Wentz Weekly Insights

Inflation Cools Further In July, But Still Far From Target

|

|

Recent Economic Data

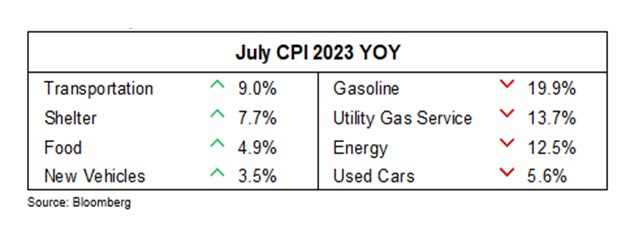

- The consumer price index rose 0.2% in July with the index rising 3.2% from July 2022, picking up slightly from the 3.0% rate in June and both coming in exactly as expected. In July 2022, the 12-month inflation rate was 8.5%. In addition, core prices, which exclude categories that are volatile like food and energy, rose 0.2% and are up 4.7% from a year ago, down slightly from 4.8% in June. Again, both numbers here were exactly as expected. Inflation has fallen substantially over the past several months, but core prices are still too high, and headline inflation has a risk of going up next month due to energy prices moving higher. Driving the higher prices in July was food up 0.2%, energy up 0.1% with shelter, which is by far the largest component in the index, up 0.4%. Driving the index lower were commodities (excluding energy) down 0.3%, used vehicles down 1.3%, airfares down 8.1%, and medical care/hospital services down 0.4%.

- The producer price index increased 0.3% in July, slightly higher than the 0.2% increase expected, with input prices for producers up 0.8% over the past year, up from 0.2% in the prior month. Core prices, which exclude food and energy, rose 0.3% also slightly more than expected and are up 2.4% from a year earlier, matching June’s increase. The increase was driven by a 0.5% increase for final demand services, led by trade and transportation/warehousing, while prices for final demand goods were up a lesser 0.1%.

- The index for consumer sentiment, created from a survey of consumers by the University of Michigan, was 71.2 for the first August survey, down slightly from 71.6 in the July survey and near the highest levels in almost two years. For comparison purposes, the low was around 50 last year while the historical average is 86. Current conditions was at 77.4, up from 76.6 in July while expectations fell somewhat, down to 67.3 from 68.3 in July. Inflation expectations over the next year dropped to 3.3% from 3.4% while expectations over the upcoming five years is 2.9%, down from 3.0%.

- The number of unemployment claims for the week ended August 5 rose 21k from the prior week to 248,000 with the four-week average at 231,000. The number of continuing claims was 1.684 million, down 8k from the prior week, with the four-week average at 1.701 million, also down nearly 10k.

- U.S. trade activity declined again in June with exports falling 0.1% and imports falling 1.0%. The U.S. trade deficit was $65.5 billion for June, which is down $2.8 billion from May and will be a slight positive read for GDP (one input to the GDP calculation is exports minus imports). The value of exports fell $0.3 billion to $247.5 billion while imports fell $3.1 billion to $313.0 billion. While the deficit is the headline number of the report, more importantly might be the volume of trade as that shows both domestic and global economic strength (higher activity = higher demand). For the first six months of the year exports are up 2.5% while imports are down 4.0%.

- Consumer credit grew a seasonally adjusted annual rate of 4%, or by another $17.85 billion in June, higher than the $13.0 billion expected and double the growth from May. Total consumer credit is just $2.9 billion from eclipsing $5 trillion for the first time ever. Revolving credit like credit cards was actually relatively unchanged while nonrevolving credit rose 0.5%, or $18.4 billion.

- The average prime rate for a 30-year mortgage nearly touched 7% last week, rising another 6 basis points to 6.96% for the highest level since hitting a high of 7.08% November, according to Freddie Mac’s weekly mortgage survey. The low this year was in February at 6.09%.

Company News

- Sources say that Disney has formed a task force to evaluate how artificial intelligence can be used across the company, according to Reuters. The task force was formed earlier this year before the writers’ strike and comes despite Hollywood writers and actors desire to prevent the industry’s use of the technology. The report notes there were job openings seeking candidates with expertise in AI or machine learning with roles that could be across its studios or theme parks.

- There was big news in the sports betting world with Penn Entertainment agreeing to sell 100% of Barstool back to David Portnoy. It also announced it and Disney have entered into a long-term exclusive strategic alliance for US sports betting where it will get exclusive rights to ESPN, including access to its unique audience, and will rebrand Barstool Sportsbook to ESPN Bet where ESPN will get its own branded sportsbook. Penn will benefit from exclusive promotional services across ESPN platforms like programming, content, and access to ESPN talent. It is a $2 billion deal in which Penn will make a $1.5 billion cash payment to ESPN and grant ESPN $500 million of warrants to purchase Penn stock. Penn indicated it could generate an additional $500 million to $1 billion or more of annual adjusted EBITDA as a result.

- Shares of biotech company Novo Nordisk moved higher last week after it announced that a Phase 3 trial for its new weight loss drug “semaglutide” (branded as Wegovy) revealed the therapy led to a 20% reduction in adverse cardiovascular events for obese or overweight adults with cardiovascular disease. The study included 17,000 adults aged 45 and older.

- Nvidia introduced its new next-gen “superchip” that is built for accelerated computing and advanced AI and the company said is designed to handle complex generative AI workloads, large language models, and others. The new chip can deliver 3.5x more memory capacity and 3x more bandwidth than the current generation.

- Tapestry, owner of the Coach brand, announced it has agreed to purchase Capri Holdings, owner of brands like Michael Kors, Jimmy Choo, and Versace, for $57 in an all cash deal that values Capri at $8.5 billion, a 65% premium to where shares closed yesterday.

- Cleveland based, flat-rolled steel producer Cleveland-Cliffs said over the weekend it presented an offer on July 28 to acquire US Steel which the company’s board rejected. Cliffs proposed buying US Steel for $17.50 in cash plus 1.023 shares of Cliffs stock which implied a total value of $35/share of US Steel which was a 43% premium to US Steel’s stock before the announcement was made. The board of US Steel rejected the offer as being “unreasonable.” Due to the rejection and no additional reasoning, Cliffs was compelled to make the offer publicly known.

Other News

- President Biden signed an executive order last week that would limit the US investments in China that would target certain sectors like semiconductors that affect things like quantum computing and artificial intelligence. The U.S. said the new order would “prevent U.S. investments from helping accelerate the indigenization of these technologies” in countries of concern and prevent China’s military from benefiting from American technology and funding.

- Policymaker comments:

- Philly Fed President Patrick Harker said the Fed may be close to where it can “hold rates steady and let the monetary policy actions we have taken do their work,” implying he prefers to hold rates steady to give higher rates time to work through the economy to see its impact. He added this assumes data comes in as expected between now and the next Fed meeting. He also said this does not mean the Fed will cut rates saying if this is the case rates will stay here “for a while.”

- Fed Governor Bowman said yesterday she does expect additional rate hikes will be needed.

- New York Fed bank President John Williams said in an interview with the NY Times that monetary policy is in a good place and where it needs to be and that he sees rates staying in restrictive levels for some time. He added rate cuts may be warranted as soon as next year if inflation does slow, one of the more direct comments on potential future rate cuts. He said how long rates will stay restrictive will depend on the data, something that has been repeated by his peers.

- San Francisco Fed president Mary Daly said after the inflation report that the data was as expected and shows inflation is moving in the right direction. She added the data still does not signal there is a victory over inflation and the Fed has more work to do. In addition, it is undecided still on what the policy move will be at the next meeting but we are still a long way out from cutting rates. Later in the week, Daly said the July consumer price index (data that came in as expected) was good news but that does not mean the Fed will declare victory.

Did You Know…?

Its all about AI:

In a new research note by Global X, an ETF provider, the artificial intelligence mania continues to gain traction, by investors and corporate executives. The mention of AI in earnings calls during the first quarter spiked 77%, while shares of AI and robotic related businesses have outperformed the S&P 500 by 21% so far this year. It added the time it took for OpenAI’s ChatGPT to reach 100 million users was just two months, this compared with TikTok taking 9 months, Instagram taking 30 months, and Google Translate taking 6.5 years. According to Global X, “Generative AI refers to artificial intelligence systems that are designed to create new and original content based on the data they are trained on. This can include generating text, images, music, and even 3D models. Unlike discriminative AI, which is used to classify and categorize data, generative AI creates new data by using probabilistic models to produce outputs based on patterns it has learned from the input data.”

Household debt:

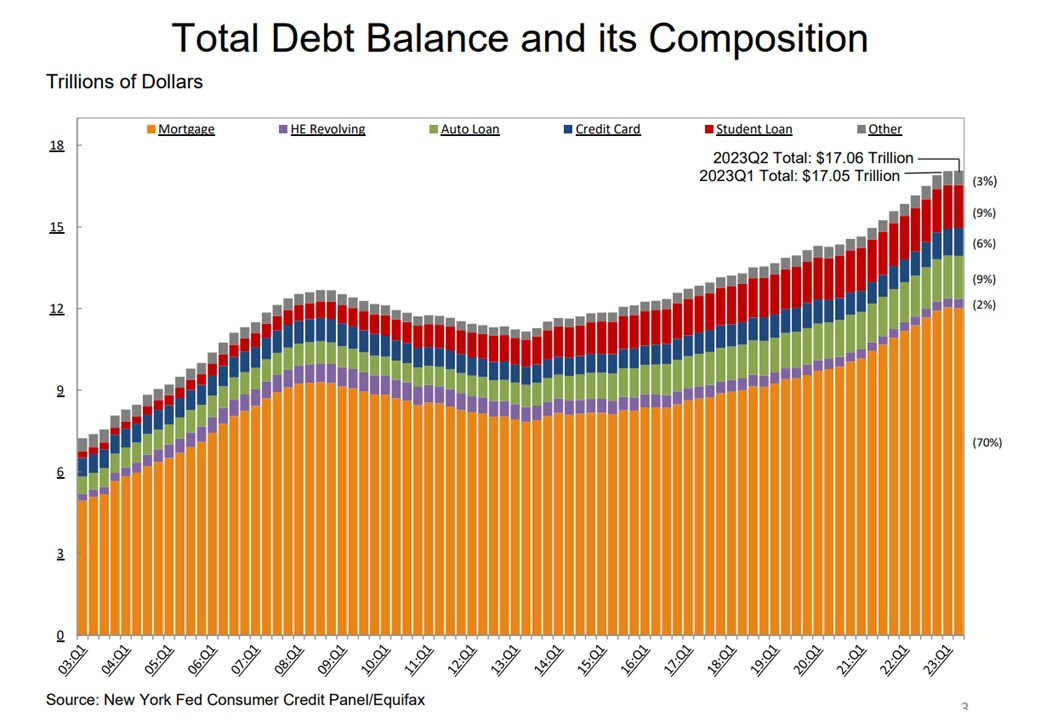

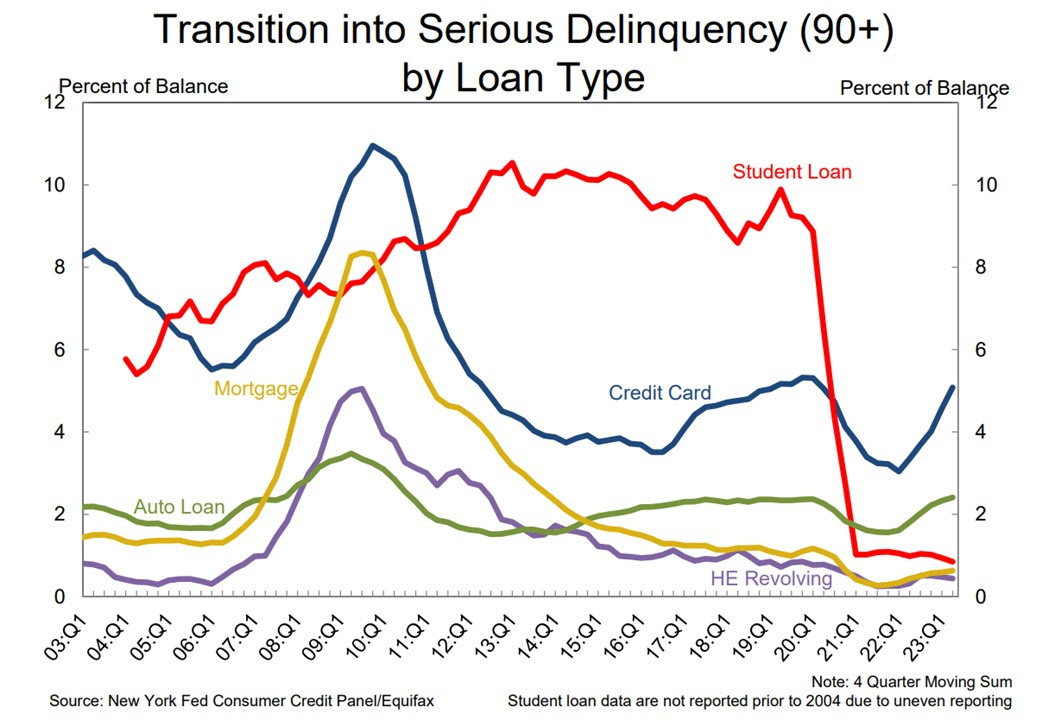

The New York Fed’s quarterly report on household debt shows total debt increased $16 billion in Q2, just a 0.1% increase from Q1 with total debt balances now at $17.06 trillion. Compared to pre-pandemic levels, household debt is up $2.9 trillion, or 20.5%. Mortgage debt fell $30 billion, or 0.2%, for the first decline since 2018 (which reflects the slower housing market/sales activity). Revolving debt rose 1.1% with credit card debt climbing the most since 2021 with a 4.6% increase in the quarter. Credit card debt is now at $1.03 trillion, crossing $1 trillion for the first time ever. Credit card delinquency rates have risen and are now back to pre-pandemic levels.

The Week Ahead

Earnings season continues but the focus this week will shift to big box retailers, as well as several other notable tech companies. Some noteworthy results will come from Home Depot on Tuesday; Target, TJX, Cisco, JD.com on Wednesday; Walmart, Tapestry, Ross Stores, Applied Materials on Thursday; and Deere, Estee Lauder, and Palo Alto Networks on Friday. On the economic calendar we will see several updates on the housing market including the housing market index on Tuesday and housing starts and permits on Wednesday. Elsewhere, the most notable economic release will be July retail sales which comes out Tuesday morning where the consensus sees sales rising 0.4%, up from a slower 0.2% monthly pace in June. Also on Tuesday will be the Empire State Manufacturing index, import and export prices, followed by industrial production on Wednesday, the Philly Fed manufacturing index and jobless claims on Thursday. Market participants will also be focused Wednesday afternoon on the release of the FOMC meeting minutes from last month to see if there were any additional hints at the Fed’s next policy move or ideas on peak interest rates. On the political front, Congress remains in recess.