Wentz Weekly: New Record, But Still Narrowly Driven By Few Names

Wentz Weekly Insights New Record, But Still Narrowly Driven By Few Names

New year, new record. It took almost exactly 24 months for the most followed U.S. stock index, the S&P 500, to reach a new record high. That happen Friday when the index closed at 4,839.81, almost 1% higher than the previous record set January 3, 2022. However, it may not feel like the markets just reached a record high. That is because, as was the case for almost all of 2023, stocks are seeing limited participation – the top, megacap names are driving a majority of the performance to start the year. The average stock fell last week, with the equally weighted S&P 500 down 1.25% while the cap weighted index rose 1.50%.

We were beginning to see some momentum in December with the average stock performing well and broad participation in the market’s rally from the October’s low. However, that seems to have faded through the first three weeks of the year. We think so for several reasons – caution over earnings, a small adjustment to rate cut expectations, and continued strength in mega cap stocks.

First, the strength in mega cap stocks appears to revolve around the continued optimism of artificial intelligence (AI). For example, Nvidia stock has risen 20% since the beginning of the year. The company is the forefront when it comes to AI as it develops the chips that goes into generative learning and most things AI related. Facebook parent company Meta is up over 8% as it was reported to be spending billions on chips for its AI efforts and Taiwan Semiconductor was up last week after saying profits were better than expected thanks to strong AI demand (Taiwan Semi produces the chips). Not to mention Microsoft making new record highs (and now the most valuable public company in the world), and Amazon and Google within reach of their respective highs.

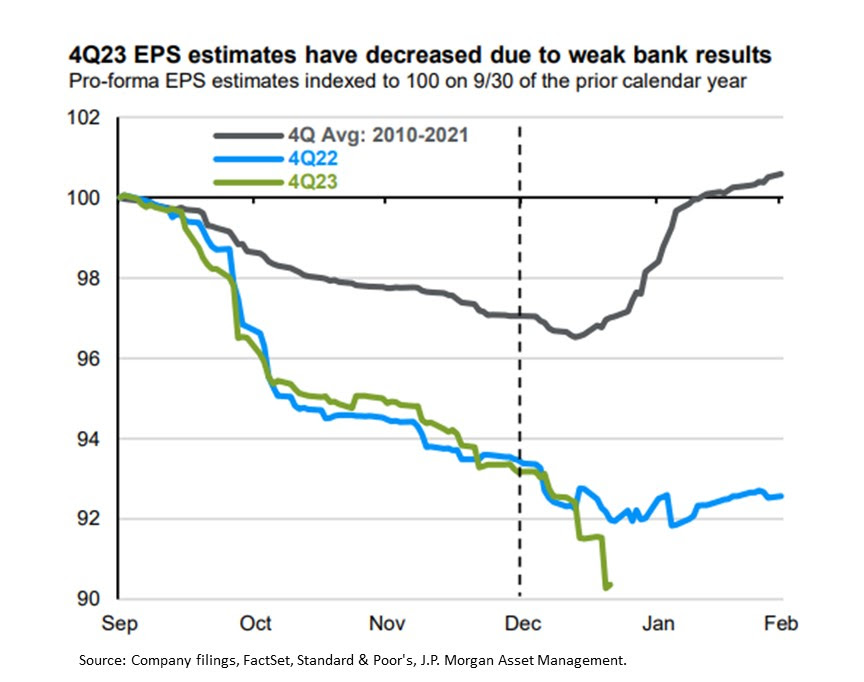

We are only two weeks into earnings season with roughly 10% of the S&P 500 companies having reported results already, although a majority of those have been financials. Earnings season got off to a slow start with estimates coming down slightly. On December 31, fourth quarter earnings in aggregate were expected to increase 1.6%, but as of Friday that expectation has moved lower to a 1.7% decline. Banks were the main reason as their profits were lower than expected, and most forecasted net interest margins (what banks make from interest it charges on loans minus what it pays on consumer deposits) lower than estimates for 2024 due to lower expectations on interest rates. The JPMorgan chart of the week below shows how earnings estimates historically fall heading into a quarter then quickly recover, versus the green line which shows earnings estimates falling much more than typical and, so far, continuing to fall.

Perhaps this biggest effect has been the small reset in market’s rate cut expectations. Coming into the new year, investors were betting the Fed would cut rates about 1.75% by the end of the year, equal to seven rate cuts (25 basis points each), according to interest rate futures pricing by the CME FedWatch Tool. Over the past couple weeks we have heard from a handful of Fed policymakers and the main message is rate cuts are not expected until at least the third quarter, that there is no reason to cut rates as rapidly as in the past, and a warning that if rates are cut too soon, the disinflation progress could stall. The result is Treasury yields (on the 10-year note) have risen back above 4.0% and the markets expectation is around 140 basis points of rate cuts this year (equal to 5-6 cuts) and the expectation for a rate cut in the March meeting dropped to 50%, down from about 80% before last week.

Now, markets have an important two weeks coming up. Almost half the S&P 500 companies are expected to report fourth quarter earnings over this period, including many blue chip, tech, and mega cap companies. Focus will be on 2024 forecasts and thoughts on consumer strength. Economic data will be in focus with the first Q4 GDP estimate and consumer data later this week and additional labor market data next week. Also on the list is central bank meetings. Several large central banks (European Central Bank, Bank of Canada, and Bank of Japan) hold policy meetings this week and the Federal Reserve holds its FOMC meeting next week where all eyes will be on rate cut expectations for 2024.

So, as Tom Barkin, the Federal Reserve President from the Richmond district bank, had said earlier this year – buckle up, even if there is a soft landing.

Week in Review:

US stocks started the week negative on a day that saw pushback on the market’s aggressive rate cut expectations from both the European Central Bank and the Federal Reserve. Fed Governor Waller said we are in “striking distance” of the inflation target but sees no need to cut rates as rapidly as in the past. Corporate highlights included additional scrutiny of Boeing over its MAX program, more earnings from financials, and a federal judge blocking the acquisition of Spirit Airlines by JetBlue. Stocks were lower across the board with the NASDAQ down 0.19% and S&P 500 losing 0.37% while Treasury yields rose across the curve.

A risk off tone is how the markets started trading Wednesday, coming after a weak day in Asian and European markets. Data was released from China that saw slower economic growth than expected in the fourth quarter and weaker retail sales, while data from Europe showed December inflation came in higher than expected. On the other hand, data from the US showed retail sales were again stronger than expected in December, leading to the thought the consumer and economy is still strong enough that rate cuts are not necessary yet, but the Beige Book said most Fed districts saw little or no change in economic activity over the past 6 weeks. Stocks had another down day as rate cut expectations for March fell. The S&P 500 fell 0.56% while Treasury yields were higher on the short end of the curve.

Events in the Middle East continued to grab attention with airstrikes back and forth between Pakistan and Iran while the U.S. launched its fourth round of airstrikes on Houthi rebels in Yemen. In the U.S., stocks got off to a great start Thursday, driven by tech, more specifically semiconductors, after Taiwan Semiconductor said it expects a better 2024 driven by investment in AI offsetting weakness elsewhere. Upside was limited though from more hawkish Fed commentary from Atlanta’s Bostic that he doesn’t see rate cuts until at least the third quarter. The S&P 500 gained another 0.88% with yields higher.

Friday saw an improvement in consumer sentiment data, helped by inflation expectations moving lower and asset prices moving higher. It was a quieter day with continued focus on Fed commentary and the pushback on aggressive rate cuts. Despite this markets strength continued with the S&P 500 gaining 1.23% and reaching a new record high for the first time in a little over 2 years.

It was a solid week for stock indexes, but market breadth has not been as strong as the equally weighted S&P 500 index underperformed by almost 3% for the week. The Dollar strength continued with the index up 0.9% for the week, gold fell 1.1%, oil was slightly higher with a 0.8% gain, and Bitcoin fell 4% as the excitement over the SEC approval of spot Bitcoin ETFs faded. The Treasury rally reversed with yields higher across the curve – the 2-year rose 24 basis points to 4.38% while the 10-year rose 19 bps to 4.13%. The major U.S. stock indices finished as follows: NASDAQ +2.26%, S&P 500 +1.17%, Dow +0.72%, and Russell 2000 -0.34%.

Recent Economic Data

Retail sales, once again, came in stronger than expected for the latest month of data. Sales in December rose a better than expected 0.6% and capped off 2023 with a 5.6% increase for the year. Unlike much of the past year or two, real sales (inflation adjusted) are trending more positive, with real sales up 2.2% (after accounting for 3.4% inflation rate) over the past year. In December, 8 of the 13 major categories saw an increase in sales, led by online sales up 1.5%, clothing stores up 1.5%, general merchandise stores up 1.3%, vehicle sales and parts up 1.1%, and miscellaneous store sales up 0.7%. Declines were seen in health/personal care sales down 1.4%, gasoline sales down 1.3%, and furniture stores down 1.0%. Over the year, restaurants and bars, vehicle sales, electronics, and health/personal care sales all saw increases of over 10%. The weakest categories over the past year have been gasoline sales due to the drop in gas prices and furniture and building material stores due to the large drop in home sales.

The Empire State Manufacturing survey index was a massive miss to the downside, with the index at -43.7 which was down nearly 30 points from last month. Outside the two months during the Covid lockdowns in 2020, this was the worst reading in history of the data series. New orders and shipments saw sharp declines, delivery times shortened with unfilled orders shrinking further, while employment declined modestly and the pace of input prices picked up somewhat. Optimism for activity over the next six months remained subdued.

After a almost record low reading on the Empire State manufacturing index earlier in the week, the Philly Fed manufacturing survey index came in at -10.6, about the same levels as December and reflects activity that continues to contract, but not as severe as the New York region. The indicators for general activity, new orders, and shipments all remained negative, but did rise slightly in the month. Employment was little changed with employment levels steady while prices overall continued to increase at a modest pace. Expectations on growth remain subdued.

Industrial production rose 0.1% in December, better than the small decline that was expected. The increase was due to a 0.1% increase in manufacturing, a 0.9% increase in mining, but offset from a 1.0% decline in utilities which is very correlated to weather conditions. Industrial production was up 1.0% in 2023, driven by mining that grew 4.3%, manufacturing that grew 1.2%, and offset by a 4.9% decline in utilities. Capacity utilization was 78.6%, slightly lower than expected and still lower than the historical average, but improving over the past year.

Prices of goods/services imported to the U.S. were unchanged in December, following two consecutive monthly declines. Import prices are still down 1.6% from a year ago. Export prices fell 0.9% in the month, the third consecutive month of a 0.9% decline, bringing prices 3.2% lower from a year earlier.

The housing market index, an index on homebuilder sentiment, rose to 44 in January, up from a very low level of 34 in December (an index level below 50 indicates contracting activity). The index on present sales improved to 48, up from 41, the index on future sales rose considerably to 57, up from 45, while the index on traffic of potential buyers remains depressed at 29, though up from 24. The index levels are still historically low, but a notable improvement from one of the most depressed months on record in December.

The number of housing starts in December fell 4.3% to a seasonally adjusted annualized rate of 1.460 million, although 7.6% above the December 2022 levels. After a strong recovery after the pandemic, housing starts have declined and have now been trending in the 1.400 million range. The number of permits to build a new home rose 1.9% to an annual rate of 1.495 million, and 6.1% above the level from a year earlier. The data is similar for permits, where it has been trending in the mid to upper-1.400 million range after a strong post-pandemic recovery. the number of homes currently under construction has been relatively consistent around 1.680 million.

Existing home sales fell 1.0% in December to a seasonally adjusted annualized pace of 3.780 million homes. On an annual basis, there were 4.090 million existing homes sold in 2023, the lowest level in almost 30 years (since 1995) and falling 19% from 2022 levels and 34% from 2021. Meanwhile, the median sales price reached a record high of $389,800, up 4.4% over the past year, due to the very limited supply of existing homes on the market. In fact, inventory of homes for sale fell 12% in the month to 1 million units as existing homeowners are preferring to stick with their low rates locked in during the pandemic and reluctant to switch homes and incur a higher mortgage rate. Existing homes sales are based on closings so this data reflects homes that went under contract in November when rates began to decline from multi-decade highs.

The number of unemployment claims filed the week ended January 13 was 187,000, a decline of 16k from the prior week with new jobless claims now at the second lowest level since the late 1960s (the pandemic low was September of 2022 of 182,000). The four-week average fell 5k to 203,250. Meanwhile, the number of continuing claims was 1.806 million, down 26k from the prior week and falling back to October lows. The four-week average was 1.848 million, down 14k from the prior week.

Mortgage rates fell to the lowest level since last May, with the average prime 30-year mortgage rate standing at 6.60% last week, according to the Freddie Mac weekly mortgage survey. This is down from the cycle and multi-decade high of 7.79% in October. With Treasury rates lower and the Fed expected to lower rates sometime in 2024, the average mortgage rate is expected to fall back below 6% this year.

Company News

A federal judge has decided to blocked JetBlue’s planned acquisition of Spirit Airlines due to anticompetitive concerns, coming after a lawsuit from the Department of Justice to stop the merger. The judge said the deal would drive up airfares for price-sensitive consumers by taking a discount carrier out of the market. The companies argued the combination would help them grow and compete better with larger rivals. The merger would have created the fifth largest airline. Some now believe Spirit may look for another buyer or, more likely, will file for Chapter 11 bankruptcy. A WSJ report said Spirit Airlines will explore options on how it could address its finances and is looking to refinance its debt and not engage in a restructuring. The company’s short term debt includes about $1.1 billion in debt due September 2025.

Shares of iRobot fell about 40% after a report was released that EU regulators are planning to block Amazon’s planned acquisition of the company. The WSJ report said the European Commission met with Amazon representatives on Thursday to discuss the transaction and was told the deal would be rejected. This comes a couple days after a report said Amazon refused to offer concessions to EU regulators to try to appease them. US regulators were also said to have concerns about the acquisition.

According to reports by the New York Times, using information from Apple’s China website, Apple is beginning to cut the price of its iPhones by up to $70, equal to about 6% to 8% discount, in China due to weaker consumer demand and increasing competition from other smartphone makers. Separately, other reports say Apple will begin selling versions of its Watches without the blood oxygen measurement feature which followed lawsuits against the company over a patent dispute with Misimo. The Court told Apple it will implement an import ban which means the company must stop selling its Watches that include the blood oxygen feature.

Job cuts – Wayfair announced it will cut about 13% of its workforce, equal to about 1,650 employees. Macy’s is reported to be cutting 3.5% of its workforce, equal to about 2,300 employees, along with closing five additional stores.

A month after cutting its electric vehicle production by 50%, Ford said it will cut its production of EVs even further and shift that production to the production of its all gas Bronco and Ranger lines.

Other News

The government was set to run out of funding for some agencies January 20, then fully run out of funding February 2 when it would have to “shut down,” but late last week another stopgap bill was passed to keep the government funded for another several weeks, allowing it about another six weeks to negotiate a longer-term solution. The new deadline is March 1, then March 8 when it would see a full shutdown if no deal were made. The January 20 deadline came after a previous stopgap deal was passed late last year.

Container shipper Maersk said that weather disruptions at northern European ports and the diversion of vessels away from the Red Sea is causing congestion at many container terminals, and it is asking customers to pick up container units as quick as possible to support fluidity at the ports. It added the disruption to global shipping is expected to last at least a few months and asked customers to prepare for complications to persist and for a possible significant disruption to the global shipping network. A separate report from Bloomberg said traffic through the Suez Canal dropped to the lowest level since the 2021 blockage.

The Biden Administration said it would cancel another $4.9 billion in student loan debt for some 74k borrowers. Those affected include those who were in the income-driven repayment plan and public service loan forgiveness plan who had at least 10 years of payment or service in a public job. The Dept of Education has now announced a cumulative total of $136 billion in student loan forgiveness for about 3 million borrowers.

Fed speak:

Fed Governor Chris Waller said we are within “striking distance” of the Fed’s 2% inflation target and downplayed the market’s aggressive pricing of rate cuts this year. He said the Fed can cut rates this year if inflation does not show signs of rebounding, but there was no reason to cut rates as quickly as the Fed has done in the past and it should be done “methodical and careful,” adding there is risk that rate cuts could be delayed further if the economy does not moderate as expected.

Atlanta Fed President Raphael Bostic said he does not see the Fed cutting rates until at least the third quarter, and emphasized that progress on inflation moving lower could stall if the Fed cuts rates too soon.

Thursday, February 1 – 6:00 pm – WFG Auditorium in Hudson, OH

Thursday, February 8 – 12:00 pm – WFG Auditorium in Hudson, OH

Thursday, February 8 – 6:00 pm – WFG Auditorium in Hudson, OH

Wentz Financial Group will be holding its semi-annual Economic and Market Outlook Seminars on the dates above. Join us as we recap a surprisingly positive 2023, explain how we got to where we are today, as well as give our expectation and forecast on the economic and market environment and how that will affect portfolios in another challenging year ahead. We will have three seminar times, one during the lunch hour and the other two in the evening. Please RSVP by responding to this email or by calling the office at 330-650-2700. Seat are limited for each event and will be on a first come first served basis. A buffet style meal will be served approximately 30 minutes before each event.

The Week Ahead

Activity picks up this week with a busy week of earnings reports, economic data, and geopolitics. We will see a break in the Fed schedule though, as policymakers will be in a blackout period ahead of next week’s FOMC meeting and policy decision. The earnings calendar sees about 15% of S&P 500 reporting fourth quarter results this week with many blue chip companies. Notable results will come from United Airlines on Monday, Netflix, Verizon, GE, Johnson & Johnson, Procter & Gamble on Tuesday, Tesla, IBM, CSX, AT&T on Wednesday, Visa, Comcast, Southwest Airlines, American Airlines, Intel on Thursday, and American Express on Friday. The economic calendar is not as busy but still includes key reports on the economy including the first estimate on fourth quarter GDP and consumer figures for December. Economic growth is seen coming in between 1.5% and 2.0% (annualized) in the fourth quarter, after a very strong 4.9% from the third quarter. The personal income and outlays report is expected to show a 0.4% increase in incomes and consumer spending but the price index bouncing back with a 0.2% increase in December. Elsewhere, we will see money supply, new home sales, durable goods orders, jobless claims, and the pending home sales index all next week. While we wait next week for the Fed’s policy announcement, this week we will see meetings and policy decisions from the European Central Bank, Bank of Canada, and Bank of Japan. No change in rates or any major policy announcements are expected at either meeting. And geopolitics is mentioned due to the ongoing conflicts in the Middle East as well as Congress working on a 2024 budget and the upcoming Republican primaries where Trump continues to dominate.

By Wentz Financial|2024-01-22T15:52:44-05:00January 22nd, 2024|Wentz Weekly|Comments Off on Wentz Weekly: New Record, But Still Narrowly Driven By Few Names