Wentz Weekly Insights A Higher Neutral Interest Rate?

Stocks saw their worst performance last week since the banking crisis in March with a 2.93% decline in the S&P 500 as longer-term Treasury yields rose to new 16-year highs. It was a risk off week with growth underperforming value stocks – consumer discretionary stocks lost 6.35% while consumer staples were down just 1.78%. Meanwhile, the 10-year Treasury note saw selling pressure as its yield rose to a high of 4.51%, the highest since October 2007, and was up 11 basis points on the week, while the shorter-maturity 2-year note’s yield rose to a high of 5.20%.

What was the reasoning for the move? A Fed projecting higher interest rates for longer. Yes, we have heard this many times over the past several months, with remarks from Chairman Powell to comments from many different district presidents. However, we saw it updated in the Fed’s summary of economic projections – the quarterly forecast from 19 of the Federal Reserve decision makers on things such as employment, inflation, economic growth, and interest rates.

The Federal Open Market Committee (FOMC) voted to keep rates unchanged at 5.25%-5.50% as widely expected, while keeping its balance sheet unwinding plans unchanged (selling Treasury securities in the open market). The policy statement was basically unchanged from the July meeting, expect it noted the economy is growing at a “solid” pace, upgraded from a “moderate” pace.

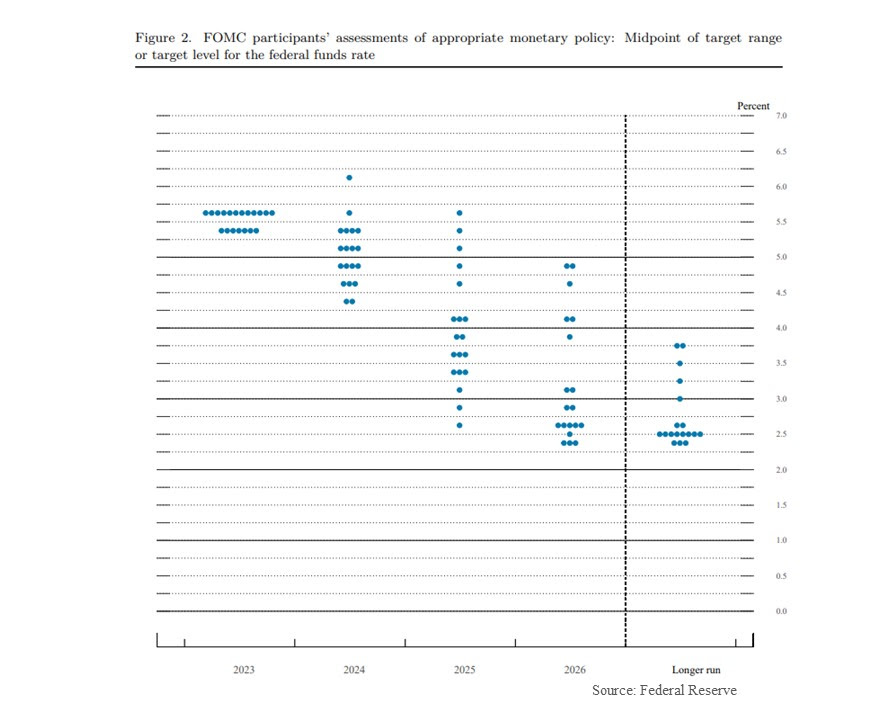

This wasn’t the focus though. We knew going into the meeting all attention would be on the “dot plot.” This is a chart (seen below) on where all 19 policymakers see rates by the end of the current year, along with the next three years, and longer-term.

There remains a bias to raising rates and a bias to keeping rates much higher for much longer, and this is where markets were slightly surprised. The dots show 12 of the 19 policymakers see at least one additional rate hike this year (the street was expecting less). In addition, the interest rate forecasts by policymakers for 2024 and 2025 moved higher than what was expected. The average dot sees rates ending 2024 at 5.1%, up from 4.6% in the June projections, indicating just two rate cuts next year. The end of 2025 rate projections were 3.9%, up from 3.4% in June, indicating just 1.75% or seven rate cuts over the next two years.

At the same time, projections on inflation were relatively unchanged while projections on economic growth moved higher. Projections on economic growth in 2023 was nearly doubled while 2024 was +1.5%, up from 1.1%. Meanwhile, unemployment projections moved lower (2024 projections at 4.1%, down from 4.5%). It was interesting to see stronger growth, stronger labor market, but unchanged inflation and also see rate projections move higher by 50 basis points. This was a question in the press conference to which Chairman Powell said because of stronger economic activity, participants chose to raise rate forecasts.

The Fed appears to believe, and based on market reaction, that the neutral rate is higher than previously thought because the economy has been able to absorb and handle higher rates better than believed. As Powell said “this is part of the explanation on why the economy has been more resilient than expected” and “it is certainly plausible that the neutral rate is higher.” This explains the move higher in longer term Treasury yields. The neutral rate is a theoretical interest rate that is neither accommodative or restrictive, that is it neither supports or restricts/slows economic activity.

Of course, the projections are not preset policy, they are where Fed members forecast things given today’s information. Powell indicated they still do not know how long rates will stay high but will know when they see it. He reiterated the recent good inflation data that has been observed is encouraging but they still want to see more than three months of data to be convinced it is moving back to its 2% target.

We are in a seasonally weak part of the year so the recent 6% pullback in stocks was not totally unexpected. The Fed will remain data-dependent and this will keep increased focus on the upcoming data. Next on the calendar is the PCE price index on Friday in the personal income and outlays release (which include wage and spending data) which happens to be the Fed’s favorite inflation reading. The consensus estimate sees a stronger 0.5% monthly increase in prices in August, stronger due to higher energy prices, with a 3.9% increase in the core index (excludes food and energy categories) over the past 12 months.

Week in Review:

On Monday, stocks opened the week relatively unchanged in what was an uneventful day. One of the only headlines was the continued strike of the United Auto Workers where no progress was made over the weekend on a new labor contract. In addition, discussions around a potential government shutdown were rising with a key deadline approaching. Data included homebuilder confidence falling in negative territory to the lowest level since April.

Crude oil continued to trek higher in the beginning of the week with a 2.5%

increase early in the day on Tuesday (however giving up gains and falling slightly for the day) further complicating the inflation picture with many strategists increasing their oil price forecasts. It was an uneventful day again, with data in the morning showing a slight increase in housing starts from August. Treasury yields saw an uptick with the 10-year yield 4 basis points higher to 4.36%, over higher oil and an uptick in inflation in Canada, while stocks fell 0.2%, near the highest levels of the day.

The main event for the week was Wednesday with the FOMC meeting and Chairman Powell’s press conference. The policy decision was as expected, no change in rates or its balance sheet reduction plans, but there was an upward shift on future interest rates in the projections, with policymakers seeing less rate cuts in 2024 and 2025 amid stronger economic growth and lower unemployment. This slightly more hawkish stance resulted in the markets believing the Fed’s “higher for longer” stance and Treasury yields moved higher as stocks moved lower, finishing the day down 0.94%.

Investors took more time to digest the FOMC meeting and projections and came into Thursday trading in selling mode for both stocks and fixed income, following global markets lower. Data on jobless claims moved back to the lows of the year, and near 50-year lows, reflecting the tight labor market, while the pace of existing home sales were relatively unchanged in August compared to July. It was a big risk off day with US stock indices finishing at least 1% lower across the board and the S&P 500 seeing its worst day since March.

It was a quieter session on Friday, with investors still digesting the recent FOMC meeting and additional talks on the United Auto Workers strike after it still could not come to a contract agreement with the automakers. Fed speak picked back up with three policymakers saying inflation has not yet shown substantial improvement, further tightening could still be appropriate, and additional talk about the uncertainty on holding rates or doing more tightening. Treasuries saw some upside as yields gave up some of Thursday’s increases while stocks fell 0.23%.

It was a risk-off week with value outperforming growth again and the worst week since March for US stocks as Treasury yields spiked to new 16 year highs. The dollar was higher on tighter Fed policy expectations, gold was slightly lower, and oil snapped a three week winning streak with a 0.8% decline. The 2-year Treasury rose 6 basis points to 5.10% and 10 year Treasury rose to a new 16 year high of 4.51% before finishing the week at 4.44%, up 11 bps on the week. The four major US stock indices finished as follows: Dow -1.89%, S&P 500 -2.93%, NASDAQ -3.62%, and Russell 2000 -3.82%.

Recent Economic Data

The housing market index, a survey of home builders on housing activity, was 45 for September, lower than the 50 expected and the reading from August (a level of 50 is breakeven – below 50 is weaker/slowing activity, above 50 is positive/growing activity). It was the first negative read in seven months. The current sales index fell 6 points to 51, expectations on sales over the next six months fell 6 to 49, while buyer traffic was very weak and back near the lowest levels of the year at 30. About 32% said they cut prices in September, up from 25% in August. The special question this month for the homebuilders was who is buying homes? The results showed 42% are first time buyers, much higher than we see from other data (which shows around 25%-30%).

The number of housing starts in August was 1.283 million (on an annualized basis and seasonally adjusted), a 11.3% drop from the July rate, 14.8% below the rate from a year ago, and falling to the lowest level since the pandemic lows. The larger decline was driven by a 26% drop in multi-family units. The number of permits filed to build a new home increased 6.9% to an annualized pace of 1.543 million however and about 7% more the expected. The number of housing units authorized but not yet started was relatively stable at 282k and still about 50% higher than pre-pandemic levels, as home builders try to keep up with the strong demand, with the number of houses still under construction relatively unchanged as well around 1.700 million.

Sales of existing home were relatively unchanged in August compared to the July sales pace, with 4.04 million existing homes sold in the month (a seasonally adjusted annualized pace). Existing homes sales are based on closings so this number reflects contracts that were signed in July. The story is basically the same – higher interest rates and inventory of existing homes on the market are keeping the sales pace about 2 million below the sales pace from the pandemic years (and about 1.5 million below the pre-pandemic sales trend). The number of existing homes on the market was 1.1 million units, down 1% from July and 14% from a year ago, with unsold inventory sitting at just 3.3 month supply (a balanced market is considered 5 months supply). The issue is people that would potentially move into a new home are no longer doing so to avoid being locked into a higher mortgage rate with their new home, something known as the mortgage rate lock-in effect. The consequence of less supply and still strong demand is higher homes prices, with the median price of an existing home up 3.9% from a year ago, picking up pace over the past several months.

The number of unemployment claims filed for the week ended September 16 decreased 20,000 from the prior week to 201,000, the lowest level of initial claims since January and back near 50 year lows. The four-week average declined 8k to 217,000. The number of continuing claims fell 21k from the prior week to 1.662 million, also the lowest since January (the low was 1.290 million exactly one year ago). The four-week average fell 9k to 1.687 million.

Manufacturing activity in the Philly region, via the Philly Fed manufacturing index, deteriorated again in September with the index at -13.5, down from a positive 12 last month and versus the expectation of somewhere near breakeven. It was the 14th negative read out of the last 16 months. The survey noted general activity, new orders, and shipments all turned negative in the month while prices were near long-run averages. About 29% of firms reported a decrease in activity, 16% reported an increase, and about 55% reported no change.

Company News

Disney announced it would expand its investment in its parks segment by accelerating its investment in the segment to $60 billion over the next 10 years, nearly double the investment it made over the past 10 years. It said the investments will involve enhancing both domestic and international parks and expanding its cruise line capacity, while prioritizing projects that generate stronger returns.

Cisco announced this morning it has agreed to acquire the cybersecurity company Splunk for $157 per share in a deal that values Splunk at $28 billion, a 31% premium to where the stock closed yesterday. Cisco said the deal would “help make organizations more secure and resilient,” and will “accelerate Cisco’s business transformation to more recurring revenue.”

US Steel is reportedly receiving interest from four potential bidders: Cleveland Cliffs, ArcelorMittal, an unidentified bidder, and another potential buyer, according to CNBC. US Steel previously said it will begin a review process after it rejected a bid from Cleveland Cliffs and others. Frist round bids for the company are reportedly due this week. Also, reports said US Steel is refusing to open its books to Cleveland Cliffs which prevents Cliffs from participating in the sales process because Cliffs refuses to sign a six-month standstill agreement that would prevent it from challenging the Board of Directors of US Steel. Later in the week it was reported by Bloomberg that Stelco was considering a bid for the company and was in talks with unnamed partners to participate in a bid.

UK’s regulators, the Competitions and Market Authority (CMA), said late last week the revised deal in Microsoft’s acquisition of Activision Blizzard addresses its previous antitrust concerns around cloud gaming and they are now consulting on remedies before their final decision in October. Microsoft said as part of the deal it would sell Activision’s cloud gaming rights to competitor Ubisoft to help push the deal through regulators.

According to a report by the Insider, Amazon is considering a new standalone subscription that would give membership for healthcare and grocery offerings, potentially including the integration of One Medical primary care service. It said Amazon is struggling to attract young customers and low-income households for its Prime membership. Separately, Amazon said it will include a limited number of advertisements in shows and videos under its Prime Video service starting next year. At the same time it will begin offering an ad-free option for an additional $2.99/month.

Uber warned that a European Union reclassification of gig workers could force Uber to raise prices for customers, with price increases as much as 40%, or even a shut down in hundreds of cities. It added that the reclassification could result in a 50%-70% reduction in work opportunities.

Other News

The United Auto Workers strike against the automakers continued over the weekend with no labor contract agreed on. The UAW threatened to have more workers strike, on top of the current 12,700, across more manufacturing plants if it still made no progress by the Friday deadline. It will expand the strike to another 38 plants across 20 states. However, it said no additional strikes would occur against Ford as the company has shown more progress and more seriousness about reaching a deal.

House Speaker Kevin McCarthy has faced multiple set backs after giving it 3 attempts to pass a budget bill, but all have failed and Congress has just six days left to agree to a budget plan for the next fiscal year. McCarthy has failed to gain support of all Republicans. In a shutdown, most essentials, like social security payments and national defense, will continues but non-essentials like national parks may be closed. There is a wide consensus by market and political strategists that a shutdown wouldn’t have a wide impact on stocks or the economy, as going back to the 1990’s there have been several shutdowns and all have had minimal impacts. At this point the most likely path forward, and what is being discussed more over the weekend, is Republican passing a stopgap funding measure that would extend government funding long enough for Congress to find a longer-term solution.

Oil moved over $90/barrel earlier last week (highest since November) but pulled back slightly over the second half of the week. It was reported by Bloomberg that oil inventories at the Cushing hub (the largest oil hub in the US) reached the lowest seasonal level in five years after seeing a drop for six straight weeks, with stockpiles reaching minimum operating levels for the facility (22.9 million barrels). A separate report from the Financial Times said hedge funds continue to ramp up bets on oil prices exceeding $100/barrel, adding to the recent upward pressure on oil.

The Bank of England chose to keep policy rates unchanged at 5.25% with a 5-4 vote as the other four voted to increase rates again. On the other hand it voted unanimously to shrink its balance sheet at a faster pace. It said it needs policy to be sufficiently restrictive for a period long enough to bring inflation lower and if there is more evidence of persistent inflationary pressures it is ready to tighten policy further, very similar comments to the Fed.

In other central bank news the Swiss National Bank surprisingly left rates unchanged, the Norges Bank raised rates another 25 basis points as expected, with more hawkish comments. The Bank of Japan lefts its short term policy rate in negative territory at -0.1% and continues to target the yield on its 10-year government bond at 0%, allowing it to trade within a 50 basis point range.

Did You Know…?

Holidays Sales Forcasts:

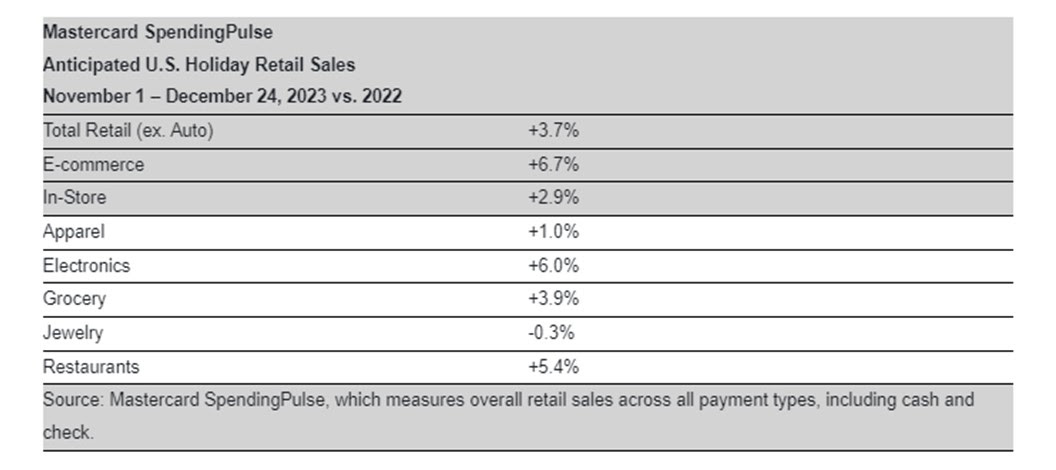

Mastercard SpendingPulse estimates that US retail holiday sales (the period from November 1 to December 24) will increase 3.7% this holiday shopping period. With a 3.7% rate of inflation over the past 12 months, that would put real (inflation adjusted) sales growth of 0%. E-commerce sales are expected to increase 6.7% while in store sales are expected to increase 2.9%. Due to the new technology in AI, as well as consumers looking to upgrade gadgets to the latest model after the pandemic surge, it expects sales of electronics to see strong growth of 6.0%.

WFG News

The Election & Its Impact on The Markets

Wentz Financial Group is happy to announce we will be brining back guest speaker Phil Orlando for a discussion on his and Federated’s thoughts on the current market and economic environment. Phil will expand on the election of 2024 and its implications for markets. Phil Orlando is Chief Equity Market Strategist of Federated Investors with over 43 years of experience and is responsible for formulating Federated’s views on the economy, markets, and the firm’s investment positioning strategies. RSVP early as this event will reach capacity quickly!

Tuesday, October 3 @ 6:00 pm

Wednesday, October 4 @ 12:00 pm

The Week Ahead

Market focus will shift back to economic data, along with several ongoing issues like the unresolved UAW strike against the big three automakers and the looming US government shutdown. The most notable data release is the personal income and outlays report Friday morning that comes with the PCE price index – the Fed’s favorite inflation measure. The index is expected to be up 0.5% in the month with the increase in the core index expected to have increased 3.9% over the past 12 months. Elsewhere, on Tuesday we see an update on home prices for July with Case Shiller Home Price Index, consumer confidence for September, and new home sales for August. Durable goods orders come out Wednesday. Then Thursday we will see the final revision on Q2 GDP, the pending home sales index, and weekly jobless claims which has moved back near the pandemic lows, and Friday will include an update on September’s consumer sentiment. The Fed has several policymakers making public appearance that may receive attention. On the corporate side, several earnings reports will be in focus including Costco on Tuesday, Micron, Paychex on Wednesday, Nike, CarMax on Thursday, and Carnival on Friday.

By Wentz Financial|2023-09-26T15:03:20-04:00September 26th, 2023|Wentz Weekly|Comments Off on Wentz Weekly: A Higher Neutral Interest Rate?