from 4 to 8, while the number that see more than two cuts came down from 5 to 2.

Chairman Powell described these changes as a function of the additional uncertainty officials are seeing due to recent events. He made remarks on how the projections are a “challenging exercise.” Regarding the decision to reduce balance sheet runoff, he said it has nothing to do with monetary policy, it was more so done for financial stability.

The most pressing question was around tariffs and how it will impact inflation, the economy, and Fed policy. Powell added more context compared to his last message, saying it will be difficult to measure the precise amount of inflation that is coming from tariffs. Goods inflation moved up “pretty significantly” the first two months of the year but it is very challenging to track what portion of that came from tariffs, according to Powell. He added multiple times that tariff impacts may result in further progress on inflation being delayed. We would equate this to a delay in rate cuts (unless the unemployment picture deteriorates faster).

One of the more important questions was whether the impact to inflation would be a one-time event or would lead to persistent inflation. This is a key question because the pandemic inflation was thought to be “transitory” or one-time where the Fed ended up being wrong because inflation turned out to be more persistent. Again, Powell said it was too soon to know this, but they will rely on the data.

Also, there was a focus on hard data versus soft data – hard data being objective and quantifiable while soft data is survey-based and sentiment driven. Survey respondents have indicated a significant drop in sentiment and are saying they expect higher inflation in the short-term. The hard data on economic growth has continued to paint a solid picture, but household and business surveys show significant concerns about downside risks, but Powell downplayed the difference, saying the Fed will be following the data to see if worsening sentiment leads to softer hard data.

Overall, markets reacted positively, perhaps because they viewed the Fed’s thoughts on tariffs as more transitory, or perhaps because there was no change in rate cut projections. Either way, the focus in the short-term will likely be tariff headlines.

As for this week, stocks look like they are set to start the week on a positive note. A weekend report said Trump’s reciprocal tariff plan that is set to be announced April 2 will be more narrow and more focused than the full global effort that Trump has threatened over the past several weeks. However, the report from Bloomberg added Trump is still looking for immediate impact with his tariffs by planning to have them take effect right away.

We expect it to be a much more quiet week this week with markets in wait and see mode until next week’s reciprocal tariff announcement. There are a few economic data reports with a focus on sentiment surveys, housing, and the biggest report on Friday on consumer spending, income, and inflation.

Week in Review:

After a strong close to the week Friday, US stocks were able to generate a gain for the week for the first time in five weeks. The major US stock indices finished as follows: Dow +1.20%, Russell 2000 +0.63%, S&P 500 +0.51%, Nasdaq +0.17%. Treasury markets saw prices move slightly higher as yields moved lower which came mostly after the Fed meeting Wednesday. The 2-year Treasury yield and 10-year yield fell 6 basis points each to 3.97% and 4.26%, respectively. The dollar rose 0.4% while gold was up 0.8% to yet another new high, up for the 11th time in the past 12 weeks. Bitcoin was relatively unchanged. Oil rose 1.64%.

Recent Economic Data

- Retail Sales: Retail sales increased at a much slower rate than expected in February, rising 0.2% in the month compared to the 0.7% increase expected. In addition, January’s initial estimate of a 0.9% decline in sales was revised down to a 1.2% decline. Of the 13 major categories, 7 of them sale a decline in sales in the month led by a 1.5% decline in bars & restaurants, a 1.0% decline in gasoline sales, and a 0.6% decline in apparel. The largest increases were seen in online sales, health & personal care, and grocery stores. Gasoline tends to skew the headline number, excluding gasoline and vehicle sales, the core index increased 0.5% as expected. Retail sales were 3.1% higher from a year ago, barely growing if accounting for inflation.

- Housing Market Index: The housing market index, a measure of homebuilder sentiment, fell to 39 for March, down from 42 in February and back to the lowest level since late 2023 after a brief rise late last year. Conditions for sales, traffic, and expected sales all fell to the lowest level since the lows in late 2023. The index on present sales fell 3 points to 43, the index on expected sales the next six months was unchanged at 47, while the index of traffic of prospective buyers fell 5 points to a very depressed level of 24.

- Housing Starts: The number of housing starts in February saw a strong rebound after trending lower for much of 2024. The number of housing starts increased 11.2% in February to a seasonally adjusted annualized rate of 1.501 million, but was about 3% lower than the pace from a year ago. The number of permits was more disappointing, falling 1.2% in the month to an annual rate of 1.456 million, and down 7% from a year ago. The number of homes currently under construction has fallen to a multiyear low of 1.412 million units, down 15% from a year ago.

- Existing Home Sales: Existing home sales increased 4.2% in February to a seasonally adjusted annualized sales pace of 4.260 million homes, which is still 1.2% below the pace from a year ago. The National Association of Realtors Economist said in the report that even though mortgage rates have not changed much, more inventory and choices are releasing pent-up housing demand with buyers slowly coming back into the market. The supply of existing homes was up 5% in the month to 1.24 million homes, now up 17% from a year ago. The median price of an existing home was $398,400, up 3.8% from a year ago.

- Industrial Production: Industrial production increased 0.7% in February, higher than the 0.2% increase that was expected. The increase was led by a 2.8% increase in mining followed by a solid 0.9% increase in manufacturing output, and offset by a 2.5% decline in utilities which was likely due to a very cold January followed by a warmer February. Capacity utilization was 78.2%, rising to the highest since mid-2024.

- Empire State Manufacturing Index: The Empire State Manufacturing index was -20.0 for March, down from 5.7 last month and much lower than the 1.0 expected, signaling a significant drop in manufacturing activity in the past month for the New York region. The report noted employment levels and hours worked declined as new orders and shipments fell. Prices picked up pace once again, rising the fastest in two years.

- Philly Fed Manufacturing Index:The Philly Fed manufacturing index was 12.5 for March, down from 18.1 from February, suggesting manufacturing conditions in the Philly region expanded at a solid rate in the last two months, a completely opposite picture the Empire State survey has shown for the New York region (where the index has been negative). About 31% of firms that responded noted increased activity while 18% noted decreases in activity and the remainder noted no change. Employment improved again, reaching its highest level since October 2022, while the prices paid index was 48.3 for its highest level since July 2022, a not so welcoming sign on the inflation front.

- Jobless Claims: The number of unemployment claims the week ended March 15 was 223,000, a small increase from the prior week, with the four-week average relatively unchanged at 227,000. The number of continuing claims moved up 33k to 1.892 million but remains in a tight range of 1.820 – 1.900 million since July. The four-week average was up slightly to 1.876 million.

Company News

- Alphabet: Alphabet said it has agreed to acquire cybersecurity company Wiz for $32 billion, in its biggest acquisition ever, in effort to boost its cloud security offerings. It was last summer that Alphabet was close to a deal to purchase Wiz for around $23 billion, but talks ended over concern the deal would face issues with regulatory approval.

- PepsiCo: PepsiCo announced it has agreed to purchase prebiotic soda brand Poppi for $1.95 billion, in addition to potential earnout considerations subject to certain performance milestones. PepsiCo said it is part of its strategy to evolve its food and beverage portfolio with a leading brand in the fastest growing beverage category.

- TikTok/Oracle: Politico reported that discussions between the White House and Oracle on a potential takeover of TikTok are intensifying, but there are major concerns in what role the Chinese creators will play in continuing its operations in the US. One source said the U.S. government would have to depend on Oracle to supervise user’s data and make sure the Chinese government does not have backdoor access, adding that it was impossible to guarantee. A separate Bloomberg report the next day said Oracle is weighing a proposal where it would take a small stake in TikTok’s U.S. operations, which would be a new American entity, while leaving the company’s algorithms owned by China.

- BYD Company: BYD Company, a Chinese battery and auto company, revealed its Super e-Platform discovered a groundbreaking battery charging development where the new technology allows EVs (electric vehicles) to be charged at speeds comparable to filling a car with gasoline, recharging in as little as five minutes.

- Boeing: Boeing shares got a boost after the company said its cash outflows are likely to be “hundreds of millions” of dollars better than expected this quarter due to stabilizing work in its factories and the clearing out of its inventory of already-built planes.

- General Motors: GM deepened its partnership with Nvidia after both announced they will collaborate with each other on next-generation vehicles, factories, and robots, using AI, simulation, and accelerated computing. The news release notes GM has been investing in Nvidia’s GPU platform for training AI models across several areas including simulation and validation, but the expanded partnership will include using AI models for plant design and operations. GM will also use Nvidia technology for future driver-assistance systems.

- Apple: Apple’s streaming service, Apple TV+, has reached 45 million subscribers, the Information reported, adding despite the subscriber number it is still losing around $ 1billion annually. The report noted Apple has spent around $5 billion per year on content since 2019, but that has been moving lower lately as the company scrutinizes spending more after several high-profile movie flops.

Other News:

- Travel Disruptions: Europe saw massive travel disruptions from London’s main airport, the busiest in Europe and 4th busiest in the world, after a fire at a substation cut power to the whole airport with early reports saying the airport could see disruptions for days. Early reports say officials see no evidence of foul play.

- Central Bank News:

- The Bank of Japan held ready at 0.5% in its meeting last week as was expected, choosing to hold steady after its third rate increase in January. Officials said they are focused on the effects of rising global economic risks and how it would impact Japan’s economy, citing U.S. tariffs and challenging international conditions.

- The People’s Bank of China left rates unchanged.

- Riksbank (Sweden’s central bank) left rates unchanged and signaled it is at or near the end of its easing cycle.

- Swiss National Bank cut rates 25 bps to 0.25%, citing low inflationary pressure.

- The Bank of England left rates unchanged at 4.50%, with the statement noting global trade policy uncertainty intensifying, other geopolitical uncertainties increasing, and financial market volatility increasing, while indicating future rate cuts will be needed still.

- European Central Bank President said 25% tariff on US imports from the EU could subtract 0.3% from Euro area growth in the first year.

- Economic Pause: Treasury Secretary Bessent said he sees no reason the US will see a recession because the underlying economy is healthy, but did suggest the economy may see a “pause” as the administration decreases the “incredible level” of government spending.

- Department of Education: Last week President Trump signed an executive order calling for the closure of the Department of Education, citing its massive budget and no results to show for it saying “the United States spends more money per pupil than any country, yet we rank near the bottom of the list in terms of success.” The order will direct the Education Secretary to take all steps to facilitate the closure of the Department and return all education authority to the states. However, this will require Congress approval with a 60 vote where Republicans hold a current 53-47 majority.

- Russia Ukraine Negotiations: Trump had a call with Putin Tuesday night where Putin agreed on steps toward a total ceasefire and peace deal to end the Ukraine war, agreeing to an energy and infrastructure ceasefire where both sides would refrain from attacking each other’s infrastructure for at least 30 days. The Trump Administration is considering recognizing Crimea as Russian territory in bid to end war, according to a Semafor report that cites two people familiar with the matter and has urged the United Nations to do the same.

Did You Know…?

Covid Bear Market 5 Year Anniversary

Yesterday, Sunday March 23, marks the five year anniversary of the bottom for stocks during the Covid-induced bear market. Prior to the Covid pandemic, stocks (as measured by the S&P 500) peaked on February 19, 2020 at 3,393.52. As the economy came to a standstill and over concerns of a deep economic recession, the index fell to a bottom of 2,191.86 on March 23, 2020, a 35.4% drop, the fastest decline stocks have ever seen. However, as the government stepped in to support individuals and businesses, and as investors realized it was a voluntary lockdown of the economy and demand would only be pushed into the future, stocks experienced one of the sharpest recoveries we have seen on record. By August, stocks had recovered all of the losses, rising 55% from the lows. The anniversary serves a great reminder to investors and retirement savers that it is important to keep your long-term investment and retirement objectives in mind, especially in times of volatile periods, and how important it is to avoid making emotional decisions, despite how hard it may feel. While market drawdowns cause a lot of worry, for long-term investors it should also be looked at as opportunity. For example, since the bottom March 2020, stocks are up 159% for one of the best 5-year periods (and up 180.5% from the March 2020 bottom to the record high reached last month!) The chart below shows the S&P 500 since January 1, 2019. As you can see the March 2020 decline was short lived and over a longer-term scale the decline appears much smaller.

Largest North America Sports Deal

The Boston Celtics basketball team was sold last week in the largest sports deal ever in North America. William Chisholm, managing partner at private equity firm Symphony Technology Group, agreed to purchase the team for $6.1 billion from Boston Basketball Partners, who decided to sell the team last year and was seeking offers. Boston Basketball Partners bought the team in 2002 for $360 million.

WFG News

Tax Documents

Please see this release to understand the timing on when to expect tax documents.

The Week Ahead

The calendar is much more quiet this week and market participants will most likely be in holding mode until next week’s reciprocal tariff decision deadline April 2. Perhaps the most anticipated event his week is Friday’s personal income and outlays economic data report that includes data for February on consumer spending, income, and the most important inflation reading the PCE price index. Other data releases include new home sales, pending home sales index, the Case-Shiller home price index, money supply, durable goods orders, jobless claims, the final Q4 GDP revision, consumer confidence, and consumer sentiment. The earnings calendar is light, with the only notable companies reporting being KB Homes, McCormick, GameStop, Chewy, Dollar Tree, and Lululemon. The number of brokerage conference will remain higher than usual this week but less than the past couple weeks. With the Fed out of its blackout period after last week’s Fed meeting, we should see a number of Fed officials give public comments on policy. Finally, on the geopolitical side, US and Ukraine negotiators are meeting followed by US and Russia at the beginning of the week for a second round of negotiations to end the Russia Ukraine war.