Wentz Weekly Insights

Supreme Court Overturns Trump’s Use of Emergency Tariffs

The holiday shortened week ended higher last week with the growth sectors bouncing back after experiencing weakness the prior week. The tech bounce drove Nasdaq higher 1.51% while the S&P 500 gained 1.07%. It was a calmer start to the week but it got more complicated as news headlines picked up with a couple moving pieces driving markets – the US/Iran negotiations, a wave of economic data, more earnings, FOMC meeting minutes, increasing private credit concerns, and ending the week with the Supreme Court’s decision on the legal use of tariffs.

Treasury yields moved a little higher on rising geopolitical tensions (Iran) and the Supreme Court tariff decision, however they remain in a tight range seen since last summer. Oil meanwhile has reached its highest level since last July over the situation with Iran.

The possibility of military action from the US in Iran has been hanging over the markets with Trump suggesting Iran reach a deal regarding its nuclear program. There were multiple reports that the US had increased its military presence in the Middle East the most since the Iraq invasion in 2003. Trump has given Iran an ultimatum to reach a deal within 15 days or “bad things will happen,” and more recently said the US could consider a limited military strike to improve the bargaining position.

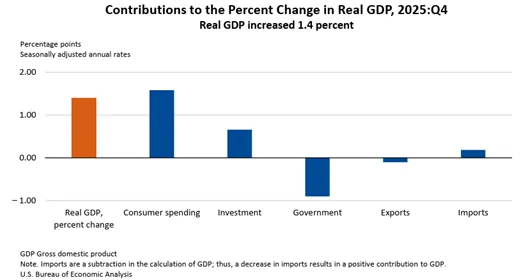

Between the headlines was a lot of economic data, most of it delayed from the government shutdown late last year. The most notable release was the first estimate of fourth quarter GDP (which will be revised a couple more times as we receive more complete data for the quarter). The report showed the economy grew at a 1.4% annualized rate in the quarter, half the growth expected.

However, the details were not as weak as the headline suggested. The largest component of GDP that makes up 70% of the US economy, which is consumer spending, increased 2.4% in the quarter, contributing 1.6% to the headline number. Business investments continue to be strong, driven by capital investments in AI infrastructure, with this category increasing 3.7% (a 0.5% contribution to GDP).

Government spending was the culprit for the weaker number, due to efforts by the administration to cut back on government spending and, to a larger degree, the government shutdown that occurred in the quarter. Federal spending declined 16.6% in the quarter, the third decline in the last four quarter, and subtracted 1.2% from GDP. The chart below illustrates the contributions to GDP.

While GDP was a little weaker than expected, we expect a stronger Q1 as these figures bounce back from easier comparisons. Beside GDP, other reports from last week show the manufacturing sector is off to a solid start to the year, inflation continues its stubborness, while unemployment claims remain very low, continuing to reflect the low hire, low fire labor market conditions.

This is leading to more Fed officials to believe it is wise to wait to cut interest rates again. This was reflected in the most recent minutes of the Fed meeting that were released last week. While the minutes were more of the same, there were a couple key items to note – mostly that the differences between officials appears to be wider.

Officials expressed their concerns about the uneven progress on inflation while seeing the downward risks of unemployment diminishing. Some officials advocated for language that could keep the possibility open for higher rates if inflation remains above its target. Overall, the minutes suggested less rate cuts in 2026 than was expected at the prior meeting.

But the highlight of the week came Friday with the highly anticipated Supreme Court decision on Trump’s April 2025 reciprocal tariff announcements. The Court ruled against Trump, holding that the International Emergency Economic Powers Act (IEEPA)—the law he relied on to impose the tariffs—does not authorize the president to implement tariffs. Uncertainty surrounding next steps remains high. It is unclear on the issue of refunding an estimated $175 billion in tariffs already collected (under the IEEPA) or what actions the administration and other nations may take regarding current trade deals.

Soon after the decision, Trump quickly announced a replacement tariff of 10% across the globe using alternative authorities – Section 122, which carries more constraints. Trump also has the Section 338 statute which allows the president to declare tariffs to respond to unreasonable policies that discriminate against commerce of the US.

Moving ahead, earnings remain a focus this week with the largest company in the world and the most important in the AI space, Nvidia, reporting after the close on Wednesday, followed by a wave of retailers (important for context on the consumer). There is another series of data releases, most of them delayed reports as the BLS catches up from the government shutdown. We expect a lot of focus on geopolitics as well – Iran, tariffs, and Tuesday evening when President Trump gives his first state of the union address of his second term.

Week in Review:

The holiday shortened week ended with higher stock prices overall as technology rebounded after a selling the first two weeks of February with consumer discretionary, communication services and technology some of the best performing sectors. The four major US indices finished as follows: Nasdaq +1.51%, S&P 500 +1.07%, Russell 2000 +0.65%, and Dow +0.25%. Treasuries were weaker as yields rose across the curve, mostly on the short end over more hawkish Fed comments – the 2-year yield increased 6 basis points to 3.48% while the 10-year yield rose 4 basis points to 4.09%. Oil rose another 5.6% for its highest level since last summer over worries on potential US airstrikes in Iran. The dollar index increased 0.91%, gold rose 0.74%, while Bitcoin fell another 1.24%.

Recent Economic Data

- GDP (first estimate): In the fourth quarter the economy grew at a 1.4% annualized rate, lower than the 2.8% rate expected and slowing considerably from 4.4% in the third quarter. Starting with the largest component, consumer spending, which makes up 70% of the economy – it was solid again, growing 2.4% which contributed 1.6% to GDP. Spending on goods fell slightly while services spending, which is where inflation is running the hottest, increased 3.4%. Investments by businesses and residential was strong again, increasing 3.4%, once again driven mostly by AI infrastructure spending. Business investments contributed 0.5% to GDP while residential investments (homebuilding) subtracted 0.1% from GDP. The growth in inventories was positive which contributed 0.2% to GDP. Imports declined 1.3% while exports fell 0.9%, with combined net exports contributing 0.1% to GDP. Government spending was the big one – spending by government fell 5.1% driven by a 16.6% decline in spending by the federal government. This contributed a negative 1.15% to GDP. A better measure of domestic economic growth, final sales to domestic purchasers, increased 1.1%, down from 2.8% in Q3.

- GDP Price Index: The GDP price index, an alternative inflation measure that measures the change in prices across all final goods and services produced in the US, was 3.6% in Q3, much higher than expected but down from 3.8% in Q3. It averaged 2.8% in 2025, hotter than the 2.5% average from 2024.

- Personal Income & Spending (Delayed): Personal income increased 0.3% in December as expected, slightly lower than the 0.4% increase from last month. The largest component of income, wages & salaries, increased 0.2%, slowing from 0.5% the month prior. What continues to grow the fastest is government transfer payments like social security and Medicare, etc where payments were up 0.8%. Incomes are up 4.3% over the past year, driven by a 9.5% increase in government transfer payments. Consumer spending increased 0.4% in the month, matching November’s increase. Spending on goods declined 0.1% while spending on services increased 0.7%. Spending is up a strong 4.7% over the past year with goods spending up 1.6% and services spending up 6.1%. Consumer’s disposable income increased 0.3% in the month, up 3.8% over the past year. The savings rate fell to 3.6%, the lowest since late 2022 and remaining below the historical average of around 7.5%.

- Trade Deficit: The big swings in the monthly trade deficit continued in December with a monthly deficit in trade of $70.3 billion. This is $17.3 billion higher than November’s deficit, and differs from the record high deficit of $136 billion last March and the 25-year low deficit of $28 billion in October. These wild swings are having a big impact on the overall GDP number. The larger deficit in December was due to a $5.0 billion decline in exports (or a 1.7% decline) and a $12.3 billion increase in imports (or a 3.6% increase). However, for 2025 the trade deficit was relative unchanged from 2024 with a $200 billion, or 6.2%, increase in exports and a $198 billion, or 4.8%, increase in imports.

- Empire State Manufacturing Index: The Empire State manufacturing index was 7.1 for February, basically unchanged from last month indicating manufacturing activity in the New York region rose at a moderate rate in the month. New orders improved while shipments were steady and inventories increased. The employment figures suggested employment increased slightly while the prices index showed input prices and selling prices both accelerated.

- Philly Fed Manufacturing Index: The Philly Fed manufacturing index was 16.3 for February, a slight increase from January, indicating solid growth in manufacturing activity in the Philadelphia region. General activity and new orders were reported as very solid however shipments were a little weaker while employment trends were steady but remained in negative territory. Both input prices and selling prices continue to suggest overall price increases but the index was the lowest in 13 months.

- Industrial Production: Industrial production increased at a 0.7% rate in January, more than double the expectation and strongest increase in a year. The strength was due to a 2.1% increase in utilities, which is very weather related and possibly due to the very cold month, while manufacturing rose a solid 0.6% due to a 1.4% gain in the auto sector, and slightly offset by a 0.2% decline in mining. Percent of capacity was 76.2%, up a half percent from December and up 1.4% over the past year, signifying the stronger conditions.

- Jobless Claims: The number of continuing claims the week ended February 14 was 206,000, a decrease of 23,000 from the prior week with the four-week average at 227,000. The number of continuing claims was 1.869 million, up 17,000 from the prior week with the four-week average relatively unchanged at 1.845 million.

- Housing Market Index: The housing market index, and index on homebuilder sentiment, was 36 for February, dropping one point from January and back down to the lowest level since September after a brief improvement. The index on present sales was 41, relatively unchanged over the past five months, the index on expected sales over the next six months was 46, dropping from 49 for the lowest in five months, and the index on traffic of prospective buyers was 22, dropping back near the lowest levels of this cycle.

- Housing Starts & Permits (Delayed): The number of housing starts in December (delayed, the report included numbers for November and December) increased 6.2% in the month to a seasonally adjusted annualized rate of 1.404 million (up over 10% from October, which was the lowest of the year). However, starts are still down 7.3% over the past year and remain at a very low level considering the demand for housing. The number of permits increased 4.3% in the month to an annualized rate of 1.448 million, though 2.2% below the rate from a year earlier. Even more, the number of homes under construction has steadily declined through the year, now at 1.277 million (annualized), the lowest of the year and down 11% from a year ago, not a good sign for future sales.

Company News

- Warner Bros. Discovery: Warner Bros. Discovery said it is reopening negotiations with Paramount Skydance amid worries over regulatory pushback with its deal to be acquired by Netflix. It said it will give Paramount seven days to come up with its best and final offer for acquiring the company after it rejected its $30.25/share offer, which was above Netflix’s $27.75/share offer. Warner Bros. added it expects a higher offer and will hold talks to address deficiencies that remain.

- Apple: Bloomberg reported that Apple is developing new AI powered smart glasses that will be equipped with a camera, speakers, and a microphone, while relying on the iPhone for a bulk of its computing power. It also plans to design and develop its own frames rather than working with a partner like Meta did with Ray-Ban. In addition, the company said it was holding a product event on March 4.

- Tesla: Tesla said it will integrate xAI’s Grok AI chatbot into its cars in the UK and eight other European markets, allowing users to ask questions and get answers real time as well as adding or editing navigation.

- Meta: The Information reported Meta is bringing back plans from five years ago, which was initially scrapped to cut costs, to launch a smartwatch this year in a direct competition with the Apple Watch. The new watch will have a built in Meta AI assistant and include health tracking features.

- Madison Square Garden Sports: The board of Madison Square Garden Sports has approved the move to explore the option of separating its New York Knicks business from its New York Rangers business into two separate publicly traded companies. The move would allow each franchise to focus on its own league, business strategy, and media rights. According to Forbes, the Knicks have a estimated valuation of $9.7 billion while the Rangers have an estimated valuation of $3.7 billion.

Other News:

- FOMC Meeting Minutes: The minutes of the Fed’s January meeting showed a larger divergence in the outlook among Fed officials. There was more concern about the uneven progress to bring inflation back to 2% and at the same time officials saw downside risks to the labor market diminishing. Dissenters saw policy meaningfully restrictive mainly due to risks to the employment market. On the other hand, several mentioned the possibility of rate hikes, not specifically calling for rate hikes but saying the balance of risks should be more even (same likelihood or cuts versus hikes). The minutes painted a picture of less rate cuts than was portrayed at the post-meeting press conference.

- Fed Talk:

- Fed Governor Miran, who Trump nominated and has been the most dovish Fed official by far, said yesterday he is leaning less aggressive on rate cuts than he was a couple months ago. He said the economy is evolving differently than what he had expected, with the labor market a little better than expected and more signs of firming in goods inflation.

- San Francisco’s Fed President Mary Daly spoke about the economic implications of artificial intelligence and said it could be possible the productivity gains driven by AI could allow the economy to grow without higher inflation. Despite this she said it is too early to call AI transformative, arguing one-time cost savings from automation differ from sustained productivity gains.

Did You Know…?

New Number One:

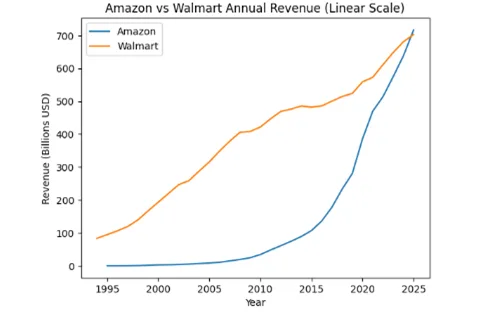

Walmart has been the largest company in terms of revenue generated for almost 20 years, however last week the company lost the top position. As of the most recent full year, Amazon surpassed Walmart’s revenues, becoming the largest company. Amazon generated revenue of $716.9 billion in its most recent full year while Walmart said last week its full year revenues were $713.2 billion. Amazon, a 31-year old company, began as an online bookseller in a garage to dominating the e-commerce industry as well as what most people don’t see – cloud computing and artificial intelligence. Its cloud computing division, called Amazon Web Services (AWS), generated $128.7 billion in revenue, a 20% increase. Amazon is expected to build on its position with sales currently growing faster than Walmart – last year it saw revenue growth of 12.4% while Walmart was 4.7%. (Some of this data was obtained from the Wall Street Journal). Chart source: ChatGPT

WFG News

Upcoming Events:

In March we will welcome a Social Security Specialist who will provide an overview of how Social Security works and discuss key strategies to help maximize your benefits.

Click the link below to RSVP today!

WFG Investment Classes:

Interested in learning more about investing and how the markets work? Wentz Financial Group holds various Investment Basics classes throughout the year. Contact us for details!

The Week Ahead

It will be another busy week with a focus on economic data, tariffs, geopolitics, and the main event for the week on Wednesday with Nvidia’s quarterly earnings. Other than Nvidia, earnings will continue to highlight smaller tech companies as well as many more retailers. Notable quarterly earnings reports this week will come from MercadoLibre, Axon, Workday, HP, Circle, theTradeDesk, Salesforce, Snowflake, Synopsis, Baidu, CoreWeave, Dell, Home Depot, Planet Fitness, TJX, Celsius, and Warner Bros. Discovery. The economic calendar would be very quiet, but the Bureau of Economic Analysis is busy releasing delayed reports from the government shutdown. Notable data releases include factory orders, durable goods orders, construction spending, the producer price index, new home sales, Case-Shiller home price index, and consumer confidence. Trump’s next move on tariffs will be top of mind as well after the Supreme Court shot down his reciprocal tariffs. There will also be focus, particularly the oil markets, on the situation with Iran and if negotiations will continue or if the US carries out airstrikes on the country’s nuclear facilities.