Wentz Weekly Insights

Stocks Fall as U.S. Bond Yields Continue to Rise, While Labor Market Data Comes in Mixed

Recent Economic Data

- The PMI Manufacturing index shows manufacturing activity continues to decline with the index at 49.8, although a small improvement from 47.9 in August. A reading over 50 indicates growing activity/conditions and under 50 is contracting conditions. Domestic and international demand remained “subdued,” but conditions declined at a reduced pace. The small improvement in the index was due to a return to growth in output as production grew at the best pace since May and as employment increased, however new orders were still down. Input prices rose at the fastest pace since April as oil affected overall price increases. It was the tenth time in the last 11 months that the index was in contraction territory (below 50).

- The ISM manufacturing index remained in contraction territory as well for the 11th consecutive month with a reading of 49.0, although improved slightly from a 47.6 in August. New orders declined for the 13th consecutive month but at a slower pace, while production moved positive. Prices paid was 43.8, the best since May indicating slower growth in prices, while employment was 51.2 for the first positive in months. Only 5 of the 18 industries reported growth in the month. Only five.

- Factory orders in August were up 1.2%, the best monthly growth since June’s 2.3% increase and 1.0% above expectations, recovering from a 2.1% decline in the month prior. Shipments of orders grew 1.3% and comes after a 0.7% increase the month prior. The final read for August shipments of nondefense capital goods excluding aircraft, an input to GDP, was an increase of 0.7%, coming after a 0.3% decline the month prior.

- Spending on construction in the US continues its somewhat surprisingly strong streak, rising 0.5% in August however is the lowest increase since April. Residential construction spending grew 0.6%, continuing to bounce back after a long declining streak to start the year. Residential spending is still down 3.0% from last year’s levels, down 9.1% from the peak May 2022, but still 44% higher from pre-pandemic levels. Nonresidential spending has been a bright spot this year, perhaps driven by the infrastructure spending bill. Nonresidential spend was up 0.4% in August, up 17.6% from a year ago, up 24% from pre-pandemic levels, and reached a new record high in the month. These are positive for GDP calculations.

- The ISM services index was 53.6 in September, slightly lower than expected, lower than the 54.5 last month for the weakest in three months, however importantly remaining in ‘expansion’ territory. The new orders index of 51.8 fell 5.7 points from September for the slowest new order growth since the end of 2022. The employment index fell 1.3 points to 53.4 while prices index was unchanged at a still elevated 58.9, remaining a concern as it is at the highest level since April. For September 13 of the 18 services related industries reported growth.

- The monthly US trade deficit in August was $58.3 billion, narrowing from July’s $64.7 billion deficit and is the smallest deficit since the middle of the pandemic June 2020. The narrower deficit was due to less imports and a growth in exports. Imports fell 0.7%, or $2.3 billion, to $314.3 billion while exports increased 1.6% or $4.1 billion, to $256.0 billion. The trade deficit is important for GDP, this number will give a boost to the Q3 number, but for the economy the bigger factor is the volume of trade. Year-to-date through August, imports have declined 4.3%, or $115.6 billion, suggesting domestic weakness, while exports have grown 1.1%, or $22 billion.

- The number of job openings on the last business day of August was 9.610 million, an increase from the two-year low of 8.920 million in July and moving back to the highest level since April. For reference, the all-time high was 12.027 million in March 2022, while the pre-pandemic trend was around 7 million. Total separations (quits, layoffs, etc) were little changed at 5.676 million, with quits slightly higher, making up 3.638 million of total separations, still near the lowest level since early 2021.

- ADP data showed private payrolls increased 89,000 in September, lower than the 150,000 increase expected and the slowest pace of payroll growth since January 2021 when there were job losses. Small and mid-sized businesses saw solid payroll gains while large establishments saw nearly 100k in payroll declines. The average monthly payroll growth through the first nine months this year is 235,000, down from 306,000 in 2022.

- Jobless claims, both new claims and continuing claims, held pretty steady in the latest week of data. The number of initial unemployment claims filed the week ended September 30 was 207,000, up just 2k from the prior week and remaining at the lowest levels of the year. Continuing claims declined 1k to 1.664 million with the four-week average down 5k to 1.667 million.

- The labor market continues to improve, with job growth picking up pace in September, according to the latest data by the Department of Labor. According to its establishment survey, 336,000 jobs were added in the month, over double the expectation by economists and 70,000 higher than the average gain of the past 12 months. All but one major industry saw job gains in the month, with the most seen in leisure & hospitality (+96k), government (+73k), and health care (+41k). Wages increased by 0.2%, a little lighter than expected, matching last month’s increase which was the lowest in 18 months, and are 4.2% higher from a year ago, down from the 4.3% 12-month pace in August. The household survey showed the labor force grew 90k, keeping the labor force participation rate at 62.8%, which is the highest since the pre-pandemic days when it was trending at 63.3%. The number of people employed increased 86k to 161.570 million while those unemployed was relatively unchanged. This kept the unemployment rate at 3.8% and made the underemployment rate, or the U-6 rate, drop 0.1% to 7.0%. Also important, the last two month revisions saw job gains 119,000 higher than the initial data suggested (July job gains of +236k and August of +227k), which was a surprise. Every other month this year has seen relatively large downward revisions.

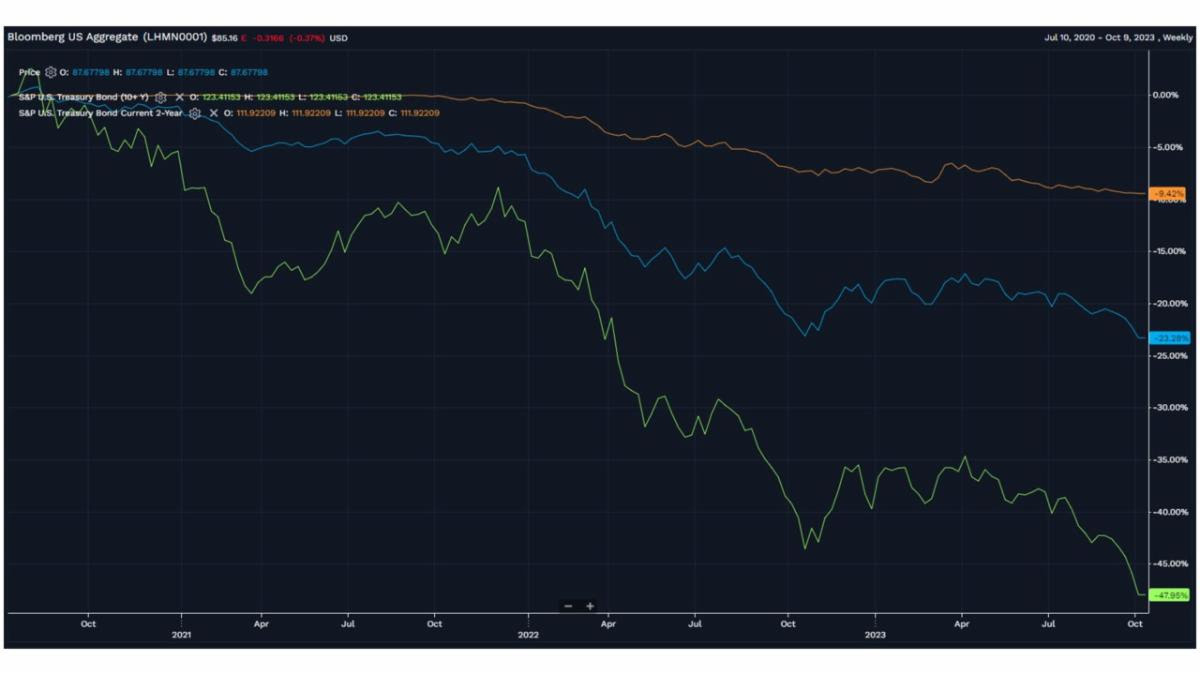

- Mortgage rates continue to move higher, following the move in long term Treasury yields. The average prime 30-year mortgage rate was 7.49% in the latest week, according to data from Freddie Mac. This is a 18 basis point increase from the prior week, and is 1.05% higher than when the year started.

Company News

- Viatrus, the generic drug business that spun off from Pfizer, said that in part of its planned divesture, it has agreed to sell its over-the-counter business, its women’s healthcare business, and its pharmaceutical business in India. The gross proceeds will be nearly $7 billion and will be used to pay down debt.

- Macy’s said it will expand on its small store format strategy and will look to triple the number of those smaller format stores by the fall 2025. It expects 30 new small format stores next year. The small format stores are about 30k-50k square feet, compared to about 200k square feet for its traditional stores.

- Facebook parent company Meta is reportedly proposing a new plan to European regulators to introduce ad-free subscription plans for its Facebook and Instagram users in the region, according to the WSJ. It said it would charge users about 10 euros/month for accounts on desktop, and 13 euros/month on mobile due to fees paid to Apple/Google, plus 6 euros/month for additional accounts. The move would be an alternative to current/proposed European regulations which would restrict its ability to show personalized ads to users without asking for consent first.

- According to a Reuters report, Boeing plans to increase its output of 737 narrowbody jets to at least 57 per month by July 2025, which would be record production for the company. For comparison, this year it has delivered an average of 34 737 jets each month.

- Kellogg announced it has completed the spin off of its cereal business and the new company, “WK Kellogg Co,” began actively trading last week. In conjunction with the spinoff, the parent company Kellogg has been renamed to Kellanova, which includes snack brands and its North American frozen food business. At the spinoff, shareholders of Kellogg received one share of KW Kellogg for every Kellogg share they owned.

- The WSJ reported Netflix is looking to raise prices a few months after the Hollywood/actor strike ends. It says the price increases could start in the US and Canada and then roll out internationally.

- AT&T is reportedly exploring options on its joint venture where it holds a 70% stake in DirecTV. Sources say the options include a dividend recapitalization, adding a new investor, or selling the holding and exiting the joint venture as early as August 2024. Its three-year commitment with the co-owner, private equity group TPG, ends at the end of July 2024. AT&T acquired DirecTV in 2015 for $48.5 billion, then spun it off to TPG in 2021 with a valuation of $16 billion, receiving $7.8 billion while retaining a 70% ownership.

- Exxon Mobil said it expects a $2.1 billion boost to operating profits compared to its last projections due to higher oil prices for crude, natural gas, and fuel products. It now expects operating profits in the range of $8.3 to $11.4 billion. It sees a $1.1 billion boost from higher crude prices, $1 billion from refining, and $400 million from higher gas prices, partially offset by losses in chemicals.

- Separately, a report late Thursday by the WSJ said Exxon Mobil is close to a deal to acquire oil producer Pioneer National Resources for $60 billion, approximately a 20% premium to where shares traded prior to the report. Pioneer is the second largest oil producer in the Permian Basin, an oil rich region in Western Texas.

Other News

- In an unprecedented event, the House ousted its Speaker Kevin McCarthy after a small group of Republicans brought a vote to remove him from his position. This comes after Congress passed a continuing resolution to avoid a government shutdown, prior to the October 1 deadline, and keep the government funded for 45 additional days until Congress can agree to a full year budget. A number of Republicans, mainly the far right, succeeded in removing McCarthy as they were pushing for deeper spending cuts. Things can still move forward through the House without a Speaker but will be a much more difficult and lengthy process. A vote on a new Speaker will take place October 11.

- Last week, OPEC+ held its monthly committee meeting with members not recommending a change to production quotas. Saudis and Russia said they would continue with their voluntary production cuts through the end of the year, despite the rise in oil prices. Both members have said the cuts are needed to stabilize the oil market.

- Central Bank – Notable Remarks:

- Vice Chair of Supervision Michael Barr said “the most important question at this point is not whether an additional rate increase is needed this year or not, but rather how long we will need to hold rates at a sufficiently restrictive level to achieve our goals.” He expects below potential economic growth over at least the next year as economic activity is restrained from tighter policy which is expected to slow the labor market.

- Fed Governor Michelle Bowman said she expects multiple interest rate hikes may be required, citing continued risks that “higher energy prices could reverse some of the progress we have seen on inflation in recent months.” She made similar comments in September, and since then we have seen several inflation readings, which apparently have not changed her stance.

- San Francisco President Mary Daly repeated recent comments that rates can remain at these levels if the labor market and inflation continue to cool and left the door open for additional rate hikes if those data points continue to strengthen. She added the recent rise in Treasury yields is equivalent to about one rate hike, which gives the Fed less reason to tighten policy further.

- Meanwhile, Richmond’s President Barkin said the surge in yields reflects stronger economic data and heavy supply of Treasuries due to an increase of new issues by the government. He was undecisive on whether another rate hike would be necessary, preferring to wait for more data.

Did You Know…?

Retail “Shrink”

A report by the National Retail Federation shows that theft at retail stores jumped 20% in 2022 compared to 2021. The level of shrink, which is the loss of inventory from a store or warehouse without being paid for, things like theft and shoplifting, rose from $93.9 billion in 2021 to $112.1 billion in 2022. The numbers reflect a study of 177 retail brands that accounted for $1.6 trillion worth of retail sales in 2022. The amount of theft is more than likely to increase again in 2023, possibly at a higher pace than in 2022. Shrink was a major topic of discussion on retailers’ earnings conference calls this past quarter and was one of the reasons many retailers reported lower than expected profits. In fact, Target recently said it would close nine stores in several major US cities due to organized crime theft and increased violence.

WFG News

Medicare Open Enrollment

- Medicare Open Enrollment period runs from October 15 to December 7 each year

- During this period, individuals are able to make changes to their current Medicare coverage. Individuals on Medicare should receive an Annual Notice of Change and/or Evidence of Coverage for Medicare Advantage or Part D plan. This is a good time to review coverage, as medical needs, benefits, and premiums may have changed over the year. During this time here are some things to consider:

- Will your primary doctor still accept you Medicare Advantage Plan?

- Have your medical needs changed? Different plans offer different benefits and different costs

- Are there comparable, lower cost plans available? Don’t forget to consider out-of-pocket costs when comparing options

- Are you medications still on your plan’s list of covered medications?

The Week Ahead

This week’s focus will be on inflation as the next consumer price index report is released on Thursday morning. Economists estimate inflation increased 0.3% in September, coming after a larger 0.6% increase in August, as energy prices continued to move higher. The most important number, core price over the past 12 months, is expected to have increased 4.1%, cooling from 4.3% in August. Other data releases on the calendar include the producer price index on Wednesday, jobless claims on Thursday, import and export prices and the consumer sentiment reading on Friday. The FOMC will also release the minutes from its most recent September meeting Wednesday afternoon where investors will look for additional clues on future interest rates. In addition, there will be a number of Fed policymakers making public speeches throughout the week. The other big focus will be the beginning of third quarter earnings season later in the week. Earnings season is typically kicked off with the big banks – on Friday JPMorgan, Citigroup, and Wells Fargo will all release their quarterly results. Other notable reports this week include PepsiCo on Tuesday, Delta Airlines, Fastenal, Walgreens on Thursday, and UnitedHealth and Progressive on Friday. Politics will be at top of mind as well after the recent attacks in the Middle East and the ongoing issues in Congress with electing a new House Speaker and continuing negotiating a longer-term budget plan for the new fiscal year to keep the government funded.