Wentz Weekly Insights

Anticipated “Liberation Day” Leads to More Volatility

Markets moved lower in another week that was dominated by uncertainty around the level, timing, and economic and inflationary impacts of tariffs. It was another week that saw defensive sectors outperform, with consumer staples up 1.7% and energy up 0.8% while technology fell 3.7%. Mega cap tech companies continue to give up some gains made over the past two years. In fact, the “Mag 7” stocks have now underperformed the S&P 500 index for 12 of the last 13 weeks.

There could be several reasons for the rotation out of Mag 7, including profit taking after the stock’s substantial gains the past two years, hedge funds de-leveraging, and increasing skepticism around artificial intelligence.

In the second instance over the past couple weeks, an analyst report noted Microsoft was scaling back some of its data center plans, creating worries that the industry is getting oversupplied. Microsoft and hyperscaler competitors Amazon, Meta, and Google, have said they plan to spend over $300 billion in 2025 to build out data centers, which house the advanced chips that power AI. A cut in investment spending would be a big disappointment for many involved in the industry with so much growth baked into stock prices.

In addition, a Financial Times report said Nvidia could see a $17 billion impact on revenues if China moves forward with enforcing stricter energy efficiency rules for use of advanced chips, about 13% of Nvidia’s last 12 month of revenues.

The bigger impact on markets since January has been tariff related. Last week’s headline on tariffs came mid-week when President Trump signed an executive order and held a news conference to announce a 25% tariff on all vehicles manufactured outside the U.S., which is set to become effect April 2. The tariffs will start at 2.5% and gradually rise to 25% to be applied to imports of both cars and foreign parts. He said the order is expected to generate $100 billion in revenue.

There was more focus last week on the inflation impact of these tariff announcements. Some analysts have said the vehicle tariffs could push up the price of new cars by an average of $5k-$10k (Wedbush), while the used car market could see inflation of 10% in the near-term (JPMorgan).

We have also seen more direct comments from Fed officials on potential tariff impacts. Atlanta Fed President Bostic said he now only sees one rate cut this year due to tariffs slowing the Fed’s inflation progress, adding that tariffs historically have a one-time price impact, but this time we may see a prolonged effect from higher price growth. Meanwhile, Boston’s Susan Collins said it is “inevitable” that tariffs will boost inflation which makes it more appropriate to keep rates at these higher levels for longer.

The most recent PCE price index, the Fed’s favorite inflation report, came out Friday that suggested inflation was slightly higher than expected in February, rising 0.3% and up 2.5% from a year ago, while core prices increased 0.4% and its annual increase ticked up to 2.8%.

Not only are tariffs causing inflation worries, but also growth worries. That comes at a time growth is already slowing. As we mentioned in recent newsletters and was a large topic from our 2025 Economic Outlook meeting in January, the substantial cut to government spending that is expected from the new administration will be a small shock and lower economic growth considerably. But tariffs may also bring a slowdown to growth. We are even starting to hear more worries about stagflation – an environment where the economy sees little or no growth and high inflation.

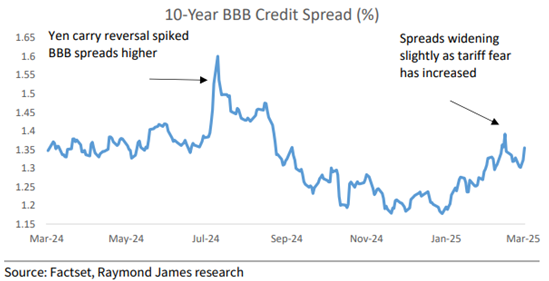

While this is a potential concern, it hasn’t reached levels that are worrisome yet and have not impacted prices of securities yet. Spreads on high yields or junk bonds are a good example as shown in the chart below. This shows the addition yield an investor receives on a BBB rated (junk rated) bond over an investment grade bond of the same maturity. The spread is currently 1.17%, remaining in a tight range, and still well below the 2%-4% spread that indicates fear and recessionary scenarios.

The next big tariff announcement comes this Wednesday with what Trump is calling “Liberation Day.” Trump is expected to announce his reciprocal tariff plan after giving his administration several weeks to study current trade relations and propose reciprocal tariffs on a country-by-country basis.

It is also a big data week with updates on the labor market. The first report is Tuesday with the job openings and labor turnover survey, followed by ADP’s payroll numbers, and Friday’s DOL labor report. Current estimates see 130,000 new jobs were added in March, a slowdown from recent months. It is also the first jobs report that will fully capture the recent efforts from DOGE.

Week in Review:

Stocks saw continued downward pressure over ongoing tariff headlines and worries over its impact to inflation and the economy. The four major U.S. stock indexes finished the week as follows: Dow -0.96%, S&P 500 -1.53%, Russell 2000 -1.64%, and Nasdaq -2.59%. The bond market was relatively unchanged with the 2-year Treasury yield falling 5 basis points to 3.92% while the 10-year yield fell 2 basis points to 4.24%. The dollar index was relatively unchanged for the week after falling about 5.3% from recent highs. Gold rose 2.26% to another new record. Bitcoin was level with a 0.37% increase. Oil rose 1.58% for its third straight weekly gain on Venezuela sanctions.

Recent Economic Data

- Personal Income & Outlays: The personal income and outlays report included a couple surprising numbers – in February incomes rose at a much faster pace than expected and inflation was slightly higher than expected while the annual rate ticked higher.

- Personal income rose 0.8% in February, double the expectation of a 0.4% increase, and follows a large 0.7% increase from January. Incomes are now up 7.7% over the past year, running about 3x the rate of inflation. Wages and salaries rose just 0.4% and were up 4.6% from a year ago. It seems government transfer payments are driving most of the increase with the category up 2.2% in the month and a very large 13.3% over the past year.

- Consumer spending increased 0.4% in the month, slightly lower than expected, while January’s 0.2% decline was revised down to a 0.3% decline. Spending is still up a solid 6.8% from a year ago, but as the data shows has slowed substantially to start 2025. Goods spending rose 0.9% (possibly consumers buying ahead of potential tariff impact on prices) and are up 2.8% over the past year while services spending rose 0.2% and up 8.5% over the past year.

- The personal savings rate increased to 4.6% up from 3.3% just two months ago, which is most likely due to weakened consumer sentiment that resulted in less spending and more saving. The savings rate is still about 3% below the historical average.

- On the inflation side – the PCE price index rose 0.3% and is up 2.5% from a year ago, both matching January’s increase. The core PCE index increased 0.4% which was more than expected and up 2.8% from a year ago, an uptick from 2.6% last month.

- Case-Shiller Home Price Index:The Case-Shiller home price index indicated home prices increased 0.5% seasonally adjusted in January which matches December’s increase (increasing 0.1% prior to seasonal adjustments). Over the past year, home prices are up by 4.1%, with the bulk of the increase happening in the first six months (while the last six months prices are down 0.7%), up from the 4.0% annual gain the prior month. The areas of the US seeing the fastest growth in prices include Midwest and Northeast regions like New York up 7.6%, Chicago up 7.5%, and Boston and Cleveland up 6.5% over the past year, while the lowest growth was in the South and West like Tampa down 1.5%, and Dallas and Denver up less than 2%.

- New Home Sales: Sales of newly built homes increased 1.8% in February to a seasonally adjusted annualized rate of 676,000, up 5.1% from a year ago. The trend in new home sales has been in the 600,000’s range for two years now, after seeing a brief spike of over 1 million after the pandemic. However, new homes are what is needed due to the large shortage in housing supply. The issue since the pandemic has been affordability with higher home prices and mortgage rates. The good news is prices of new homes are down 1.5% from a year ago with the median price at $414,500 (and down 10% from the peak October 2022). The other good news is inventory of new homes is up 8.1% from a year ago at 494,000 homes. The new home market is improving more than the existing home market, where there are more significant supply issues as current home owners are reluctant to give up their low mortgage rates they locked in during the pandemic.

- Durable Goods Orders: Orders of durable goods, one of the big inputs to factory orders and business investment in GDP, increased 0.9% in February – much better than the 1.0% decline that was expected, and follows a quite strong 3.3% gain in January. Excluding transportation, orders were up 0.7%, but the report wasn’t all that good as core capital goods orders fell 0.3%. Perhaps it is tariff related, with categories such as metals seeing big increases. The figure that is used for GDP, shipments of nondefense core capital goods excluding aircraft, was solid with a 0.9% monthly increase.

- Money Supply: The amount of money in circulation, called the money supply which includes cash, deposits at banks and money market balances, increased $93.9 billion in February, or 0.4% and is up $809.4 billion over the past year, or 3.9%. Money supply saw a record $6.32 trillion, or 41%, increase from the beginning of the pandemic to 2022, the root cause of inflation. Since then it moved lower for a brief period but has now began increasing at a faster pace than normal, which should keep upward pressure on inflation.

- Jobless Claims: The number of unemployment claims the week ended March 22 was 224,000, a relatively small decline from the week prior. The four-week average fell 5k to 224,000. The number of continuing claims was 1.856 million, down 25k from the prior week, with the four-week average up slightly to 1.870 million.

- Consumer Confidence: Consumer confidence has taken a significant hit over the past couple months and in March it deteriorated further. The Conference Board’s consumer confidence index was 92.9 in March, down 7.2 points from February and down from the narrow range it has been in since 2022, for the lowest level since January 2021. The present situations index fell 3.6 points to 134.5 while the expectations index fell 9.6 points to 65.2 for the lowest level in 12 years (even below pandemic levels!) and is well below the threshold of 80 that usually signals recession. The report noted the decline in confidence was likely a response to recent market volatility and tariff news.

Company News

- Apple: A Bloomberg report said Apple is exploring adding cameras and Visual Intelligence features to its smartwatch and would expect it to be rolled out by 2027. The upgrades would allow users to use camera features to look up details about a location, identify things, translate/summarize text, among others. The camera would most likely be fitted in the display part of the watch, similar to the iPhone’s front facing lens. In addition, it is considering adding cameras to AirPods to power AI features. The report added Apple will need to upgrade its Artificial Intelligence to make these integrations more useful.

- 23andMe: DNA genetic testing company 23andMe has filed for bankruptcy protection, after having once been a $6 billion market capitalization company at its peak in 2021. The company had once hoped to use the DNA tests to develop drugs that were tailored to its research and even had the FDA on its side. However, persistent losses, a lack of successful follow-up products and repeat customers/recurring revenue, and a massive data breach led to a loss of trust in the company and its ultimate fate.

- Boeing: Boeing received a multi-billion dollar contract (which could reach up to $50 billion over the life of the contract) from the Department of Defense to lead the development of the Air Force’s next gen fighter jet, the F-47, according to the WSJ.

- Dollar Tree: With its earnings release, Dollar Tree said it reached an agreement to sell its Family Dollar business to a private equity consortium for $1 billion. Family Dollar was acquired by Dollar Tree in 2015 for $9 billion.

- Under Armour: Under Armour said it has signed a deal with the NFL to be the official provider of footwear and gloves in a multiyear deal. The deal gives Under Armour rights to include logos on shoes and gloves worn during games for the first time since its prior deal ended in 2020.

- OpenAI: OpenAI revenues are expected to more than triple in 2025 to reach $12.7 billion, according to a Bloomberg report. The report added the company expects momentum in revenue growth to continue with 2026 revenue hitting nearly $30 billion which would be a 136% increase from 2025. However, the company is still operating at a massive loss, on track to lose $5 billion in 2024. A separate Bloomberg report said the company had a valuation of $300 billion based on the recent funding round that raised $40 billion, up from a $157 billion valuation in its prior funding round. This would rank the company as one of the largest private company investments ever.

- Nvidia: A report from the Financial Times said Nvidia could see a $17 billion impact on revenues if China moves forward with enforcing stricter energy efficiency rules for use of advanced chips. The $17 billion figure makes up about 13% of Nvidia’s trailing twelve months revenue.

- Microsoft: Microsoft and other AI related stocks fell last Wednesday after an analyst report from TD Cowen said Microsoft was scaling back some of its data center plans. It said the pullback on new data center capacity was driven by Microsoft’s decision to not support incremental OpenAI training workloads. It said it believes the cancellations point to data center oversupply relative to current demand forecasts. This was the second report he past several weeks of Microsoft cutting capacity growth plans.

- X: Elon Musk said in a post on X that X.AI, an AI lab that builds models and data centers, has acquired X in an all-stock transaction that values X at $33 billion. The post said it makes it the official step in combining the data, models, compute, distribution, and talent, and said the deal will unlock potential by blending xAI’s advanced AI capabilities and expertise with X’s massive reach.

Other News:

- U.S Fiscal Outlook Weakens:Credit rating agency Moody’s said the fiscal strength of the U.S. has “deteriorated further.” This comes just one and a half years after the country’s debt rating was hit with a negative outlook. Its report said higher interest rates have weakened debt affordability and has accelerated the decline in fiscal strength. Moody’s forecasts a rising pace of deterioration with interest payments-to-revenue increasing to 30% by 2035 from 9% in 2021. It also said sustained high tariffs, unfunded tax cuts, and significant tail risks to the economy could result in less effective U.S. strength in global finance.

- Government Deadline: The Congressional Budget Office (CBO) said the government’s ability to borrow under extraordinary measures is estimated to be exhausted by August or September, which is the time the government runs out of cash to continue operating. Congress must find an agreement on raising the debt limit by this deadline to continue paying its obligations and to avoid defaulting on its debt.

- Privatizing Freddie Mac & Fannie Mae: Trump is considering signing an executive order that would have federal agencies evaluate the idea of privatizing Fannie Mae and Freddie Mac. The two are government sponsored enterprises (GSE) that buy mortgages from lenders and bundles them into mortgage-backed securities to sell to investors and is crucial in helping keep money flowing in the mortgage markets. Some in the administration are even considering transferring the government’s stake in each to its proposed sovereign wealth fund. Privatizing the two could lower costs for the government but may also push up mortgage costs from investors demanding more return.

- Fed updates:

- Atlanta Fed President Bostic says he now sees only one rate cut this year due to tariff increases slowing the Fed’s progress of lowering inflation. He added while tariffs historically have been a one-time impact on prices (transitory), this time we may have a prolonged effect from higher price growth.

- Fed Governor Kugler said recent data on goods inflation was “unhelpful” and impacts expectations while noting the recent economic data shows weakness.

- Minneapolis Fed President Kashkari said progress has been made on lowering inflation, but a lot of work remains, and unpredictable fiscal policies are muddying the Fed’s outlook. He commented on the recent drop in consumer confidence saying outside March 2020 during Covid it is the most dramatic shift in confidence he has experienced, but attributed it to uncertainty around tariffs, adding the shift in confidence makes him more concerned than the tariffs itself.

- Boston Fed President Susan Collins said it is “inevitable” that tariffs will boost inflation, at least in the near term, which makes it likely appropriate to keep rates at these levels for longer. She said tariff-driven inflation could be short lived, but it may make price pressures more persistent.

- Tariff news:

- The tariff headline last week was President Trump’s news conference where he signed an executive order stating the U.S. will impose tariffs of 25% on all vehicles manufactured outside of the U.S. to be effective April 2. He said the tariffs are projected to raise $100 billion in revenue. The tariff will start at 2.5% and gradually rise to 25% and will apply to both cars and foreign parts imported.

- A Bloomberg last weekend said Trump’s reciprocal tariff plans expected to be announced this week will be more targeted than what he has recently threatened. It added the administration does not intend to unveil separate, sector-specific tariffs at the same time. However, one source said Trump is hoping to get immediate impacts from the tariffs.

- Trump later said at the beginning of the week “I may give a lot of countries breaks” on reciprocal tariffs, but when asked for clarification said “yeah it’s going to be everything, but now all tariffs are included that day.”

- Trump said during a news conference last week that he would consider lowering tariffs on China if it meant it would help facilitate a deal that would involve ByteDance selling TikTok’s U.S. operations, saying TikTok is big, but every point in tariffs is worth more than TikTok. The app faces another deadline of April 5 to make the sale or be banned in the U.S., but Trump said he is willing to extend the deadline again.

- Venezuela tariffs: Oil moved higher after Trump said the U.S. will put a 25% tariff on any country that buys oil from Venezuela starting April 2 due to Venezuela sending the US “tens of thousands of criminals, many of whom are murderers and people of a very violent nature.”

- India is considering cutting its tariffs on over half its imports from the U.S., which is valued at $23 billion in goods, in effort to protect its exports to the U.S., which is valued at about $66 billion, which is sees at risk due to the expected reciprocal tariffs on April 2. The Reuters report says India is willing to cut tariffs on 55% of its U.S. imports, which currently see tariffs between 5% and 30%.

- Trump said he would place far greater tariffs on the EU and Canada if they collaborate to do economic harm to the U.S.

- Russia/Ukraine: After two days of talks, the U.S. said it would help Russia increase agricultural exports and it would restore access to payments systems in return for a ceasefire in the Black Sea, after Russia negotiators demanded the easing of certain sanctions. European allies imposed many of these sanctions and have vowed to keep them in place, created a standoff between the U.S.

WFG News

Tax Documents

Please see this release to understand the timing on when to expect tax documents

Investment 101 Class

Interested in learning more about the basics of investing and how the markets work? Join us in our next Investment 101 class on April 15 at 4:00pm!

This is a great opportunity to learn in a small setting about key financial principals, like risk and return, liquidity, inflation, diversification, growth versus income, time value of money, account types, and how your money can work harder for you!

The Week Ahead

The much anticipated “Liberation Day” will come April 2 and is expected to be one of the major headlines this week where President Trump is expected to announce his full reciprocal tariff plans. Recent comments suggest the tariff announcement will be toned down, but it is unclear how much and whether it is just the first of a series of announcements. On the economic calendar, the highlight will be data on the labor market including the job openings and labor turnover survey, ADP’s payroll numbers, jobless claims, and the employment report on Friday. Consensus estimates see 131,000 new jobs added for March, a slowdown from recent months. We will also see the PMI and ISM manufacturing indexes, factory orders, construction spending, February trade data, and the ISM services index. The earnings calendar is very light again, with the only notable quarterly results coming from PVH, RH, BlackBerry, and Conagra. The Brokerage conference calendar continues, with a focus on medical and drug conferences, and there are a couple IPOs (initial public offering) expected. Finally, on the Fed side there will be several Fed officials with public appearances this week including a speech by Chairman Powell late Friday morning at the University of Chicago’s Booth School of Business 2025 U.S. Monetary Policy Forum.