Wentz Weekly Insights

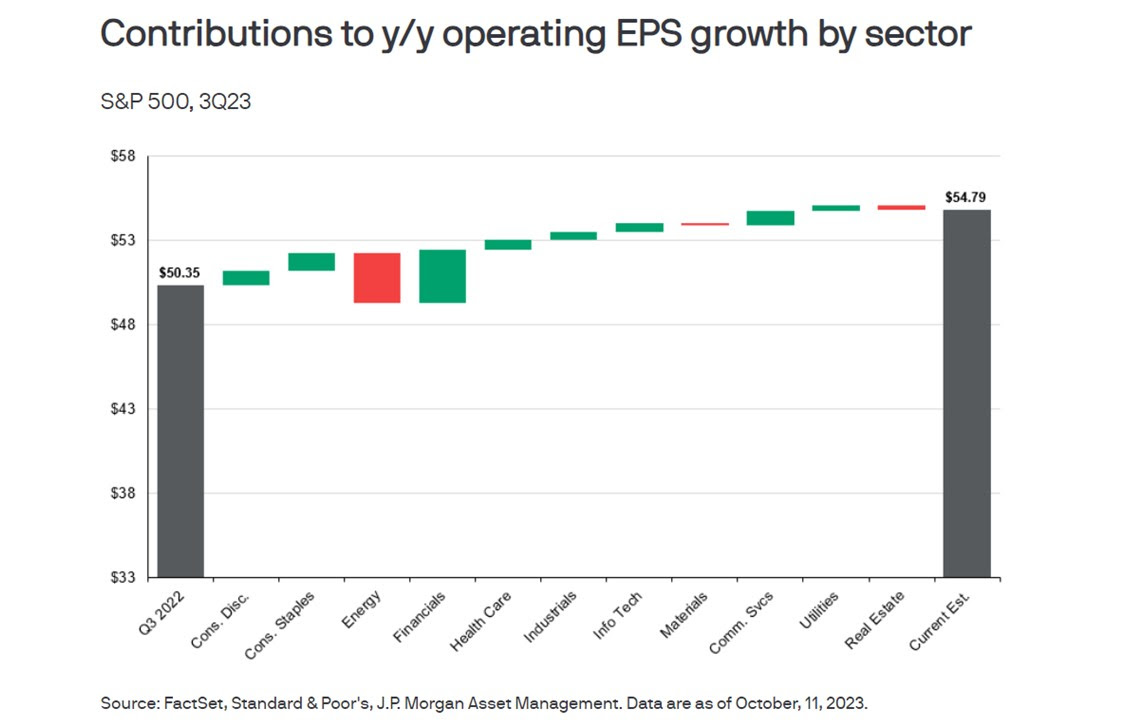

Third Quarter Earnings Preview

Recent Economic Data

- Inflation at the consumer level was a little higher than expected in September. The consumer price index rose 0.4% in the month, slightly more than the 0.3% increase expected, coming after a 0.6% increase in August. The index was expected to fall to a 12-month increase of 3.6% but stayed at 3.7% in September. The index for energy prices was up 1.5% in September, after a 5.6% increase in August, due to higher oil prices, while food prices remained stable, rising 0.2%. Excluding these two volatile categories gives us the core index where it rose 0.3% as expected, matching August’s increase after two months of increasing 0.2% which happened to be the lowest since February 2022. Core prices were up 4.1% from a year ago, down from the 4.3% 12-month increase in August and have not been below 4.0% since May 2021. In the core index there were several categories with lower prices including used vehicles, apparel, and medical care, while shelter increased 0.6% and transportation continues to run hot, rising 0.7% (up 9.1% y/y). Insurance costs is an interesting one – both vehicle and home insurance are up double digit pace over the past year, while health insurance costs are down 37%. The Fed’s closely followed “super core” index rose at a faster 0.6% rate in the month, up 3.8% over the past 12 months, but is concerning as the 3-month annualized pace was 4.8%, much hotter than the Fed’s 2% target.

- Prices producers pay rose at a faster pace than expected in September. The producer price index rose 0.5% in the month, higher than 0.3% expected and are 2.2% higher from a year earlier, increasing from the 1.7% annual pace in August. Final demand goods prices rose 0.9%, driven by a 3.3% increase in energy prices and 0.9% increase in food prices, while final demand services prices increased 0.3%, driven by trade up 0.5% and offset by a 0.4% decline in transportation/warehousing. The less volatile core index that excludes food, energy, and trade prices, rose 0.2% as expected and is 2.8% higher than a year ago.

- The price index for US imports increased a less than expected 0.1% in September after a 0.6% increase in August which was the largest monthly increase in 15 months. Prices were driven by fuel products, offset by a decline in prices for non-fuel goods/services. Prices of imports are still down 1.7% over the past 12-months. The price index for goods/services exports from the US rose 0.7% in September, after a 1.1% increase in August which was also a 15-month high. The increase was driven by industrial supplies, vehicles, and capital goods, offset by declines in agricultural and consumer goods. Prices of exports are still down 4.1% from a year ago.

- The number of unemployment claims filed the week ended October 7 remains low at 209,000, unchanged from the prior week. The four-week average declined slightly to 206,250. The number of continuing claims was 1.702 million, up 30k from the prior week, with the four-week average relatively unchanged at 1.674 million.

- The flash reading on October consumer sentiment index, based on the survey compiled by the University of Michigan, was 63.0, a drop from 68.1 in September where the index has held steady for about two months, and for the worst reading since May this year. The index on current conditions was 66.7, down from 71.4 in September, while the index on expectations fell to 60.7 from 66.0 in September, also the weakest level since May. One of the more important readings is expectations on inflation over the next 12 months which increased to 3.8% from 3.2% in September (which was the lowest since March 2021) for the highest since May, and remains well above its long-term range of about 2.5%. Inflation expectations over the next five years moved to 3.0%, up from 2.8%.

Company News

- Exxon Mobil confirmed it has agreed to acquire Pioneer Natural Resources, the second largest oil producer in the Permian Basin, for $59.5 billion, or $253/share in an all-stock deal. The is approximately a 18% premium to where shares traded prior to the initial report last Thursday. The terms of the deal say Pioneer shareholders will receive 2.3234 shares of Exxon for each Pioneer share owned.

- The United Auto Workers union said it would expand its strike to its Kentucky truck plant, which has about 8,700 UAW members, and in which is one of Ford’s most profitable plants. UAW said it is making the move after Ford refused to make progress on bargaining. Bank of America analyst estimates each week of work stoppage would equate to a $247 million hit to EBIT for Ford, which is equal to about $0.05 in EPS, and would bring the total, between all plants it is striking, to $430 million in EBIT loss per week. In comparison, Ford’s 2023 EBIT is estimated to be around $10.7 billion. An estimated 30% of US vehicle production by the big three automakers is now affected by strikes.

- Microsoft said it has received a notice from the IRS that it owes $29 billion in backed taxes, plus interest and penalty, from 2004 through 2013. Microsoft responded that it believes its “allowances for income tax contingencies are adequate,” and it will challenge the IRS notice.

- After a long battle with regulators, Microsoft closed on its acquisition of Activision Blizzard on Friday.

Other News

- The Congressional Budget Office released its monthly budget review that provided estimated fiscal year 2023 deficit numbers. According to the report, the federal budget deficit was $1.690 trillion in the fiscal year (the 12-month period ended September 30), $315 billion or 23% more than fiscal year 2022’s deficit. If it was not for a timing difference (October 1 falling on a weekend in 2023), the deficit would have been 28% higher in 2023 versus 2022. The larger deficit was due to a $455 billion, or 9%, decline in tax revenues, offset somewhat by a $141 billion, or 2%, decline in outlays. However, the deficit was skewed from the planned (and later struck down by the Supreme Court) cancellation for student loan debt. If this was excluded from fiscal 2022 and 2023, the deficit in 2022 would have been $900 billion and the deficit in 2023 would be estimated to be $2.0 trillion, indicating a $1.1 trillion increase in the deficit in fiscal year 2023. One of the consequences of higher interest rates is the cost to service the U.S. debt is growing. Net interest on the debt increased $177 billion, or 33%, in 2023 to a total of $711 billion.

- The FTC said it will propose a new rule that would ban junk, or hidden, fees that are charged by businesses such as hotels/resorts, airlines, concert tickets, utility bills, etc. The FTC last year opened public comments on how consumers are affected by junk feeds where a common complaint was sellers do not advertise the total amount they have to pay, disclosing the fee only at the point where the transaction was submitted.

- Recent comments by Fed policymakers:

- Vice Chair Philip Jefferson said he is seeing evidence the imbalance between labor demand and supply is narrowing while saying he will take into account the recent surge in Treasury yields when assessing future policy decisions. He added policy is at a “sensitive period” because of the balance of risks in tightening too much versus not enough, and this was a reason for holding rates unchanged at the prior meeting.

- Atlanta’s President Bostic said “I actually don’t think we need to increase rates anymore,” adding that if unexpected developments impact the outlooks, it may require more rate hikes. A week ago, he mentioned he sees one more rate increase by the end of the year.

- Governor Michelle Bowman reiterated that rates could go higher and stay there for some time, but also talked about the increased risks the Fed faces regarding financial stability, citing the sizeable move in interest rates and geopolitical tensions/conflicts. She added that failing to get inflation back to target would lead to greater financial stability risks.

- Minneapolis President Kashkari spoke on the recent spike in 10-year Treasury yields, saying it is a “little bit perplexing.” He said the Fed is assessing whether there is more optimism that economic growth will be stronger for the next five to ten years. He added it could be that investors believe the Fed could be more aggressive, which he called a head scratcher, or that the rise reflects increased US debt issuance. He also said it is possible that the higher yields could help in bringing inflation lower.

- Philly Fed President Patrick Harker said that “absent a stark turn in what I see in the data and hear from contacts,” the Fed is at a point where it can hold rates at these levels due to the progress it has seen in inflation and its downward trajectory. He added “I am sure policy rates are restrictive, and as long they remain so, we will steadily press down on inflation and bring markets into a better balance.

Did You Know…?

Bank’s Issue With Higher Rates:

Social Security Raise:

WFG News

Medicare Open Enrollment

- Medicare Open Enrollment period runs from October 15 to December 7 each year

- During this period, individuals are able to make changes to their current Medicare coverage. Individuals on Medicare should receive an Annual Notice of Change and/or Evidence of Coverage for Medicare Advantage or Part D plan. This is a good time to review coverage, as medical needs, benefits, and premiums may have changed over the year. During this time here are some things to consider:

- Will your primary doctor still accept you Medicare Advantage Plan?

- Have your medical needs changed? Different plans offer different benefits and different costs

- Are there comparable, lower cost plans available? Don’t forget to consider out-of-pocket costs when comparing options

- Are you medications still on your plan’s list of covered medications?

The Week Ahead

Market participants will be busy assessing many things this week from geopolitics to earnings and more economic data. In the Middle East, the focus will be on how/if Israel escalates the conflict with a full ground invasion as it has warned. Oil markets have been paying close attention, particularly if the conflict escalates and involves other nations, due to the amount of production that comes from the Middle East region. In the US, the House still needs to elect a new Speaker with a government shutdown deadline just one month away. Economic data releases will include updates on the housing sector and more consumer spending data. The housing market index comes out Tuesday, housing starts and permits on Wednesday, and existing home sales on Thursday. Retail sales for September will be released Tuesday where economists are estimating sales rose 0.3%, which would be one of the smallest increases in months. We will also see manufacturing updates with the Empire State and Philly Fed manufacturing surveys, and industrial production. Fed speak will continue to be a big topic as well with many more policymakers lined up to speak this week including Chairman Powell on Thursday afternoon. Earnings reports will ramp up this week before entering the busiest period of the quarter next week. Notable companies reporting quarterly results this week include Charles Schwab on Monday, Johnson & Johnson, Bank of America, Goldman Sachs, Lockheed Martin on Tuesday, Tesla, Procter & Gamble, Netflix on Wednesday, Union Pacific, CSX, American Airlines, AT&T on Thursday, and American Express on Friday.