Wentz Weekly Insights

Software Selloff Drives Stocks Lower

US stocks were mixed again last week with a much larger divergence in markets than in recent weeks as the equally-weighted S&P 500 outperformed the cap weighted index by over 2%. So far this year, the equally-weighted index has overperformed the cap weighted index by over 4%; a 1.27% return versus 5.59%. A couple driving factors include a pullback in technology from a significant software selloff as well as weakness in mega cap tech stocks – an index of the Magnificent 7 stocks is down 4.32% this year. At the same time, small cap stocks are up 7.59%, a complete reversal from what we saw most of 2025 (and 2023-2024).

The software pullback stems from fears AI agents will be able to perform many software tasks and begin taking significant market share from many companies that excelled after the pandemic and possibly make them obsolete. This concern intensified last week after AI startup Anthropic announced a new tool called Claude Cowork, a desktop agent capable of conducting sophisticated professional tasks and coordinating whole teams of AI agents.

As Barron’s reported, an example of Cowork would be “Go through my emails and messages, find all the deliverables I have this week, and create first drafts of them, including any charts and slide decks. Then email the drafts to the team and solicit feedback.”

While this could disrupt software-as-a-service (SaaS) companies, it may have also provided opportunities for software companies. A basket of software stocks are now down over 30% from their highs in October.

On the earnings side, two more Magnificent 7 companies reported quarterly financial results last week; Amazon and Alphabet. These stocks, along with the others (Apple, Microsoft, Meta/Facebook, Nvidia, and Tesla) are all closely followed not only because they are the largest companies in the world but also because of the amount they are spending on the buildout of artificial intelligence infrastructure.

Amazon reported its financials that were much better than expected – its revenues of $213.4 billion were $2 billion more than the consensus estimate with growth in its Amazon Web Services segment (its more important segment that includes cloud computing) up 24% for the strongest growth in over 3 years, driven by AI workloads, a rise in backlog, and strong growth in its in-house chips. Its guidance was solid too, however it said due to strong demand it plans to invest $200 billion in capital expenditures in 2026, much more than the ~$150 billion analysts were expecting, and comments that the capex would continue through 2028.

Alphabet reported its financials that were solid as well – its $113.8 billion in revenues were $2.5 billion more than expected. It said it saw accelerating growth in Search with AI driving an expansion in Search, which was a concern given rising competition from chatbots like ChatGPT. Its key growth segment, Google Cloud, saw accelerating growth as well with revenue up 48%. Like Amazon, its very strong quarter was diminished by its capex plans. It expects to spend $175B-$185B this year, well above $115 billion that was expected.

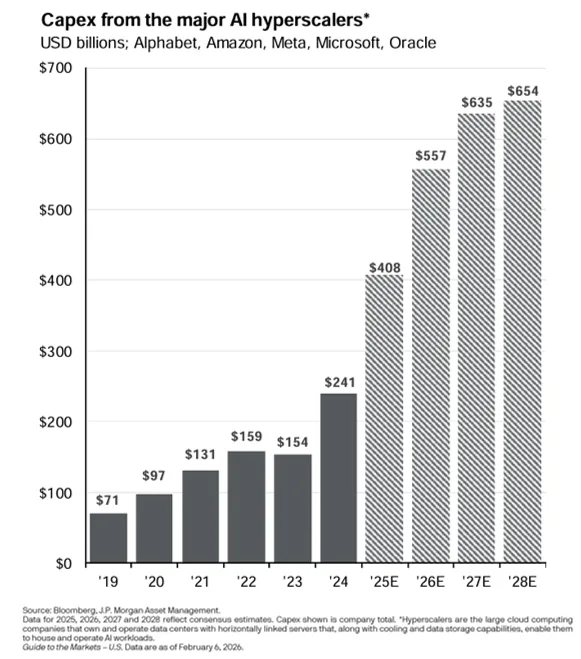

The chart below reflects the amount of capex the top 5 major hyperscalers (Alphabet, Amazon, Meta, Microsoft, and Oracle) have announced. Hyperscalers are the large cloud computing companies that own and operate data centers that enable them to house and operate AI workloads. The initial estimates saw capex plans of $557 billion for 2026, however after the earnings reports that has moved up to $710 billion, a staggering 74% increase from 2025. To put this extraordinary spending in perspective, the size of the US economy is $31.1 trillion and 2026 capex plans from only these five companies represents 2.3% of the US economy.

The Magnificent 7 stocks have lost $3 trillion in combined market cap since their record highs, with the largest drop coming from Microsoft, down 27% from its high in October. Apple has generated the best performance of the seven, down 4.8% from its highs.

Earnings season progresses this week, with an additional 15% of the S&P 500 scheduled to report. Investor attention will be centered on the consumer, as a higher concentration of consumer-facing companies release results. Attention will also be on the upcoming data releases – the employment report initially scheduled for last Friday was delayed to this Wednesday while the next batch of inflation data comes out Friday.

Week in Review:

It was a mixed week for US stocks with higher risk assets like technology selling off, driving a decline for the Nasdaq, while defensive stocks outperformed, leading to a strong gain for the Dow. The four major indices finished as follows: Dow +2.50%, Russell 2000 +2.17%, S&P 500 -0.10%, and Nasdaq -1.84%. Fixed income markets were little changed with the 2-year Treasury yield down 4 basis points to 3.50% while the 10-year Treasury yield fell 2 basis points to 4.22%. Bitcoin sold off alongside risk assets, falling another 16% last week and down 44% from its all-time high. The dollar index increased 0.66% while gold rose 5.03%. Meanwhile, oil fell 2.55%.

Recent Economic Data

- Employment Report: Due to the partial government shutdown that lasted a couple days, the January labor report is delayed to February 11.

- Job Openings and Labor Turnover Survey: The number of job openings in December moved lower again, falling to the lowest level of the post-pandemic economy at 6.542 million openings. This was almost 400,000 less than November’s openings and about one million openings less than the same month a year ago. The number of separations increased a little over 100,000, mostly due to a rise in layoffs. Meanwhile, the Challenger job cuts report noted US employers announced 108,000 job cuts in January, up 118% from a year earlier and the highest number of job cuts for a January since the Financial Crisis in 2009.

- ADP Payrolls: ADP’s payroll data said it saw 22,000 new private payrolls in January, half the increase that was expected and slowing from 37,000 in December. Job growth is up just 280,000 over the past 12 months, the slowest rolling 12-month increase since coming out of the pandemic, while average monthly gains are just 22,000. The report added that even though we have seen a dramatic slowdown in job creation over the past couple years, wage growth has remained stable.

- Jobless Claims: The number of jobless claims the week ended January 31 was 231,000, an increase of 22,000 from the prior week with the four-week average up slightly to 212,250. The number of continuing claims was 1.844 million, up 25,000 from the prior week and the four-week average was down about 15,000 to 1.850 million, the lowest since late 2024.

- PMI Manufacturing Index: The PMI manufacturing index was 52.4 for January, rising from 51.9 in December and slightly ahead of expectations, indicating manufacturing conditions improved and grew at a moderate pace in the month. Output growth saw its best growth since 2022 however it was likely driven by inventory building as new orders were more stagnant. Tariffs remain a key theme, driving up input costs at a faster pace than recent months and limiting demand gains, particularly from international markets, the report noted.

- ISM Manufacturing Index: The ISM manufacturing index was 52.6 for January, a sharp improvement from 47.9 in December, like the PMI report, indicating moderate manufacturing growth in the month for the first time in 12 months. The survey saw improvements in all five subindexes, however employment and inventories remained in contraction territory. Nine industries reported growth while eight reported contracting activity.

- Consumer Sentiment: The consumer sentiment index was 57.3 for February, rising from near the lowest levels ever in January. The index on current economic conditions rose 3 points to 58.3 while the index on consumer expectations declined slightly to 56.6. Year ahead inflation expectations fell from 4.0% last month to 3.5% in February, remaining in an elevated range. Longer-run expectations moved up to 3.4%, up from 3.3% last month.

Company News

- Disney: The Wall Street Journal reported Disney CEO Bob Iger has told people close to him he intends to resign from his position before his contract expires at the end of 2026. Disney Board later held a vote to name Josh D’Amaro as its new CEO, current head of parks and resorts who has been with Disney since 1998.

- Microsoft: The Wall Street Journal reported that Microsoft’s AI product Copilot is facing issues and higher competition. It said Copilot has become its key AI strategy, however its efforts to build it as an alternative to ChatGPT have been quite tough with confusing brand positioning and interoperability issues frustrating users, according to Microsoft employees. In addition, data shows only a small percentage of Microsoft enterprise subscribers use Copilot and the portion that prefer it over Alphabet’s Gemini has declined recently.

- AppLovin: Shares of AppLovin fell around 15% last Wednesday after an AdExchanger report said a new AI driven startup, CloudX, could disrupt the mobile advertising stack, something AppLovin has dominated. CloudX launched into general available last week, using large language models to automate advertising operations.

- FMC: Agricultural sciences company FMC said after its earnings release it is exploring strategic alternatives, including the sale of the company, saying they are in the preliminary stages and no guarantee a transaction will happen.

- Meta: Meta is now testing its “Vibes” app as a standalone platform to “build on its momentum,” which could become available as part of its family of apps soon. It was initially launched in September within the Meta AI app. Vibes is a social media app that displays short-form videos, similar to TikTok, but would also allow the creation and hosting of AI-generated videos only.

- Oracle: Oracle announced plans to raise up to $50 billion in capital to continue funding its AI buildout and meet contracted demands from its cloud infrastructure customers. Half of the funding will come from equity and the remainder debt, helping it protect its investment grade rating as well as its dividend, with minimum dilution to existing shareholders.

Other News:

- Tariffs: President Trump said he reached an agreement with India on trade to lower tariffs on Indian imports to 18% from 25% following a phone call between himself and India PM Narendra Modi. Trump added India will “reduce their tariff and non-tariff barriers against the United States to ZERO.” India also committed to buying more American goods and halt purchases of Russian oil.

- Strategic Minerals Stockpile:Bloomberg reported Trump is getting ready to announce a strategic critical minerals stockpile with about $12 billion in seed money in a venture named Project Vault with $1.7 billion in private funding and a $10 billion loan from the US Export-Import Bank. The strategic stockpile will be similar to the US strategic oil reserve as the US looks to reduce its reliance on China.

- Housing Boost: Housing stocks were higher last week after a Bloomberg report said homebuilders are working on a privately funded plan, “Trump Homes,” aimed at improving the supply of homes and easing the affordability issue. The plan would allow builders to sell entry level homes in a pathway-to-ownership program backed by private investors. There are several proposals, but one would allow investors to rent the homes to tenants with monthly payments counting toward a downpayment on the home after three years if the renter chooses to purchase. There are no agreed on numbers but some have discussed one million homes valued at $250 billion.

WFG News

Upcoming Events:

In March, we will welcome a Social Security Specialist who will provide an overview of how Social Security works and discuss key strategies to help maximize your benefits.

Click the link below to RSVP today!

WFG Investment Classes:

Interested in learning more about investing and how the markets work? Wentz Financial Group holds various Investment Basics classes throughout the year. Contact us for details!

The Week Ahead

The week ahead has two of the most important economic data reports of the month, a rare occurrence to see them both in the same week, something that is happening because the labor report was delayed from last week due to the brief government shutdown. The employment report is released Wednesday with economists expecting about 70,000 new jobs. The consumer price index is released Friday where economists expect a 0.3% increase in inflation in January and a 2.5% annual change. Other data reports include December retail sales, employment cost index for Q4, existing home sales, and jobless claims. Earnings season continues this week with another chunk of S&P 500 companies set to report quarterly results, with more consumer related companies. Notable company reports will come from Cliff’s, CVS, Spotify, Datadog, Robinhood, Ford, Cloudflare, Zillow, Shopify, KraftHeinz, McDonald’s, AppLovin, Cisco, Nebius, Crocs, Birkenstock, Coinbase, Pinterest, Toast, DraftKings, and Enbridge. There will also be a number of Fed policymakers expected to make public appearances this week where we expect comments on their stance with interest rates.