Wentz Weekly: U.S. Sees Credit Rating Downgrade For Second Time in History

Wentz Weekly Insights U.S. Sees Credit Rating Downgrade For Second Time in History

It was a down week for stocks for the first time in four weeks, driven mostly by the technology sector (which lost 4.1%) while energy was the lone sector seeing a gain. A small rally in energy stocks recently is being driven by higher oil prices where crude oil saw its sixth consecutive weekly increase, now up 20% over that period reflecting a more resilient global economy suggesting stronger demand for oil.

On the earnings side of things, Amazon and Apple made the headlines in a week where almost 200 S&P 500 companies reported results. It was a tale of two stories with Amazon shares up nearly 10% after its results while Apple shares were down 4.8% with its market cap falling below the $3 trillion level. The takeaway for Amazon was resiliency in its e-commerce business and better than expected growth in its cloud computing segment (AWS – Amazon Web Services) with its cost cutting measures improving profitability, as well as a better than expected forecast for the third quarter. It discussed on the conference call how AI is “going to be at the heart of what we do.” Apple’s drawdown stemmed from disappointing sales for hardware including its most important and profitable product the iPhone where sales declined for the third consecutive quarter. A bright spot was services, where it saw subscriptions rise to one billion for the first time, as well as a recovery in China.

Meanwhile, market participations were surprised when one of the three major credit rating agencies, Fitch Ratings, announced it downgraded the United States’ long-term credit rating one notch. Fitch said the downgrade was due to the expected fiscal deterioration, a high and growing debt burden, a rising interest service burden, a steady erosion of governance relative to peers with the same credit rating, a complex budgeting process, rising social security and Medicare costs, and the repeated debt limit standoffs and last minute resolutions.

The only other time the U.S. saw a credit downgrade was in 2011 by S&P following the debt-ceiling crisis that occurred that year. This caused the most volatile week for financial markets since the Financial Crisis with stocks falling over 15% in the following days. Interestingly enough, Treasury bonds rallied with yields falling as investors bought up “safe haven” assets like US debt, despite the lower credit rating, because of fears Europe’s debt crisis would spill over to the U.S. and the U.S. debt remains the only risk-free asset.

Many tried using what happen in 2011 as a guide for this time. However, longer-dated Treasury bond yields rose and stocks fell only slightly, down 1.38% after the announcement. However, this also coincided with another strong report on the labor market (ADP reported more job gains in July than what was expected – this led to concerns for more rate hikes and a higher peak rate, hence the move higher in yields) and the Treasury refunding announcement where it said it will offer more bonds in the upcoming auction than expected.

It is also worth noting Fitch projects a recession in the fourth quarter this year and first quarter 2024. It said tightening credit conditions, weaker business investment, and slowing consumer spending will lead to a “mild recession.” The resiliency of the economy lately it said makes the Fed’s job of bringing inflation lower so does not see rate cuts until next year.

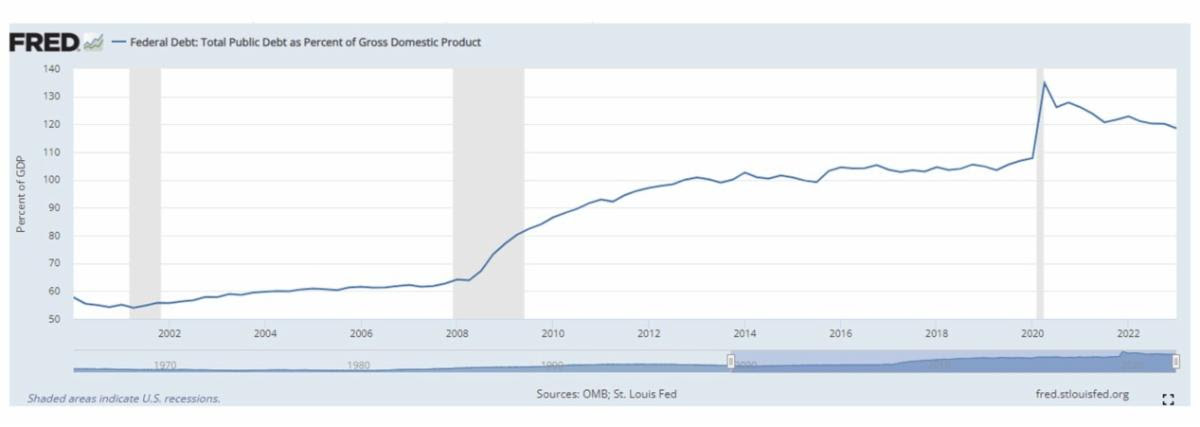

What the downgrade does do though is bring an important issue in focus which is the government’s spending problem and the trajectory of the nation’s debt. Since the passage of the package to suspend the debt ceiling earlier this year, the debt has increased over $1.1 trillion from $31.47 trillion to $32.60 trillion. To put into context, as the chart this week shows, the debt is 121.5% of the size of the U.S. economy – also called the debt-to-GDP ratio. The level was 106% prior to the pandemic and just 62% prior to the Financial Crisis. Add on to this higher interest rates which results in the cost to service the debt surging (the interest the Treasury pays on its debt). With tax revenue limited the only solution would be to control spending, but both parties in Congress are needed to get this done.

While this has been in the news, the other big headline last week was the July employment report where data was basically in line with expectations. In July, 181,000 new jobs were created, below the average of 312,000 over the past 12 months. The labor force continued to increase with the number unemployed near the post-pandemic low and the unemployment rate falling to 3.5%. Wages will be something to focus on going forward – July wages rose 0.4%, slightly higher than expected, with the average up a more than expected 4.4% over the past 12 months.

The labor market has remained resilient but is showing signs of slowing with jobs creation in July at the slowest pace since declining in 2020. We are cautious over the near term with stocks showing they are at risk to a pullback, especially as markets enter a seasonally weak period (August is the eighth worst and September is the worst month of the year on average). The next catalyst for markets will be the inflation report on Thursday.

Week in Review:

The week started on a quiet note Monday with no economic data and few earnings reports before the open. It was the last day of July in which equity markets finished higher to end the month with a 3.11% gain, the fifth straight monthly gain. The Federal Reserve released the Senior Loan Officer Survey that showed banks lending standards continued to tighten over the past three months with loan demand weakening further for commercial and consumer loans. Treasuries saw little movement while stocks were higher across the board with the S&P 500 gaining 0.15%.

Several high profile earnings reports, like Caterpillar and Uber, showed strong results and guidance for Q3 but the major indexes began the day lower. Economic data included key manufacturing surveys for July that showed the 10th consecutive month of contracting activity, along with job openings that fell slightly but hit a new 2 ½ year low (still well above pre-pandemic levels). Fed comments from Chicago’s Goolsbee and Atlanta’s Bostic both noted they see a path for inflation coming down but pushed back on potential rate cuts in 2024 saying cuts are still far in the future. Treasury yields saw an uptick with the 10-year back over 4.0% while stocks were mixed in a favor to value with the Dow slightly higher and S&P 500 down 0.27%.

The big headline going into Wednesday’s session was credit rating agency Fitch’s surprise downgrade of the U.S.’s credit rating to AA+ from the top notch AAA. This caused a risk-off day with a selloff in stocks, which closed near the lows of the day, and a rise in bond yields. Also driving yields higher was stronger economic data on the labor market and the Treasury refunding announcement where it announced a larger funding need than expected (higher bond offerings in the upcoming quarter). Stocks fell 1.4% while the yield curve saw a flattening with the 10-year treasury yield hitting 4.10%.

Thursday’s headlines included the pickup in bond yields over concerns of excess Treasury supply, the Bank of England raising rates another 25 basis points with some policymakers supporting a 50 basis point increase, another wave of earnings reports – mostly mixed, and more solid economic data points including better worker productivity, jobless claims that were steady, but a weaker (yet still growing) services sector via the ISM services index. The risk off trade continued Thursday, although to a lesser extent, with long-term Treasury yields continuing to move higher (the 10-year nearing 4.20% for the highest since November), and stocks trading lower by 0.25%.

Apple and Amazon earnings reports took Friday headlines after they reported Q2 results after Thursday’s close. Apple shares were lower over weaker iPhone demand where sales missed expectations, but seeing strength in its services and subscriptions, while Amazon shares were much higher over additional strength in its cloud offerings and e-commerce, in addition to higher profitability amid cost cutting efforts. The other big headline was the employment report for July where job gains were slightly less than expected but wages grew slightly more than expected. Stocks ended up moving lower led by Apple, the broader tech sector, as well as defensive sectors, but offset by strength in consumer discretionary. The S&P 500 fell 0.53% while Treasury yields saw a sharp move lower.

For the week Treasury yields saw a multi-month high, before the sharp rally in bonds Friday that led to lower yields. The 2-year yield ended up finishing the week 10 basis points lower to 4.78% while longer-dated bond yields moved higher as the 10-year reached a new year-to-date high of 4.21% before settling Friday at 4.05%. Stocks finished lower across the board, led by technology (-4.1%) after a disappointing quarter from Apple. The major indices finished as follows: Dow -1.11%, Russell 2000 -1.21%, S&P 500 -2.27%, and NASDAQ -2.85%. Commodities continue to move higher, with oil seeing its sixth consecutive week of gains with a 2.8% increase. The dollar index was down 0.8% and gold was up 0.8%.

Recent Economic Data

Job openings came in pretty much exactly in line with expectations – the number of job openings was 9.582 million on the last day of June, dropping about 30k from May and is now the lowest level of openings since April 2021 when openings were on their substantial uptrend (as a reminder, job openings were trending around 7.2 million prior to the pandemic). The number of hires declined 326k to 5.9 million, the number of layoffs was unchanged at 1.5 million, while the number of quits fell 295k to 3.8 million for the first notable decline in months.

ADP says it saw another very strong month of payroll gains. For July it saw payroll gains of 324,000, again almost double the expectations of 185,000. Leisure and hospitality continues to drive a large portion of the gains, with 201,000 payroll additions coming from the sector, and a meaningful decline only seen in manufacturing where surveys have shown us activity has been contracting for almost a year now. Small business saw all the job gains with large businesses seeing a small decline.

Jobless claims remain at very low levels, with the number of claims filed to states for the week ended July 29 at 227,000, up just 6k from the prior week with the four-week average falling 5.5k to 228,250. The number of continuing claims rose slightly to 1.700 million, with the four-week average down 4.5k to 1.712 million. The week prior, claims fell to the lowest level since February.

The Department of Labor’s employment report showed employment grew 187,000 in July, slightly below the consensus expectation and below the 12-month average of 312,000, according to its establishment survey. June’s job gains of 306k were revised down to 281k and May’s 209k was revised down to 185k for a total downward revision of 49k. Other details:

In July, employment gains was seen most in health care, social assistance, finance, whole trade, construction, and leisure/hospitality and losses were seen in professional business services.

The household data showed the labor force increased 152k to 167.103 million but the labor force participation rate was unchanged at 62.6%, matching the post-pandemic high, but still below pre-pandemic levels of 63.3%.

The number of people employed increased another strong 268k to 161.262 million, the highest ever.

Those unemployed declined 116k to 5.841 million, where this number has bounced around over the past year between 5.650 million and 6.100 million.

The above numbers resulted in a 0.1% drop in the unemployment rate to 3.5%, while the U-6 rate (underemployment rate) fell 0.2% to 6.7% (the low was 6.5% in December).

Wages grew another 0.4% (equals a 4.8% annualized rate), slightly higher than 0.3% expected, and are up 4.4% from July 2022 which is 0.2% higher than expected.

Also important to note, the average weekly hours worked was 34.3 hours, down from 34.6 several months ago and down from 35.0 hours earlier in the pandemic, and now back to pre-pandemic levels. This may be telling us employers are no longer having as much difficulties finding workers as their existing employees are no longer needed to work longer hours.

The U.S. PMI manufacturing survey index was 49.0 for July, an improvement from 46.3 in June but still below 50 which signals a contraction in activity. It was another monthly decline in new orders while input buying fell which led to a large decline in inventories. Manufacturers saw a rise in raw material costs but stable selling prices. Interestingly, employment strengthened as companies saw greater confidence in the outlook for output.

The ISM manufacturing index was 46.4 for July, below the expectations of 46.9 and remains in contraction territory for the 10th consecutive month. New orders were 47.3 and have not expanded since August which led to a continued decline in output. Good news is prices paid continue to decline and the index was 42.6 which is a positive read for inflation. Employment was weaker with the report saying there are signs of employment reduction in the near term to better match lower output.

The ISM Services index was 52.7 in July versus the 53.1 expected and an improvement from May. Prices showed upward pressure with the prices paid index at 56.8, an uptick from 54.1 in May. New orders slowed to 55.0 from 55.5 in May.

Construction spending in June increased by 0.5% compared to May with a 0.9% increase in residential construction spending and a 0.1% increase in nonresidential. Compared to a year ago construction spending is up just 3.5%, driven by nonresidential projects which remains strong, but offset by a 10.3% decline in residential, which has actually improved in recent months but also coming off easier comparisons from a year earlier.

US worker productivity increased a much better than expected 3.7% (all numbers are annualized rates) in the second quarter, according to initial data (which will be revised) from the Department of Labor. This was well above the 1.3% increase in productivity that was expected and comes after a 1.2% decline in productivity from the first quarter (which was actually revised upward from a 2.1% decline in the previous estimate). The better than expected productivity is because hours worked declined 1.3%, the first decline since Q2 2020, with output increasing 2.4%. Now looking at productivity compared to a year ago, it increased 1.3% reflecting a 2.6% increase in output and a 1.2% increase in hours worked. This data is important not for the short-term, but for longer-term economic growth as productivity is one of the most important variables.

Company News

The WSJ is reporting, citing a company memo, CVS will cut 5,000 jobs (1.7% of its 300k workforce), mainly corporate positions, in effort to reduce costs and aligning with its shift to focus on its health services. It is also looking to reduce travel expenses and looking to cut the use of consultants and outside vendors.

Meta is planning to launch a range of AI powered chatbots which give different personalities in attempt to boost engagement with its social platforms, and the changes could come as soon as September, according to a report by the Financial Times. It is designing prototypes that could have humanlike abilities and talk with its users, for example a chatbot that talks like Abraham Lincoln, or another that advises on travel options in a specific personality (like a surfer).

One of the first less-than-truckload (LTL) carriers, Yellow Corporation, announced over the weekend it has filed for bankruptcy after its debt issues that stemmed from its many acquisitions since 2000 were made worse by a union contract dispute. Yellow employed about 30,000 people and said in the filing it had $1 billion to $10 billion in assets and the same amount of debt with over $1 billion in debt that matures in 2024.

Other News

The Senior Loan Officer Opinion Survey on Bank Lending Practices noted banks continue to tighten standards for business and consumer loans. One of the ways was from increasing spread of their loans compared to the cost to fund the loans (higher net interest margins for banks). Banks are seeing reduced demand for commercial and industrial loans across all size firms, and continue to see weak demand for commercial real estate loans. On the consumer side, demand for mortgage remains weak while there were tighter standards and weaker demand for all consumer loan categories including home equity lines, auto loans, other loans, and credit card loans. One special question for this survey was banks outlook for the second half of 2023 which they responded they expect further credit tightening, citing a more uncertain economic outlook and expected deterioration in collateral values and credit quality of loans. It is hard to quantify the survey results but overall lending conditions tightened significantly after the banking issues in March/April and continued to tighten further since then.

Amid stronger economic data and an equity market rally, many strategist are increasing S&P 500 price targets and economic forecasts. Bank of America said last week it no longer expects a recession and sees a path for a soft landing of the U.S. economy, citing recent incoming data. It expects sluggish growth in 2024 where growth is below trend, but growth will nonetheless remain positive.

Last week Fitch downgrading the government debt rating to AA+ from the top notch AAA rating. It cited the “expected fiscal deterioration over the next three years,” the high and growing debt level, the “erosion of governance” relative to peers of the same credit rating, repeated debt limit standoffs and last minute resolutions, the lack of a medium-term fiscal framework, a complex budgeting process, and rising social security and Medicare costs. The last and only other time the US debt got a downgrade was about 10 years ago and the S&P 500 dropped about 7% afterwards.

A joint ministerial meeting of OPEC+ members on Friday concluded with no change in production quotas from the group. Saudis will continue with its 1 million barrel/day production cut (with production at 9 million bbl/day), with Russia continuing its cuts as well. Meanwhile, last week saw a 15.4 million barrel draw on crude oil inventories, the largest weekly drop in stockpiles ever (data going back to 1982), according to the weekly data by API. Inventories are now at the lowest levels since January. Crude oil prices rose another 2.8% last week, the sixth consecutive weekly gain. Over this period crude oil has increased 19.8%.

The Bank of England raised interest rates 25 basis points to 5.25% as was expected with a 6-3 vote, with 2 members voting for a 50 bps increase and one voting for no change. The inflation expectation was revised higher compared to the May projections, economic growth has been around 0.2% during the first half and is expected to be similar in the second half. The policy statement mentioned that policy is now restrictive and will remain restrictive for a time that is “sufficiently long.”

The Week Ahead

Earnings season continues this week while data on the economy will shift to inflation readings. Roughly 70% of S&P 500 companies reported quarterly results the past two weeks and this week will be much slower, but there will still be about 7% of the index reporting this week. Notable results will come from Tyson Foods, Paramount Global, Skyworks on Monday; UPS, Datadog on Tuesday; Walt Disney, Trade Desk, Wynn Resorts on Wednesday; and Alibaba and Ralph Lauren on Thursday. The main event for the week will likely be the July consumer price index on Thursday. The consensus expectation is for a 0.2% increase in the month for both headline and core prices, but headline picking up to a 3.3% annual rate and core inflation remaining at a 4.8% annual rate. Elsewhere, on Tuesday we see trade data for June, jobless claims on Thursday, and the producer price index and consumer sentiment on Friday. Markets will likely pay attention to consumers’ inflation expectations in the consumer sentiment reading. Also, there may be increased focus on this week’s Treasury auctions for the 10-year Treasury note and 30-year Treasury bond due to the increased offering and higher yield.

By Wentz Financial|2023-08-09T09:22:46-04:00August 7th, 2023|Wentz Weekly|Comments Off on Wentz Weekly: U.S. Sees Credit Rating Downgrade For Second Time in History