Wentz Weekly: Quiet Week Pushes Stocks Into New Bull Market, Fed Meeting Ahead

Wentz Weekly Insights Quiet Week Pushes Stocks Into New Bull Market, Fed Meeting Ahead

US markets finished the week positive overall, with small caps outperforming for the first time in weeks with a 1.90% gain in the Russell 2000 (an index of 2,000 of the smallest companies in the Russell 3000, which is a broad measure of the US stock market based off 3,000 stocks, representing 96% of the US equity market). The S&P 500 finished the week up 0.39% and after Thursday’s 0.62% increase, it was enough to push the index into a new bull market. A bull market is commonly referred to a 20% increase in stocks from recent lows. It was one of the more quiet weeks we have seen in some time and with no headlines, the path of least resistance has been to the upside. It is also important to note that rallies like this are not uncommon in bear markets, as Raymond James notes, a rally of at least 20% happen three separate times in the 2001-2002 bear market.

The reason for the bull market is based on a number of things, but most notably has been driven by the top eight names in the index – Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, Berkshire Hathaway, and Facebook parent Meta. Based on our calculations, the average performance of these stocks this year is 69.4% (this is not a typo). While the S&P 500 index is up 11.9% this year as of Friday, these eight stocks have driven 16.6% of the S&P 500 performance this year alone. With the S&P 500 up 11.9% and the top eight stocks making up a 16.6% gain for the S&P 500, the average stock is still down this year.

This performance is not sustainable and we don’t believe it will last much longer. The rally in growth stocks is coming from the market’s expectation of a pivot in Fed policy at some point later this year, from increase rates in the first half of the year to cutting rates by the end of the year (growth stocks typically outperform in a lower rate environment), and the recent hype in artificial intelligence (AI) with things like chatbots and machine learning.

This week investors will get a better idea on how the Fed sees the path forward on interest rates, as well as how much progress we are making on the inflation front. The consumer price index for May will be released on Tuesday morning. Consumer inflation is coming down on the headline level, with a 0.2% increase in the index expected, but the “core” index, which excludes categories that see more frequent fluctuations in prices like oil/gas, is expected to have increased another 0.4% in the month, while still being 5.3% higher than a year ago. This is well over the Fed’s target of 2%.

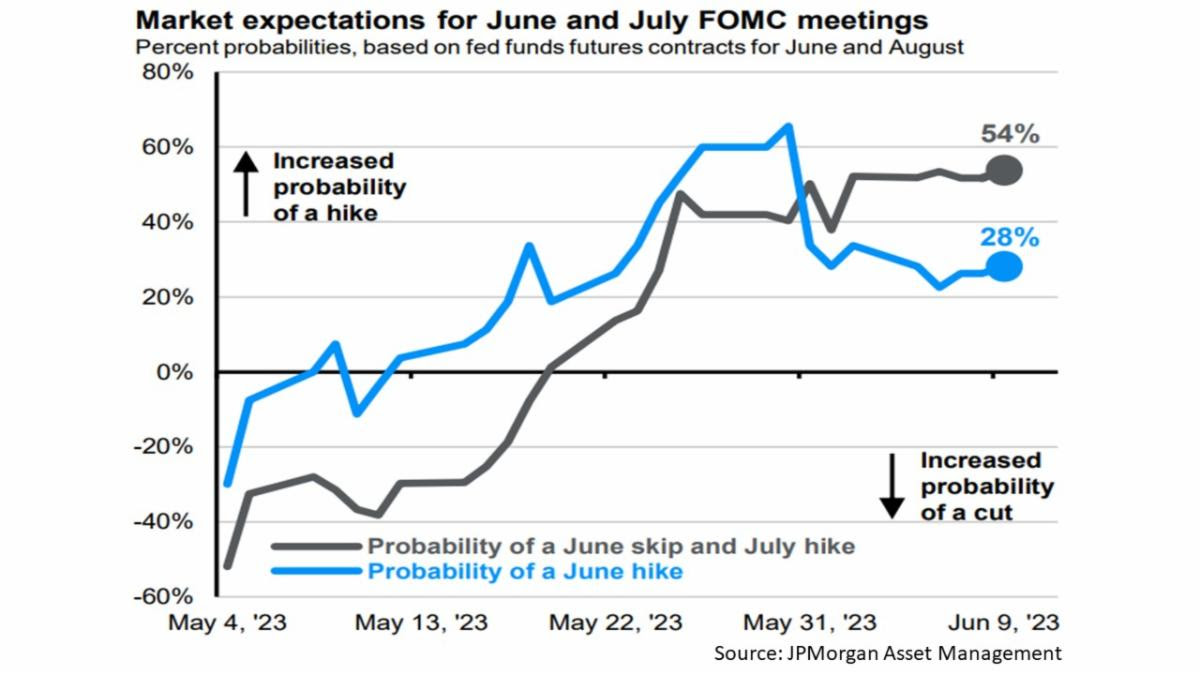

Because of this, the Fed may give a more hawkish message that it is to remain tough on its fight on inflation. As the chart below helps illustrate, even though it may not raise rates – future pricing sees only a 30% probability it will – it may signal that the rate hike cycle is not over and a rate increase at the July meeting will be on the table. The odds of a July rate hike are at 70%, and this moved higher after the central bank of Canada and Australia surprised markets with an unexpected rate increase at their respective policy meetings last week. Markets were previously expecting, just a month ago, that the Fed would look to begin cutting rates as soon as July to boost an economy that was expected to begin contracting.

What will be equally important in our opinion is the Fed’s updated projections on economic growth, inflation, unemployment, and policy rates via the “dot plot” in the Summary of Economic Projections. The Fed releases these projections every other meeting (roughly every 13 weeks) and in its most recent March release were saying rates would reach peak levels after its May increase to 5.10%, which is where they currently stand. However, recently officials have indicated further rate increases will be necessary so it is very likely those projections will move higher. It will be interesting to see when, and by how much, policy rates are projected to come down. Previously, policymakers said this would happen sometime in 2024.

Inflation was expected to move down to a 3.3% annual rate by the end of this year, versus the most recent 4.4% reading, while core prices were projected to fall to an annual rate of 3.6%, down from the most recent reading of 4.7%. At every SEP over the past year, policymakers have had to increase their projections for policy rates and inflation, and we think this release will be no different based on data that shows inflation has remained stubbornly high.

Coming off a quiet week and stocks now approaching more overbought levels, we don’t see much more upside left in this rally and reversion is expected in markets. There is also a small concern of a liquidity issue due to the Treasury needing to replenish its general account after running it close to zero from the debt ceiling debate. The general account is typically kept at around $450 billion and the Treasury said it expects it to be $425 billion by the end of the month meaning billions in new issuance of Treasury notes. When the Treasury issues new bonds it takes liquidity out of the system. History shows a strong negative correlation between the Treasury general account balance and stock prices.

While this could create short-term volatility, our eyes will be on the Fed meeting to gain a better understanding on Fed policy for the remainder of 2023.

Week in Review:

It was a slow start to the week for stocks after they came off a three week winning streak. The week was expected to be a quiet one with very little economic data, earning releases, political noise, and Fed speak. The highlight on Monday was the decision from OPEC+ to hold oil production and previously announced levels, although Saudis announced additional voluntary cuts to productions. This had oil higher initially over a potential drop in supply, but it only finished the day up 0.6%. The ISM services index in the morning was below expectations indicating slowing activity in the services sector, but still expanding. On the corporate side, Apple held its Worldwide Developers Conference where it unveiled its VR headset the Vision Pro. Stocks were lower across the board with small caps underperforming and the S&P 500 down 0.20%.

Cryptocurrency dominated Tuesday’s headlines with the SEC filing a lawsuit against crypto exchanges Binance and Coinbase over violation of securities regulations, manipulating trading, and mishandling customer funds. Outside of this news it was another quiet day. In global central bank news the Reserve Bank of Australia unexpectedly raised rates another 25 basis points. Treasuries were little changed while small caps had a big day. The volatility index, the VIX, fell below 14 during the session for its lowest level since before the pandemic started, January 2020. The Russell 200 small cap index rose 2.69% while the S&P 500 rose just 0.24%.

Wednesday morning there was another surprise interest rate increase by a central bank, this time coming from the Bank of Canada which raised rates 25 basis points, due to “stubbornly high” inflation, after two consecutive meetings of making no changes. It was another quiet day but there was a big shift in leaders in the stock market – the NASADQ fell 1.29% as semiconductors and software names struggled while the small cap index (Russell 2000) rose 1.78%. Treasury yields rose across the curve over more hawkish global central banks with the 2-year back to 4.58%.

The quiet trend continued on Thursday with no major headlines, but jobless claims in the morning ticked up to 261,000 initial claims, the highest weekly count since October 2021. Some of the largest companies performed better, driving the S&P 500 0.62% higher while small caps were back to underperforming with a 0.41% decline on the day and Treasury yields falling slightly.

Friday was another quiet day. There were no data releases and a lack of other headlines. Stocks did well although small caps were down and breadth was weak with more declining stocks than advancers. The S&P 500 moved over 4,300 briefly before stepping back and closing below that level with a 0.11% increase and officially entered a bull market (gain of at least 20% from the recent lows).

It was a very quiet week as stocks finished higher for the fourth consecutive week with the NASDAQ seeing its seventh consecutive weekly gain, the longest winning streak since November 2019. The major US stock indices finished the week as follows: Russell 2000 +1.90%, S&P 500 +0.39%, Dow +0.34%, and NASDAQ +0.14%. Treasuries were slightly weaker for the week with yields rising, more so on the short end. The 2-year note’s yield rose nine basis points to 4.61% for the highest level since March, prior to the banking issues, while the 10-year yield rose to 3.72%. Gold finished up 0.4%, oil was down 2.2% despite Saudis voluntarily cutting oil output, and the dollar was down slightly.

Recent Economic Data

New orders for manufactured goods increased 0.4% in April for the fourth increase in the past five months, but only half the increase that was expected. However shipments were down for the fifth month of the past six, declining 0.4% in April. Durable goods orders were up 1.1% which drove most of the increase in orders, but this was driven by transportation more specifically aircraft orders which are large orders and skew the index most times.

The ISM non-manufacturing survey index, an index of general business conditions based on the services sector, deteriorated further in May to 50.3, down from 51.9 in April and two points below expectations. The survey indicated growth in the services sector, but very little growth as a reading below 50 suggests declining activity. Most of the indicators declined from April levels in May, with the two most important – new orders and business activity – both falling in May. Employment fell into contraction territory, but good news is the prices index declined as well, the index on prices still elevated but falling to 56.2 from 59.6 in the prior month for the lowest since May 2020. However, price increases are still happening with 12 of the 18 industries in the survey reporting higher prices in May.

The US trade deficit had shrunk in recent months, but in April it expanded again to $74.6 billion for the month, up from a deficit of $60.6 billion in March. The increase was due to a $9.2 billion, or 3.6% decline in exports (total of $249.0 billion) while imports increased $4.8 billion, or 1.5% (total of $323.6 billion). That is positive for the US economy as it shows demand is still strong, but an unusually large drop in exports. Through the first four months of the year the deficit is 23.9% lower, or $86.5 billion lower, from the same first four months of 2022, due to exports rising 5.8% and imports decreasing 2.3% from 2022 levels.

The number of unemployment claims filed to states for the week ended June 3 was 261,000, a jump of 28k from the prior week for the highest level of initial claims since October 2021. The four-week average was 237,250, up 7.5k from the prior week. The number of continuing claims was 1.757 million, down 37k from the prior week with the four-week average at 1.785 million.

The Fed’s monthly report on consumer credit showed total credit carried by US consumers rose at a seasonally adjusted annual rate of 5.7% in April, the same pace as March (on a non-seasonally adjusted basis was up an annual rate of 6.4%). Total outstanding credit is $4.860 Trillion. Again, revolving credit like credit cards is seeing a large increase and driving most of the increase with an adjusted annual rate of 13.1% in the month (non-seasonally adjusted up 15.8% annually) while nonrevolving credit like mortgages, auto loans, etc, rose 3.2%. Revolving credit makes up 25.6% of all consumer credit versus pre-pandemic when it accounted for 23.3% of all credit.

The average 30 year prime mortgage rate declined for the first time in four weeks, falling 8 basis points to 6.71%, though still near the highs of the year, according to Freddie Mac’s mortgage survey. Its Chief Economist said while affordability remains challenging, inventories continue to be the biggest obstacle for prospective homebuyers.

Company News

Apple held its Worldwide Developer Conference Monday where it unveiled its first new product in almost ten years. It announced its virtual reality headset, the Apple Vision Pro which will be available early 2024 and will sell for $3,499 and will come with its own operating system (visionOS) and app store. It also announced a new Mac and operating system updates. The event and its announcements were as expected, according to analysts. Reports say Apple is projecting 500k-1million unit sales per year for its Vision Pro. The stock made a new all-time high during the conference and was just 7% away from reaching a $3 trillion market cap (was only 4% away at the highs). With today’s market cap it makes up roughly 8% of the S&P 500’s total market cap.

GM said it will invest at least $1 billion in two Michigan plants to produce its new next-generate heavy duty trucks (its gas and diesel trucks). This comes despite its commitment to offer all electric vehicles by 2035 as demand for its pickups remains strong.

Days after announcing a deal with Ford, GM said it reached an agreement with Tesla where GM Electric vehicles will be able to utilize Tesla’s Superchargers across the country. Similar to Ford, GM EVs will need to use an adaptor to access the Supercharger stations, but GM (like Ford) will integrate the connector design into its vehicles by 2025.

Boeing said it is delaying deliveries of its 787 Dreamliner after it found defects in its parts during its production. It said this will delay deliveries by about two weeks. It has consistently dealt with production issues since the two 737 MAX plane crashes several years ago, most recently earlier this year it had a delay due to problems on a fuselage component.

Tesla said, and it was later confirmed on a government website, an update to vehicle eligibility allows its Model 3 sedan to be fully eligible for the full US tax credit of $7,500.

The SEC has filed a lawsuit against cryptocurrency exchange Binance and Coinbase. The lawsuit against Binance said the company violated securities regulations by mishandling customer funds and secretly sending them to a separate entity controlled by the CEO as well as deceiving investors about the sufficiency of its systems and misleading its investors about its risk controls and manipulating trading. Its suing Coinbase over the company operating as an unregistered securities broker since at least 2019. The SEC says digital tokens like Bitcoin qualify as securities rather than currency.

Other News

Treasury Secretary Janet Yellen said in an interview that US banks could be pressured by a weakening commercial real estate market and are most likely preparing for the difficulties they will face in the months ahead. Strategists have made similar comments recently, suggesting the commercial real estate market could be the catalyst that pushes the economy into a recession.

The Reserve Bank of Australia unexpectedly raised interest rates another 25 basis points to 4.10%. The expectation was for a pause in rate hikes, but the central bank Governor said inflation is “still too high” and “services price inflation is still very high and is proving to be very persistent overseas.” He also said further policy tightening may be needed.

Similar to the Reserve Bank of Australia, on Wednesday the Bank of Canada unexpectedly raised interest rates by 25 basis points to 4.75%, this coming after it paused rate hikes for two meetings, and made no changes to its quantitative tightening (QT). It said the reason for the increase was underlying inflation remains “stubbornly high” and that policy was not sufficiently restrictive enough as global central banks have to raise rates “further to restore price stability.” Canada’s CPI unexpectedly moved higher in April to 4.4% for the first increase in 10 months.

Did You Know…?

Household Net Worth

U.S. household net worth increased 2.1% during the first quarter 2023 to $148.8 trillion as a rise in equity prices (+$2.4 trillion) more than offset the decline in real estate valuations (-$0.6 trillion) in the quarter. Household debt rose at an annual rate of 2.2% in the quarter while consumer credit debt like revolving debt increased at a 4.3% annual rate.

New Bull Market

After a 0.68% gain in Thursday’s session, the S&P 500 has increased 20% from the low formed on October 12, 2022. According to Barron’s, the S&P 500 was in a bear market (a drop of 20% from the recent highs) for 248 days. Believe it or not, this was the longest stretch the S&P 500 has been in a bear market since 1948. The NASDAQ recently achieved “bull market” status (a 20% gain off recent lows) as of May and the Dow achieved that status in November 2022. Despite the 20% gains from the lows, the S&P 500 is still 11% from record highs that were made on January 3, 2022.

WFG News

Office Hours

Please be aware that starting after Memorial Day and running until Labor Day, Wentz Financial Group will begin its summer hours. Our hours will be 8:30 to 4:00 Monday through Friday. As always, if you need to speak or meet outside of those hours, please reach out and we will be happy to set up an appointment.

Office Closed – Monday, June 19

Please note that with the stock and bond markets closed and due to the national holiday, Wentz Financial Group will be closed next Monday, June 19th.

The Week Ahead

After what ended up being a calm and quiet week, the schedule picks back up this week with the biggest event of the week the Fed meeting on Wednesday. On the economic calendar the highlight will be the consumer price index Tuesday morning, which will come before the FOMC announces either a pause or hike in interest rates. The current consensus estimates see a 0.2% increase in the index, but still a stronger increase of 0.4% in core prices, while the annual rate is expected to have slowed to a 4.1% increase and a 5.3% increase in core prices. Elsewhere, on Wednesday the producer price index is released, on Thursday we will see an update on jobless claims, the Philly Fed and Empire State manufacturing indexes, May retail sales, prices of imports and exports, and industrial production, while Friday will see an update on consumer sentiment. The earnings calendar will still be light of quarterly releases with notable results from Oracle on Monday, homebuilder Lennar on Wednesday, and Kroger and Adobe on Thursday. On the central bank side, the European Central Bank will announce its policy decision on Thursday where the expectations are for another 25 basis point increase in its policy rate. Finally, the Federal Reserve holds its FOMC meeting on Tuesday and Wednesday with a policy announcement Wednesday afternoon. It will be a bigger meeting with investors betting no change in rates, although that has gone back and forth, and a new update to where policymakers see inflation, economic growth, unemployment, and policy rates in the Fed summary of economic projections.

By Wentz Financial|2023-06-13T09:25:11-04:00June 12th, 2023|Wentz Weekly|Comments Off on Wentz Weekly: Quiet Week Pushes Stocks Into New Bull Market, Fed Meeting Ahead